MiCA Stablecoin Reserves: Timestamping Attestation Evidence

Jun 11, 2026

Thomas Hepp

Jun 11, 2026

The New Era of Stablecoin Oversight: MiCA's Reserve Requirements

In 2023, a stablecoin issuer could publish a PDF and call it a reserve disclosure. Under MiCA, that era is over. The question now is whether the industry actually knows what replaces it, and most compliance teams I've spoken with are still figuring that out.

The Markets in Crypto-Assets Regulation, Regulation (EU) 2023/1114, establishes one of the world's most rigorous legal frameworks for digital asset oversight, and reserve transparency sits at its core.

Under MiCA, stablecoins fall into two primary categories: Asset-Referenced Tokens (ARTs), backed by a basket of assets including fiat currencies, commodities, or other crypto-assets, and E-Money Tokens (EMTs), pegged 1:1 to a single fiat currency. Both carry mandatory reserve requirements. Issuers must hold sufficient, segregated reserve assets at all times, assets that cannot be commingled with operational funds and must be accessible for redemption on demand.

This is not a soft guideline. ESMA's technical standards under MiCA specify how reserves must be composed, valued, and disclosed. Issuers of significant ARTs face additional obligations: monthly reserve disclosures, independent audits, and regular reporting to competent national authorities.

The shift is fundamental. For years, the crypto industry operated on a "trust us" basis, with issuers publishing reserve claims backed by no independent verification mechanism. MiCA replaces that model with a "verify us" mandate. Failure to comply carries severe consequences: suspension of token issuance, financial penalties, and potential revocation of operating authorization across EU member states.

If you're a stablecoin issuer building your MiCA disclosure stack right now, here's what most frameworks get wrong: they focus on what to disclose, not how to prove the disclosure is accurate, timely, and tamper-evident. That distinction is where the real compliance risk lives.

The Anatomy of a Proof-of-Reserve (PoR) Attestation

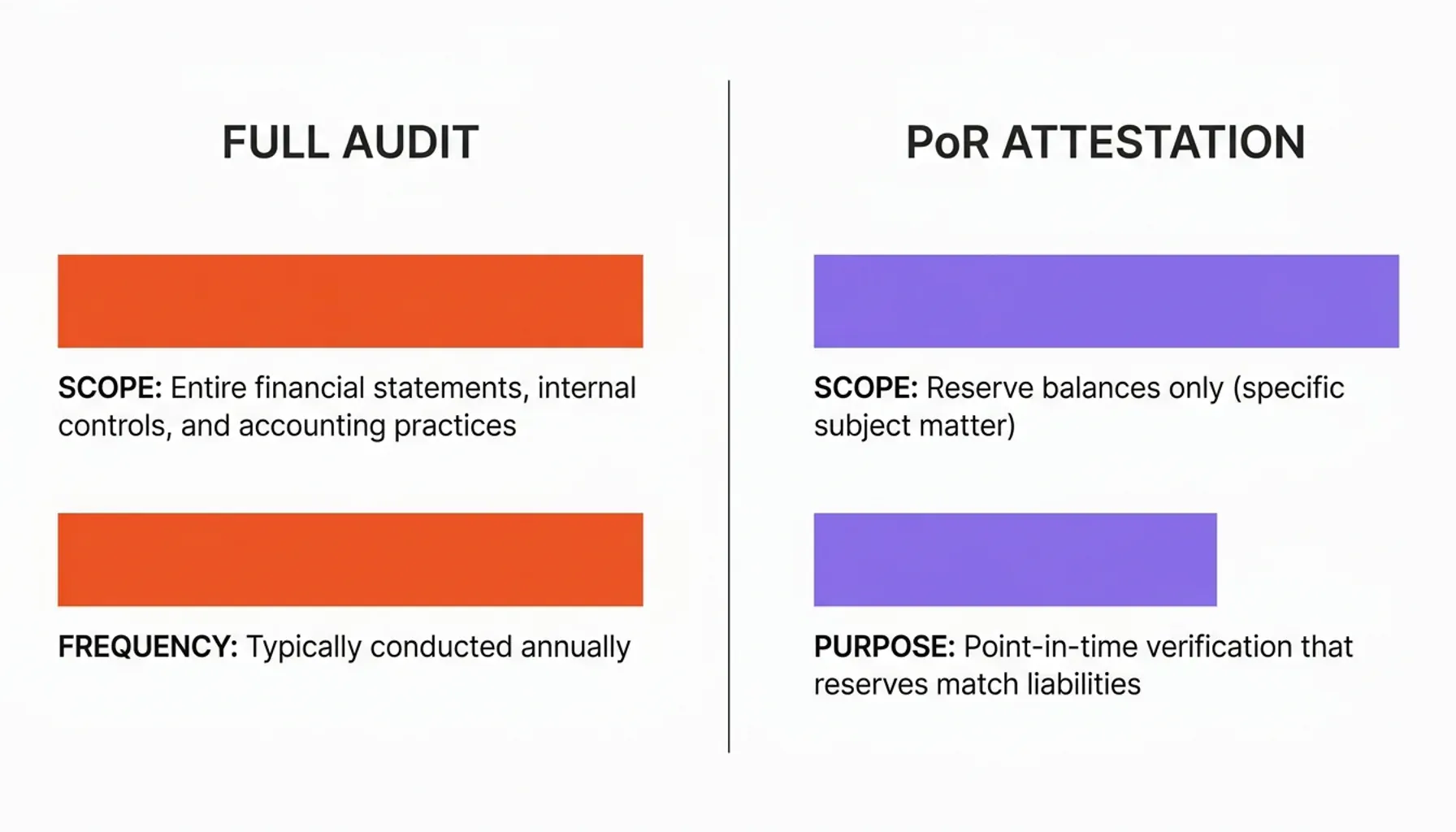

A Proof-of-Reserve attestation is not the same as a full financial audit. If you're a compliance officer or legal counsel working under MiCA obligations, this distinction matters more than most people realize.

A full audit examines an entity's financial statements, internal controls, and accounting practices in their entirety, typically conducted annually by a licensed auditor. A PoR attestation, by contrast, is a point-in-time verification that the reserve assets backing a token supply actually exist and meet the claimed valuation. It answers one specific question: at this moment, do the reserves match the liabilities?

Attestation engagements under SSAE 18, the prevailing standard used by major accounting firms, require the practitioner to examine specific subject matter (in this case, reserve balances) and express a conclusion based on defined criteria. The auditor doesn't opine on the broader financial health of the issuer. They confirm: the reserves existed, in this form, at this snapshot date.

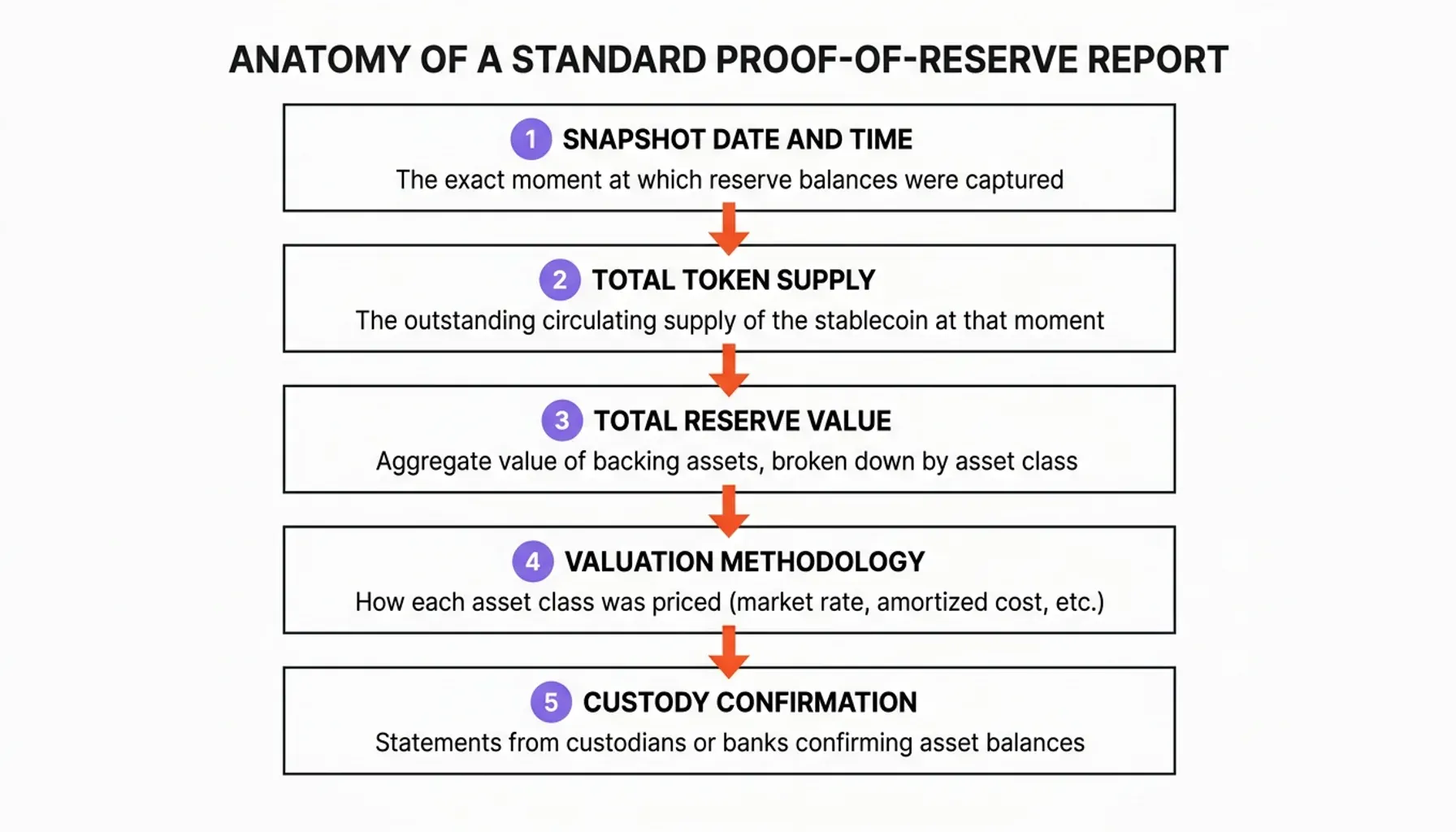

A standard PoR report contains several core components:

- Snapshot date and time: The exact moment at which reserve balances were captured

- Total token supply: The outstanding circulating supply of the stablecoin at that moment

- Total reserve value: The aggregate value of backing assets, broken down by asset class

- Valuation methodology: How each asset class was priced (market rate, amortized cost, etc.)

- Custody confirmation: Statements from custodians or banks confirming asset balances

Here's the problem. In current practice, these reports are almost universally published as PDF documents hosted on the issuer's website. That introduces a fundamental vulnerability: the document itself carries no cryptographic proof of when it was created or whether its contents have been altered since publication.

A PDF's metadata can be edited. A web server's "Last Modified" timestamp can be manipulated by anyone with administrative access. An issuer facing a temporary liquidity shortfall has a technical window, however brief, to delay publication, backdate a report, or quietly replace a filed document with a revised version. Under MiCA, that window represents legal and reputational risk of the highest order.

The Integrity Gap: When Reports Lack Mathematical Proof of Existence

The most dangerous compliance failure is not the one that gets reported. It is the one quietly corrected before anyone notices.

Consider a hypothetical: a stablecoin issuer experiences a 48-hour period where reserves temporarily dip below the required 1:1 ratio due to a liquidity event in the underlying asset markets. By the time the monthly attestation report is due, the reserves have been restored. The issuer publishes the report, which accurately reflects the current state, but the snapshot date falls during the undercollateralized period. The report looks clean. The problem has been erased from the record.

This is the post-dating problem, and it's not a theoretical edge case. Without an independent, cryptographically verifiable timestamp anchoring the report to its actual creation date, there is no mechanism to detect this kind of retroactive manipulation.

The limitations of centralized infrastructure compound the risk. Web servers record "Last Modified" headers, but server administrators control those. File system metadata can be altered with basic tools. Even document management systems with internal audit logs share the same fundamental flaw: the entity controlling the system controls the timestamps. A regulator examining a document cannot distinguish between a report filed on time and one backdated to appear compliant.

FATF guidance on virtual asset service providers emphasizes verifiable record-keeping precisely because centralized records are inherently manipulable by those with access. Regulatory supervisors are acutely aware of this vulnerability, and their skepticism is well-founded.

The "silent update" problem is equally serious. An issuer might publish a compliant report, then, without announcement, replace the PDF at the same URL with a revised version that corrects an embarrassing disclosure. Unless a regulator or market participant happened to download and store the original, the revision is effectively undetectable. No notification required. No version history maintained. The public record simply gets overwritten.

If you're building a MiCA-compliant disclosure workflow, understanding how blockchain proof of existence works in practice is the starting point for closing this integrity gap. Cryptographic anchoring solves a problem that no amount of internal policy or procedural controls can fully address.

Blockchain Timestamping: Creating an Immutable Fingerprint for MiCA Compliance

The solution to the integrity gap is mathematically elegant and operationally straightforward: create a cryptographic fingerprint of the attestation document the moment it is finalized, then anchor that fingerprint to a public blockchain.

Here is how it works in practice.

Step 1, Hashing the document. When an attestation report is complete, a SHA-256 cryptographic hash is computed from the document's binary content. This hash is a fixed-length string, 64 hexadecimal characters, mathematically unique to that exact version of the document. Change a single character anywhere in the file, and the hash changes entirely. Critically, the hash reveals nothing about the document's content. It's a fingerprint, not a copy.

Step 2, Anchoring to the blockchain. The hash is submitted to a blockchain timestamping service, which aggregates multiple hashes and embeds them into a transaction on a public blockchain, Bitcoin, Ethereum, or both. Once confirmed, the hash is permanently recorded in a block carrying the blockchain's own immutable timestamp: the block's creation time, validated by global network consensus.

Step 3, Generating the certificate. The timestamping service issues a verifiable certificate linking the document hash to the specific blockchain transaction. Anyone with access to the public blockchain can independently verify this certificate, with no reliance on the issuer, the auditor, or the timestamping provider required.

That last point is the critical differentiator. A blockchain-based timestamp is provider-independent. If the issuer goes bankrupt, if the timestamping service shuts down, if the auditing firm dissolves, the proof remains permanently accessible on the public blockchain. The trusted timestamping infrastructure underpinning this approach has been validated by over a decade of peer-reviewed academic research.

For stablecoin issuers operating under MiCA, this means every attestation report can carry a mathematically provable assertion: this document, in exactly this form, existed at this precise moment in time. No administrator can alter that record. No server migration can corrupt it. No legal dispute can credibly challenge it.

To be precise about what timestamping does and does not do: it does not validate the auditor's methodology, confirm that reserves are sufficient, or replace the qualitative judgment of a licensed attestation practitioner. What it does is create an immutable integrity layer around the disclosure process itself, ensuring that the document regulators examine is provably the same document that was filed, unaltered, at the stated time.

For financial institutions already investing in blockchain-based compliance infrastructure, OriginStamp's tamper-proof timestamping for financial data provides the technical foundation for this level of evidentiary rigor.

Strengthening Financial Reporting with Unbreakable Data Integrity

Regulatory examinations are expensive. Producing historical records, demonstrating document integrity, and satisfying auditor inquiries about disclosure timelines consumes significant legal and compliance resources. For stablecoin issuers operating across multiple EU jurisdictions, that cost compounds rapidly.

An audit-ready system is one where every historical disclosure can be instantly verified without manual reconstruction of records. When a regulator asks "prove that this report was published on this date and has not been modified since," the answer should take seconds, not weeks of forensic investigation.

Tamper-proof audit trails built on blockchain timestamping reduce this friction at every point in the compliance lifecycle:

- During routine examination: Regulators independently verify document integrity without requesting internal records from the issuer

- During enforcement proceedings: Timestamped evidence is cryptographically robust and carries evidentiary weight that internal logs simply cannot match

- During due diligence: Institutional investors and counterparties verify the complete history of reserve disclosures without relying on issuer representations

The institutional trust implications are significant. As ISO 27001 information security standards establish, the integrity of information management systems is foundational to organizational trustworthiness. For stablecoin issuers competing for institutional capital, mathematically provable evidence of disclosure timelines is a competitive differentiator, not merely a compliance checkbox.

Swiss-standard data integrity practices, built on cryptographic proof, independent verification, and long-term immutable archiving, represent the benchmark for financial operations that must withstand scrutiny across multiple regulatory regimes simultaneously. This is particularly relevant for issuers seeking authorization in Switzerland, where FINMA's regulatory framework for digital assets demands a comparable level of technical rigor.

The connection between MiCA stablecoin reserve attestations and broader financial data integrity is direct. Institutions that build tamper-evident disclosure infrastructure now will be better positioned for the inevitable tightening of ESMA's supervisory expectations as MiCA implementation matures. Those relying on centralized, manually managed records will face increasing scrutiny and increasing cost.

Implementation: Integrating Timestamps into the Disclosure Workflow

Most companies get this wrong. Implementing blockchain timestamping for MiCA reserve attestations doesn't require a wholesale technology overhaul, yet teams routinely treat it as an afterthought rather than a workflow design decision. The integration fits into existing disclosure workflows with minimal disruption when you plan it correctly from the start.

Automating the timestamp at report finalization. The most operationally robust approach is API-based automation. When the attestation report reaches its final, signed state, before transmission to regulators or public publication, a timestamping API call triggers automatically. The document hash is computed, submitted to the blockchain, and a certificate returned. The entire process takes seconds and requires no human intervention.

The automation point matters. Timestamping a document after publication introduces a window during which the document could theoretically be altered. Timestamping at finalization, the moment the auditor and issuer agree the report is complete, closes that window entirely. This aligns with BSI guidelines on electronic time-stamping for legally significant documents.

Public hosting of the blockchain certificate. Publish the timestamping certificate alongside the PDF report, not buried in internal systems. Stakeholders, regulators, and market participants should be able to verify document integrity independently, without requesting access to internal records. A simple verification link or QR code embedded in the report publication page achieves this.

Multi-signature acknowledgment. For maximum evidentiary robustness, both the issuer and the independent auditor should timestamp the finalized report independently. This creates a two-party cryptographic record: the auditor confirms the report reflects their findings at a specific moment, and the issuer confirms publication of that exact document. Any subsequent discrepancy between the two timestamps would itself be evidence of a problem.

Long-term archival strategy. MiCA requires record retention for a minimum period following a token's authorization. The principles behind immutable audit trail management for regulated documents apply directly here: every document version preserved, every timestamp verifiable, every access logged.

Historical archives of timestamped attestations become a strategic asset over time. They demonstrate a pattern of consistent, timely disclosure, evidence that regulators value and institutional investors rely upon when evaluating a stablecoin issuer's credibility. The same tamper-evident principles apply directly to maintaining the integrity of MiCA white paper disclosures, where foundational token issuance documents face identical manipulation risks.

Conclusion: Future-Proofing Stablecoin Transparency

MiCA stablecoin reserve attestations represent a significant step forward in regulatory rigor. But the regulation's effectiveness depends entirely on the quality of evidence underpinning each disclosure. A PDF published to a web server, however carefully prepared, is not sufficient evidence of timely, unaltered disclosure. It is a document without a provable history.

Blockchain timestamping bridges the gap between regulatory intent and technical reality. By anchoring the cryptographic fingerprint of each attestation report to public blockchains at the moment of finalization, issuers create evidence that is mathematically immutable, independently verifiable, and permanently accessible, regardless of what happens to any centralized system or service provider.

The legal risk reduction is concrete: post-dating allegations become indefensible, silent update disputes become resolvable, and regulatory examinations become faster and less costly. The market confidence benefit is equally tangible: institutional investors and counterparties can verify disclosure integrity without relying on issuer representations.

The future of MiCA compliance is not just transparent data. It is data whose integrity is mathematically provable. As AI-driven systems increasingly interact with financial records, the importance of cryptographically anchored evidence will only grow.

For stablecoin issuers and financial service providers building compliant disclosure infrastructure, explore how OriginStamp delivers blockchain-grade data integrity for financial institutions and build the evidentiary foundation your MiCA compliance program requires.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.