What is Blockchain? A Guide to Data Integrity and Trust

Dec 23, 2025

Thomas Hepp

Dec 23, 2025

The Evolution of Trust: Why Blockchain Matters Today

Here's something that keeps enterprise security leaders up at night: the global economy runs on trust, and that trust has a serious problem.

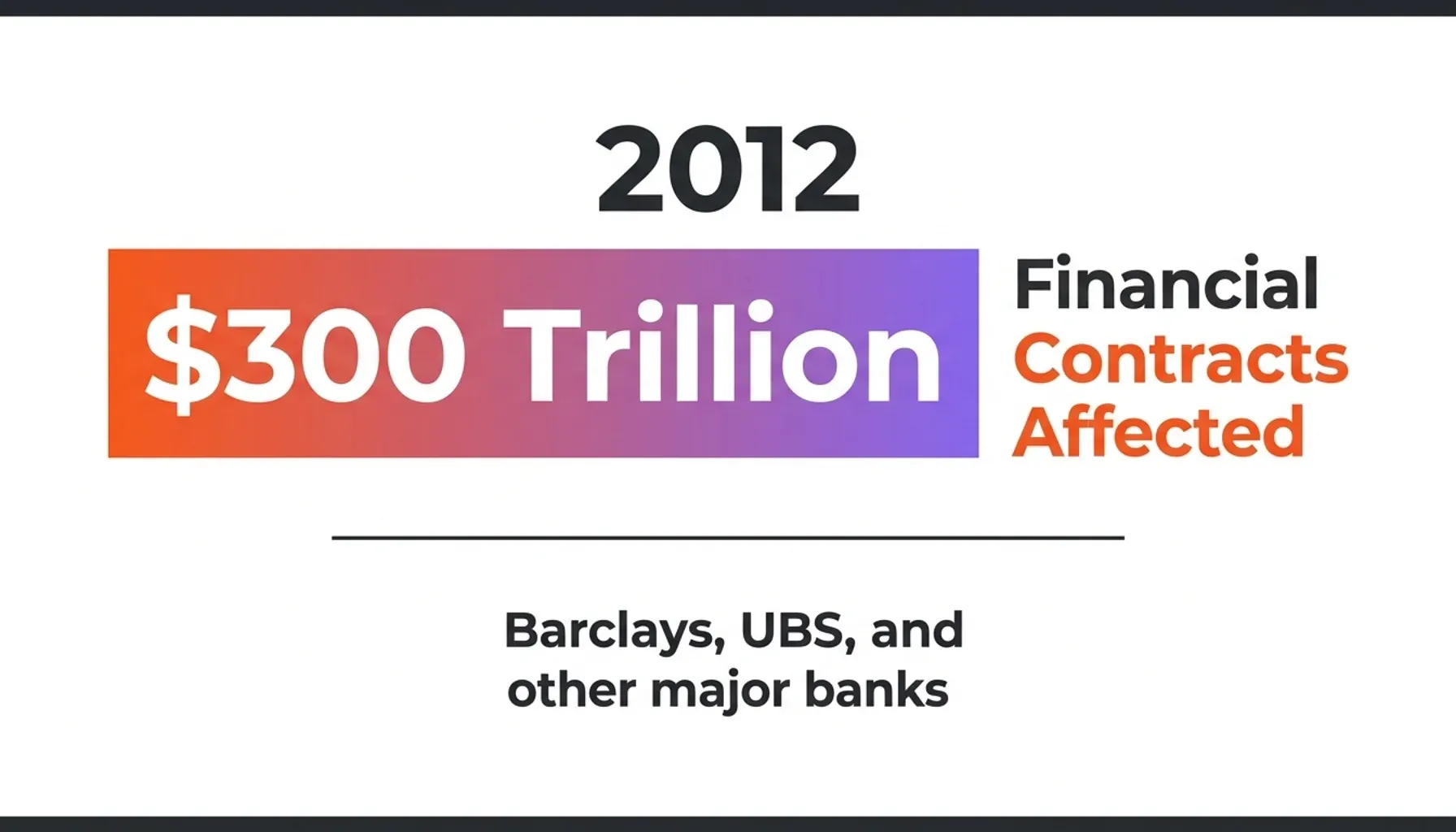

For centuries, we've handed that responsibility to centralized authorities—banks, notaries, clearinghouses, and system administrators—to verify transactions, authenticate documents, and maintain ledgers. But digital transformation exposed a critical flaw in this model: centralized databases are inherently mutable. Any administrator with sufficient privileges can alter, delete, or backdate records without detection. This isn't hypothetical. In 2012, the LIBOR scandal revealed that traders at Barclays, UBS, and other major banks had systematically manipulated benchmark interest rate submissions stored in centralized systems—affecting an estimated $300 trillion in financial contracts worldwide. Nobody outside the inner circle noticed for years. In an era where digital assets drive enterprise value, "just trust us" is no longer good enough.

The peer-to-peer electronic cash system introduced in 2008 offered a radical alternative: mathematical proof. By decentralizing verification and securing it with advanced cryptography, this architecture created the first truly immutable ledger. Today, the conversation has moved well beyond cryptocurrency volatility. Enterprise leaders now recognize that the underlying infrastructure—distributed ledger technology—addresses data integrity challenges that centralized systems simply cannot solve.

Data integrity is the gold standard of the modern digital economy. It guarantees that information stays complete, accurate, and unaltered throughout its entire lifecycle. When you secure data on a decentralized network, its authenticity becomes mathematically provable and independent of any single provider or administrator. That shift—from trusting a central party to verifying the mathematics—fundamentally changes how businesses manage risk, compliance, and intellectual property.

For over 12 years, OriginStamp has specialized in blockchain timestamping API infrastructure backed by peer-reviewed academic research. This infrastructure lets organizations anchor digital files to public networks, generating tamper-evident proof that a document existed in a specific state at a specific point in time. If you want to understand how distributed ledger technology actually works before securing your digital legacy, that's the right place to start.

How Blockchain Works: The Mechanics of the Digital Seal

At its core, a blockchain is a distributed digital ledger. Instead of storing data on a single centralized server, the ledger gets duplicated and distributed across a vast network of independent computers called nodes. This architecture eliminates any single point of failure and removes any central authority capable of unilaterally altering the record.

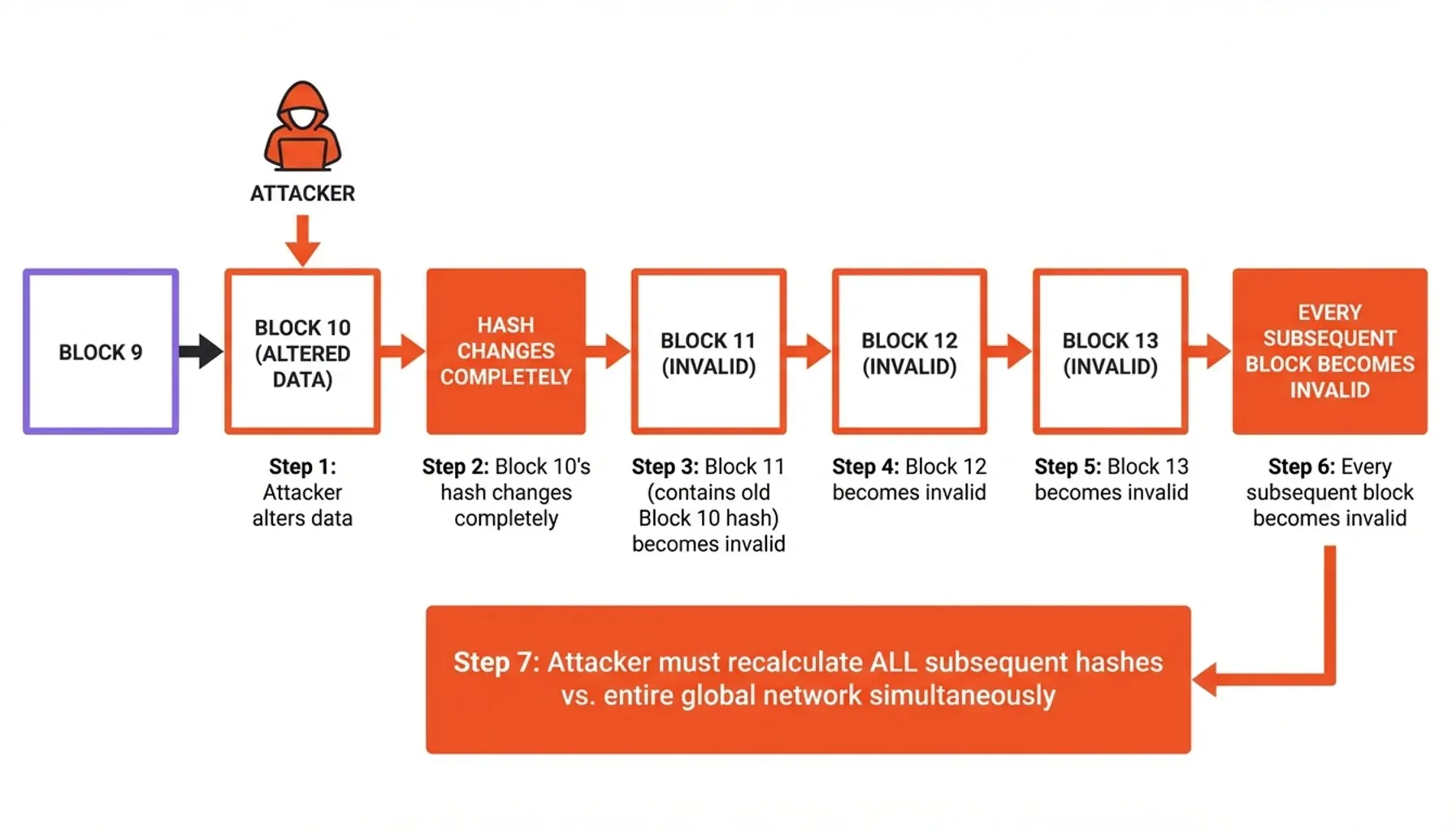

To understand the mechanics, look at the anatomy of a block. Every block in the chain contains three critical components: the relevant data, a cryptographic hash of that data, and the cryptographic hash of the immediately preceding block.

The hash acts as a unique digital fingerprint. When a block is created, its hash is calculated based on the data it holds. Change a single bit of that data—even swap a lowercase letter for an uppercase one—and the hash changes completely.

The real security lies in including the previous block's hash. This creates a chronological chain reaction. If a malicious actor tries to alter a historical record in Block 10, Block 10's hash changes. Block 11, which contains the old hash of Block 10, immediately becomes invalid. That invalidates Block 12, Block 13, and every block after it. To successfully alter a single piece of data, an attacker would need to recalculate the hashes for that block and every subsequent block—all while racing against the computational power of the entire global network. That's not a practical attack; it's computationally infeasible at any realistic scale.

This security is enforced by decentralized consensus. Before a new block joins the ledger permanently, the network of nodes must agree it's valid according to strict cryptographic rules. This consensus mechanism ensures all participants share a single, synchronized version of the truth. Distributing validation across thousands of independent entities gives the network a level of fault tolerance and tamper resistance that no centralized database can match.

Cryptographic Hashing: The Foundation of OriginStamp

The entire concept of an immutable ledger rests on the strength of cryptographic hashing algorithms—specifically SHA-256 (Secure Hash Algorithm 256-bit). A hash function takes an input of any size—a simple text document, a high-resolution video, or an entire database backup—and condenses it into a fixed-size string of characters. Brute-forcing a SHA-256 hash would require more computational steps than there are atoms in the observable universe—making reversal not just difficult, but physically unrealistic with any foreseeable technology.

Hashing is a one-way function. You can't reverse-engineer the original file from its hash. This introduces a critical advantage for enterprise applications: privacy by design. Organizations can't afford to upload sensitive contracts, proprietary code, or patient health records to a public network.

With OriginStamp, your actual data never leaves your local environment. Your system generates the SHA-256 hash locally and sends only that anonymous string of characters to the OriginStamp API. Because the hash reveals absolutely nothing about the underlying content, organizations can establish cryptographic proof of existence without compromising confidentiality or violating data protection regulations.

Once OriginStamp receives the hash, it uses an "anchor" concept to secure it. Rather than processing thousands of individual transactions directly on the blockchain—which would be prohibitively expensive and slow—OriginStamp aggregates hashes using a Merkle Tree structure. The single root hash of this tree, which mathematically represents all the individual hashes beneath it, then gets anchored into public networks like Bitcoin and Ethereum. This process creates an independent blockchain timestamp, providing cryptographic proof that your specific digital fingerprint existed at that exact moment.

Beyond the Ledger: Blockchain as an Integrity Layer

Not all distributed ledgers offer the same level of security and independence. The enterprise market is often confused by the distinction between public, private, and consortium blockchains—and that confusion is worth clearing up, because it matters enormously.

Private blockchains are operated by a single entity or a closed group of participants. While they use the structural mechanics of blocks and hashes, they lack the decentralized consensus that makes the technology genuinely revolutionary. In a private network, the administrator still retains the power to rewrite the ledger, alter consensus rules, or censor transactions. Consortium blockchains distribute this power among a group of known organizations, but they still require you to trust that the consortium won't collude to manipulate data.

Public blockchains—Bitcoin and Ethereum being the most prominent—are permissionless and globally distributed. Anyone can participate, and no single entity, corporate or governmental, can control them. This extreme decentralization is precisely why public blockchains offer the highest level of independence from providers. When OriginStamp anchors a hash to the Bitcoin network, thousands of independent nodes worldwide validate that proof. Even if OriginStamp were to cease operations tomorrow, the cryptographic proof of your data's existence would remain verifiable forever.

This architecture enables a fundamental shift: from administrative promises to mathematical provability. Traditional IT security relies on a "Trust but Verify" model, which in practice often means trusting the system administrator and verifying through periodic, manual audits. An integrity layer built on public blockchains upgrades this to "Verify, Don't Trust." It delivers tamper-evident proof in real time. If a document is secretly altered, the discrepancy between the file's current hash and the blockchain-anchored hash immediately exposes the manipulation—turning silent data corruption into a loudly ringing alarm.

Smart Contracts and Programmable Blockchains: On-Chain Logic, Determinism, and Platforms

Blockchain's utility extends well beyond passive record-keeping. Smart contracts—self-executing programs stored directly on a blockchain—let organizations encode business logic that runs automatically when predefined conditions are met. Think of them as contracts that enforce themselves, with no intermediary needed to pull the trigger.

On Ethereum and similar platforms, smart contracts are written in languages like Solidity and deployed to the network as immutable code. Once live, they execute deterministically: given the same inputs, every node on the network reaches the same output, every single time. There's no ambiguity, no discretion, and no room for a counterparty to quietly reinterpret the terms. A supply chain payment releases automatically upon verified delivery. An insurance payout triggers when a flight delay is confirmed on-chain. A licensing agreement revokes access the moment a subscription lapses. All of these become programmable, auditable, and tamper-resistant.

Determinism is what makes this trustworthy—and also what makes it unforgiving. The Ethereum Virtual Machine (EVM) enforces strict execution rules so that every node processes identical logic. Other platforms take different architectural approaches: Solana prioritizes throughput using a Proof of History mechanism; Hyperledger Fabric targets permissioned enterprise environments where participants are known; Cardano uses a formally verified smart contract language designed to reduce logic errors before deployment. Each platform makes different trade-offs between speed, decentralization, and programmability—and choosing the right one depends entirely on your use case.

For enterprise applications, this programmability is a significant leap forward. It eliminates the manual overhead of contract administration, reduces the risk of human error, and creates a transparent, auditable execution record that all parties can independently verify. The immutability of on-chain logic means that once a smart contract is deployed, no party can quietly amend the terms in their favor.

However, that same immutability introduces a sharp double-edged risk. If a smart contract contains a bug or a logic flaw, it cannot simply be patched after deployment—at least not without significant architectural planning. The 2016 DAO hack, in which an attacker exploited a reentrancy vulnerability to drain roughly $60 million in Ether, remains the most cited example of what happens when flawed on-chain logic meets an immutable execution environment. Formal auditing by specialized security firms is now considered non-negotiable before any production deployment.

Other key risks include oracle dependency—smart contracts can only act on data that exists on-chain, so they rely on external data feeds called oracles to interact with the real world. If an oracle is compromised or manipulated, the contract executes correctly based on bad data, with no mechanism to reverse the outcome. Governance risk is equally real: upgradeable contract patterns introduce administrative keys that, if mishandled, recreate the very centralization that blockchain is meant to eliminate.

For organizations integrating blockchain timestamping into compliance workflows, understanding these programmability trade-offs is essential. OriginStamp's anchoring approach deliberately keeps business logic off-chain, using the blockchain purely as an immutable notary layer. This sidesteps smart contract execution risk entirely while still delivering the cryptographic integrity guarantees that matter most for audit trails and legal defensibility.

Real-World B2B Use Cases: Proving the Impossible

The theoretical elegance of decentralized security translates into powerful, pragmatic applications for B2B enterprises. Wherever trust, accountability, and data integrity are mission-critical, blockchain timestamping provides a decisive operational advantage.

Evidence Preservation and Legal Disputes In legal proceedings, the authenticity of digital evidence is frequently challenged. Metadata on photos, videos, and documents is easily manipulated using standard software. By automatically generating a blockchain timestamp the moment a file is created, organizations build a verifiable record of authenticity that holds up under scrutiny. This is particularly vital in scenarios involving insurance claims, law enforcement, or corporate liability—where stopping deepfake evidence tampering requires a mathematically verifiable origin point established before any manipulation could occur.

Intellectual Property and Trade Secrets Filing formal patents is slow, expensive, and public. During research and development, engineering firms, pharmaceutical companies, and software developers generate vast amounts of valuable intellectual property that can't yet be patented. By timestamping CAD files, lab notes, and source code daily, companies establish a clear prior-use claim. If a competitor attempts to patent the same technology or steals the trade secret, the original creator has mathematical proof of exactly when they held the proprietary data—securing their legal position without prematurely disclosing the IP.

Supply Chain Transparency and Industrial Audit Trails Modern manufacturing and logistics depend on complex, multi-tiered supply chains. When a component fails in aerospace or automotive, determining liability requires a flawless audit trail. Traditional databases allow suppliers to potentially alter quality assurance records retroactively to avoid blame. Integrating an immutable ledger into manufacturing execution systems ensures every sensor reading, quality check, and handover protocol is permanently sealed. This kind of industrial supply chain traceability keeps the historical record intact, dramatically reducing dispute resolution times.

Healthcare and Defense Infrastructure In heavily regulated sectors like healthcare and defense, data manipulation isn't just a financial risk—it's a threat to human life and national security. Zero-trust architectures require that every action, access log, and configuration change be independently verifiable. Acting as an invisible integrity layer beneath these critical systems, blockchain technology ensures patient records can't be silently altered to cover up medical malpractice, and defense configurations can't be maliciously modified without leaving an indelible cryptographic footprint.

The Compliance Factor: Blockchain in Archiving and ERP

For enterprise software vendors—particularly those building Enterprise Resource Planning (ERP) systems—robust archiving and compliance features represent a massive developmental burden. Regulatory frameworks demand strict adherence to electronic record-keeping standards. In Germany, the GoBD dictates the proper management and storage of digital books. In Switzerland, the GeBueV mandates legal requirements for electronic archiving.

The core requirement of these regulations is an unchangeable audit trail. Auditors must verify that financial documents, invoices, and tax records haven't been altered since their creation. Traditionally, achieving this required complex Write-Once-Read-Many (WORM) storage hardware and extensive custom software development.

OriginVault transforms this compliance burden into a seamless, white-label premium feature for ERP vendors. Designed specifically as a compliance and archiving engine, OriginVault integrates blockchain security directly into existing software ecosystems. When an invoice is finalized in the ERP, OriginVault automatically archives the document, generates a cryptographic hash, and anchors it to the blockchain—delivering out-of-the-box compliance with GoBD, GeBueV (KRM-certified), and ISO-27001 standards. That saves ERP vendors years of development time and millions in R&D costs.

For robust security, OriginVault uses an advanced AES-256 data seal—combining military-grade encryption with a blockchain certificate. Even if a malicious actor gains root access to the server, they can't decipher the encrypted documents or alter files without breaking the blockchain seal. The result is an archiving solution that's tamper-proof even against system administrators.

OriginVault also operates on a foundation of digital sovereignty. Hosted on Swiss-based infrastructure—or deployable via cloud-agnostic environments (AWS/Azure/On-Prem)—it ensures enterprise data remains subject to Switzerland's strict Federal Act on Data Protection. This geographic and architectural independence gives C-level executives the strategic assurance that their data is protected from both unauthorized manipulation and foreign jurisdictional overreach.

The Future of Blockchain: Strategic Environment Analysis and AI

We're moving from the Information Age into what I'd call the Age of Authenticity—and the transition is turbulent. The rapid proliferation of generative AI has made it trivial to produce hyper-realistic synthetic media, sophisticated phishing campaigns, and forged documents. In an environment where seeing is no longer believing, establishing the origin and integrity of data is critical for strategic decision-making.

Blockchain technology is the necessary counterweight to AI-driven manipulation. While AI excels at generating content, distributed ledgers excel at verifying origin. By timestamping original media, sensor data, and strategic reports at the moment of creation, organizations build a verifiable chain of custody that can identify AI-generated synthetic media and deepfakes before they cause damage.

OriginStamp is actively expanding this capability through OriginRadar, an AI-powered strategic environment analysis tool engineered for Defense, Energy, and critical infrastructure sectors. Launching as a Proof of Concept in 2026, OriginRadar delivers situational intelligence and capability maps backed by blockchain-sealed data. For C-level and VP-level executives, this means decisions are no longer based on potentially compromised intelligence—they're grounded in mathematically verified operational realities. The integration of AI for analysis and blockchain for integrity represents the next frontier of enterprise security.

The implications extend further than any single product. As blockchain-based identity and data ownership frameworks mature, individuals and organizations alike will gain granular control over who accesses their data and under what conditions—a paradigm shift that makes the current model of centralized data custodianship look dangerously fragile by comparison. I'd argue that understanding how this technology scales across civilizational infrastructure gives you the clearest sense of just how foundational the underlying architecture is becoming.

Conclusion: Choosing Facts Over Promises

Blockchain technology is far more than a decentralized database. It's a proven infrastructure for establishing digital trust and data sovereignty at scale. By replacing the vulnerabilities of centralized administration with cryptographic proof—specifically, SHA-256 hashes that are computationally infeasible to reverse or forge—distributed ledgers keep data integrity intact across every phase of the digital lifecycle.

In a business environment where compliance failures, intellectual property theft, and data manipulation carry devastating financial and reputational consequences, relying on promises is a profound risk. Leaders must demand independent, peer-reviewed technology that guarantees tamper-evident proof.

OriginStamp builds trust with facts. Whether through the core timestamping API that secures millions of digital assets, or through the OriginVault engine that delivers effortless compliance for ERP vendors, the mission is clear: provide verifiable, cryptographically grounded proof of authenticity. Secure your digital legacy today by integrating a data integrity standard that auditors, courts, and regulators can independently verify.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.