Benefits of Private Blockchain: Security, Transparency, Fast Transactions, and More

Salomon Kisters

May 16, 2022This post may contain affiliate links. If you use these links to buy something we may earn a commission. Thanks!

When most people think of blockchains, they think of the public ones that are used to power cryptocurrencies like Bitcoin and Ethereum.

But there is another type of blockchain - a private blockchain. Contrary to its name, a private blockchain is actually quite public and is often used by businesses to manage their data securely.

So what is the point of a private blockchain?

Users may only access some data and perform some functions, while everything else remains off-limits. The access granted depends on the specifications set forth by the network creator.

However, you probably shouldn’t store raw data on the blockchain; instead, you can use OriginStamp to anchor data on blockchains – a much safer, secure, and convenient option.

What is a Blockchain?

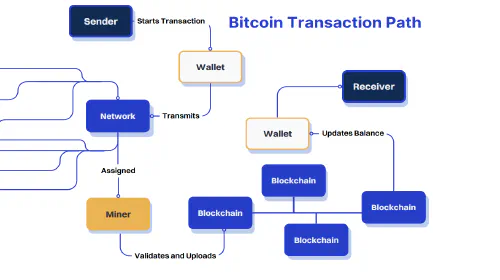

A blockchain is a way of storing sensitive information as complex code. This storage is kept in computers connected over a wide-scale network and is used extensively in cryptocurrency.

Blockchains are specially designed to help keep data secure and prevent leaks, infiltration, and hacking. They comprise ’nodes’ that store information. These nodes combine to form chunks of data called ‘blocks,’ and this entire system makes up the blockchain infrastructure.

This feature is vital for cryptocurrencies, NFTs, or any other digital transaction involving confidential information where rock-solid security is required.

Where are Blockchains Used?

The most popular use of blockchains is in cryptocurrencies and crypto mining. Blockchains, in this case, are like public ledgers, housing encoded information in the form of packets of data called ‘blocks.’ Each block contains confidential information, all of which is encoded and sealed.

Apart from cryptocurrencies, blockchains also provide the foundations for using decentralized applications. Blockchains, like Ethereum, Cardano, Solana, Polkadot, etc., are immensely extensive and complex ecosystems, hosting a wide variety of DApps, metaverses, and DeFi projects.

What Is the Difference Between a Public and a Private Blockchain?

In a public blockchain, the chain information is available to all users. Anyone can join the chain if they want to since there is no central authority to govern the system. However, private blockchains are more exclusive.

Users can only join a private system if they have permission from the system administrator. These chains have authority on the network and answer to a moderator.

Pros of a Private Blockchain

Private blockchains are in use globally by many different companies and digital currencies due to their inherent safety. There are multiple reasons behind their extensive use today, which we will discuss in detail next.

Administrator Control

The network creator or administrator controls the type of access allowed to users in the private system and can moderate the entire system.

Private blockchains can also monitor the number of active users on the network. Therefore, the online traffic is low, causing the transaction speed to stay very high and preventing malfunctions.

Security

Blockchains are widely acknowledged as the most secured database technology. That’s exactly why the founders of digital currency projects, such as Bitcoin and Ethereum, decided to base their innovations on the blockchain mechanism.

It is impossible to cheat the system and outsmart the code. If a centralized entity also wants to add that extra layer of security to their exclusive data, private blockchains provide that benefit.

Fast Transactions

If the total number of users is kept low, the system can approve transactions faster while data transfers occur efficiently, at thousands of transactions per second! Public databases have no way of restricting random users from logging in.

This excessive online traffic may lead to glitches, slow service, and even system malfunctions mid-transaction.

Full Transparency

There is full transparency within a private blockchain. The users carrying out a transaction have complete access to all the information related to their deal and store it. Public databases do not allow this.

On the other hand, private blockchains are exceedingly safe as random users cannot be privy to your transactions since everything is secure.

Negligible Fees

In public chains, fellow miners might verify transactions. This phenomenon can result in commissions and fees, incurring additional expenses.

In a private blockchain, the system administrators verify all transactions, so miners cannot profit off your deals. Therefore, the charges for network accommodation are null or very low.

No Disputes

Unlike public databases, private blockchains are under a single entity. The localized system only answers to one creator, leading to harmony and quick decisions regarding verification, data transfers, and viewing information.

There is no waste of time in contacting all the creators, reaching a consensus, and then providing you with a final answer.

Scalability

The private blockchains are scalable, albeit on a medium level. Since the private blockchain deals with a pre-set amount of data, it may scale up and take larger data loads, carry out more transactions, and support more users.

However, the scalability is, at best, medium in scope since these companies would have to incur heavy expenses for significant upgrades.

Cons of a Private Blockchain

There are some drawbacks to having a private blockchain. It does come with its advantages, but some would argue that the cons outweigh the benefits.

Uncontrolled Power to One Entity

In a private blockchain, most of the power lies with the system creator. Therefore, the creator may change the system, rewire the entire software, and in a nutshell, do as he pleases.

Expenses

When compared to a conventional database, private blockchains are a lot more expensive. Private blockchains require the latest hardware and the extra security features and protocols needed for maintenance and heavy code, leading to a pricey system.

Administrators may find the low online traffic against them since the funds might not be sufficient for maintenance.

Dependence on One System

If a company relies on a private blockchain, it may shut down in a power outage. Blockchains require large amounts of electricity to function. If the company is located in a region with an unstable electricity supply, its private blockchain may depend on backup generators or the power supply.

This reliance can drain resources or tarnish the company’s reputation.

Security Holes

Private blockchains claim to keep unidentified users out of the system and only employ trusted third parties.

Many users feel that hiring third parties defeats the entire purpose of having a private platform and are uncomfortable with unknown ’trusted’ parties within the loop.

Poor Data Storage

It has recently come to light that blockchains are not the ideal means of storing data. They require unnecessary expenses to do so and lead to extra hassle.

Users feel that traditional databases are a lot more energy-efficient and help keep costs down. Some companies stay away from blockchain technology altogether, claiming it has overcomplicated many things for them.

IBM Hyperledger Fabric: a Leading Private Blockchain

The IBM Hyperledger Fabric is arguably one of the most, if not the most, popular and widespread private blockchains in the world. IBM is one of the leading advocates of blockchains since the creator of Bitcoin, Satoshi Nakamoto, invented the technology. Hyperledger Fabric is an open-sourced platform where only known or ‘permissioned’ users share and transfer data.

The platform is an attempt to promote blockchain technology and help users create more blockchain projects, solutions, and applications, particularly for private companies. According to Monika Proffitt, IBM charges an upward of $120,000 every year to host its Hyperledger Fabric System.

Are Blockchains Good for Storing Data?

Contrary to popular belief, blockchains are not a good solution for storing data. This is because the information on blockchains is stored on nodes. Nodes are the building blocks of the entire blockchain infrastructure and help store data.

Hundreds of nodes are needed to store data on blockchains (100,000 in the case of Bitcoin). Therefore, many companies and networks find it tiresome to store data on blockchains. A large number of nodes tends to increase expenses and energy consumption.

The hardware required to efficiently monitor blockchains is also expensive and high-maintenance as compared to traditional databases.

Conclusion

Private blockchains are useful as far as security is concerned. The users can safely carry out all transactions without fear of hacks or malicious software.

The transparency inherent in private blockchains is another attractive feature, but traditional databases are better for data storage. Data storage via blockchains seems unnecessary in this case.

However, it is vital to understand that blockchain technology is still new, and we have barely scratched the surface. Further research and development related to blockchain technology should lead to better performance in the futur

Stay informed with the latest insights in Crypto, Blockchain, and Cyber-Security! Subscribe to our newsletter now to receive exclusive updates, expert analyses, and current developments directly to your inbox. Don't miss the opportunity to expand your knowledge and stay up-to-date.

Love what you're reading? Subscribe for top stories in Crypto, Blockchain, and Cyber-Security. Stay informed with exclusive updates.

Please note that the Content may have been generated with the Help of AI. The editorial content of OriginStamp AG does not constitute a recommendation for investment or purchase advice. In principle, an investment can also lead to a total loss. Therefore, please seek advice before making an investment decision.

How to Create a Bitcoin Blockchain Address: A Step-by-Step Guide

Discover the process of generating a Bitcoin blockchain address through our detailed step-by-step tutorial. Get started with cryptocurrency now!

Blockchain 1.0 vs. 2.0 vs. 3.0 - What's the Difference?

Blockchain is a disruptive technology that has been around for 40 years. But what's the difference between Blockchain 1.0, 2.0, and 3.0?

Top Reasons Why Your Bitcoin Transaction is Still Unconfirmed

If you've ever transferred cryptocurrency, then you probably have experienced a delay in the confirmation of your transactions. Why is that, and what can you do?

Protect your documents

Your gateway to unforgeable data. Imprint the authenticity of your information with our blockchain timestamp