E-Invoice Archiving: Format, Integrity, and Audit Trails

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

Every year, tax authorities across Europe disallow input tax deductions, not because invoices were fraudulent, but because they were stored incorrectly. The invoice existed. The transaction was legitimate. The archive failed.

This is the real risk hiding inside the e-invoicing mandate. Receiving and sending structured digital invoices is only half the equation. Storing them in a way that satisfies legal, technical, and audit requirements is where most organizations — and the software vendors serving them — fall short.

So why do so many compliance teams discover the gap only when an auditor is already in the room? Usually because "we store our invoices" and "we compliantly archive our invoices" sound identical until the moment they aren't.

This piece breaks down the three foundational pillars of compliant e-invoice archiving: format retention, cryptographic data integrity, and complete audit trails. If you build ERP systems, run compliance infrastructure, or architect SaaS platforms for regulated markets, that distinction matters more than it first appears.

Storage Is Not Compliant Archiving

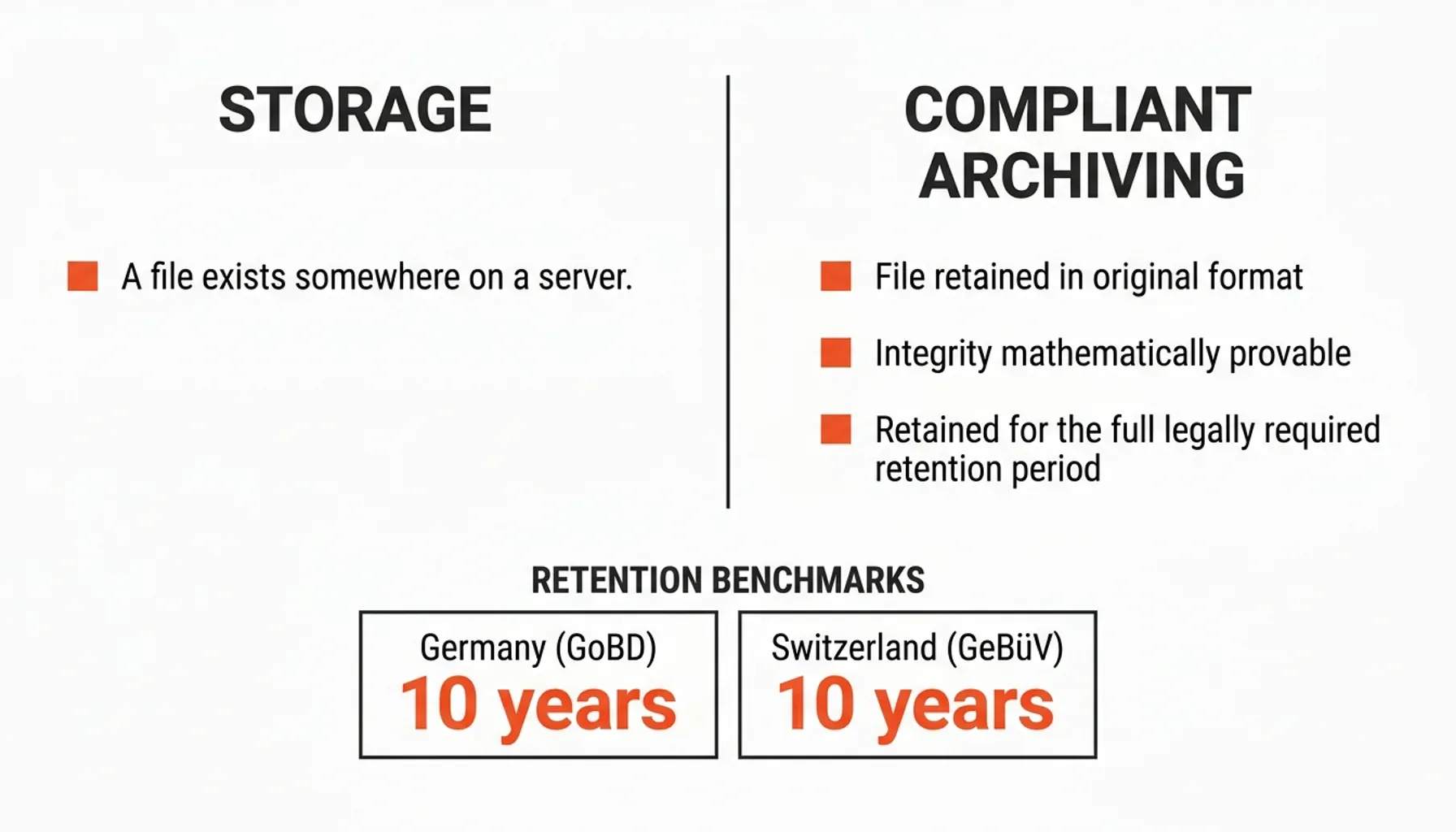

Here is the line that trips people up. Storage means a file exists somewhere on a server. Compliant archiving means that same file is retained in its original format, with its integrity mathematically provable, for the full legally required retention period — ten years under GoBD in Germany, ten years under GeBüV in Switzerland.

The two sound interchangeable in a planning meeting. They are not interchangeable in an audit. A backup folder full of PDFs satisfies the first definition and fails the second, and the difference is exactly what an inspector probes when input-tax deductions are on the line.

Getting it wrong has concrete consequences:

- Tax audits triggered by incomplete or unverifiable archives

- Disallowed input tax deductions when invoice authenticity cannot be proven

- Regulatory fines for failing to meet retention obligations

- Legal exposure in disputes where document integrity is challenged

The mandate itself doesn't end at transmission — it begins there. The EN 16931 e-invoicing standard is now the legal baseline for electronic invoices across EU member states, and national implementations are already live or scaling fast: Germany's XRechnung, France's Factur-X, Italy's SDI. The VAT in the Digital Age (ViDA) framework pushes mandatory cross-border e-invoicing and digital reporting to 2030, but the obligation to keep those invoices correctly is in force the day you receive your first one.

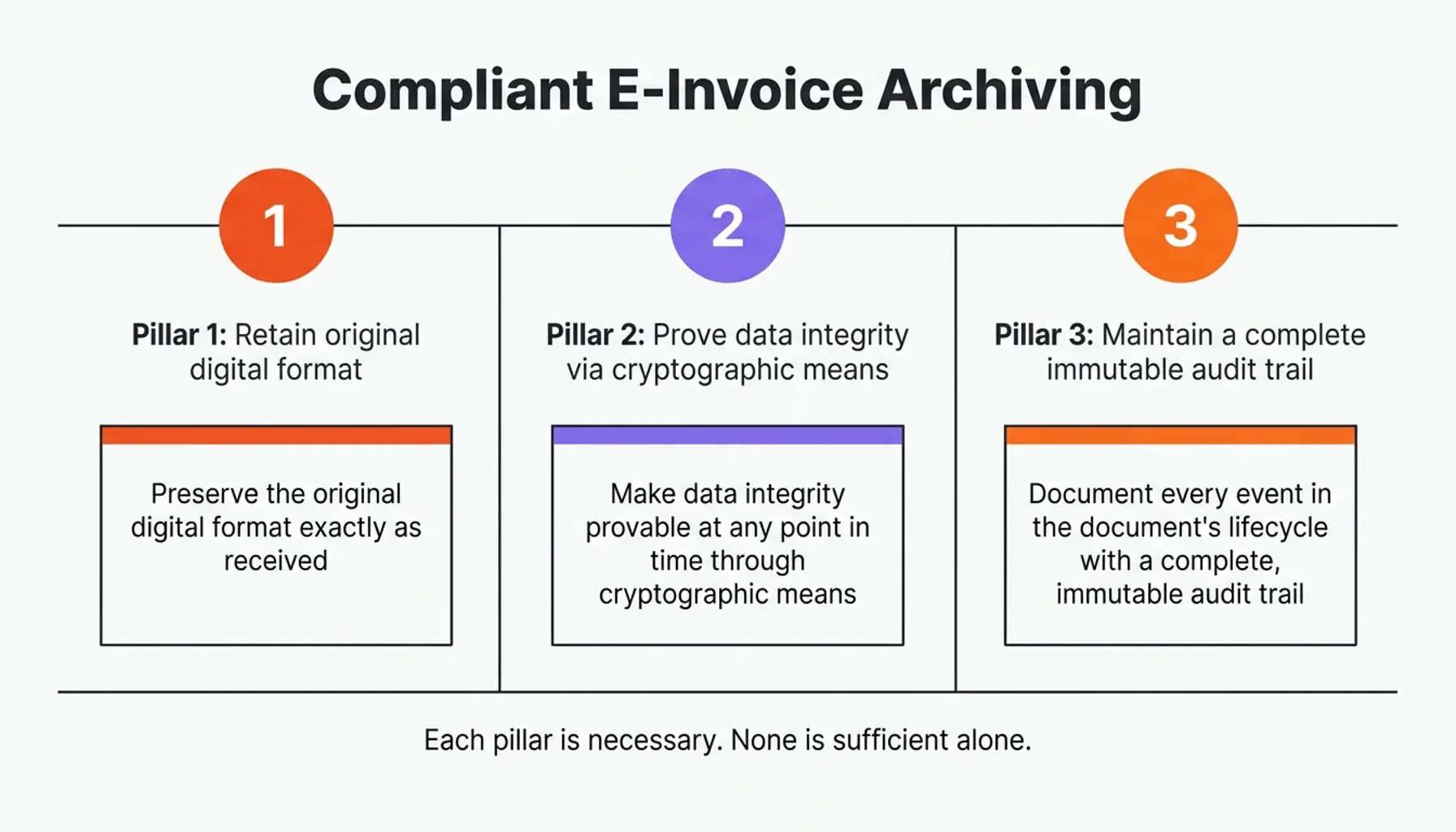

Compliant archiving rests on three pillars, and each one is load-bearing. First, preserve the original digital format exactly as received. Second, make data integrity provable at any point in time through cryptography. Third, document every event in the document's lifecycle with a complete, immutable audit trail. Each pillar is necessary. None is sufficient on its own.

Pillar 1: Retention of the Original Digital Format

A printed PDF of an XRechnung is not a compliant archive. Neither is a PDF/A export of a ZUGFeRD invoice that strips out the embedded XML. This is one of the most common — and most expensive — misunderstandings in the field.

Structured e-invoice formats are fundamentally different from traditional documents. They carry machine-readable data inside standardized XML schemas: supplier identifiers, line-item codes, VAT classifications, payment terms. That data isn't decorative. It's legally relevant, and tax authorities read it directly.

Why the Machine-Readable Source File Must Be Preserved

The FeRD (Forum für Elektronische Rechnungen Deutschland), the body governing ZUGFeRD and Factur-X specifications, is explicit. The structured XML component of a hybrid invoice must be retained in its original, unmodified form. The visual PDF layer alone does not satisfy the legal requirement.

That creates specific obligations for any archiving system:

- Hybrid formats (ZUGFeRD, Factur-X) must preserve both the PDF/A-3 visual layer and the embedded XML data stream

- Pure XML formats (XRechnung, UBL) must be stored as received, with no transformation or normalization applied

- Metadata — creation timestamps, sender identifiers, transmission records — must travel with the document rather than being discarded at ingestion

The Format Conversion Trap

Many archiving systems silently convert incoming invoices to a "house format" for easier storage and retrieval. It feels tidy. It is a compliance failure waiting to happen, and it catches teams off guard more often than they expect.

Conversion introduces two distinct risks. The first is metadata loss: fields that exist in the original XML may not map cleanly to the target format, so information gets dropped without anyone noticing. The second is a broken chain of authenticity: once a document has been transformed, you can no longer prove the stored version is identical to what arrived.

The ISO 19005 (PDF/A) standard for long-term archiving addresses format longevity — keeping documents readable across decades — but it does not solve the integrity problem. Format compliance and integrity proof are separate requirements that need separate technical mechanisms.

The baseline rule is simple: archive the original, in the format it arrived, with no silent transformation.

Pillar 2: Integrity That Math Can Prove

Storing the correct format is necessary. Proving it hasn't changed since the moment of archiving is what makes that storage legally defensible.

Integrity here has a precise meaning. It doesn't mean the file looks correct. It means the file is mathematically provable as identical to the version archived at a specific point in time. Any modification — a single flipped byte, an edited metadata field, a tweaked timestamp — has to be detectable. That bar can only be met with cryptography, not with access controls or administrative promises.

The mechanism that delivers it is well understood: a SHA-256 hash computed at ingestion produces a unique fingerprint of the document's exact binary content, and that fingerprint is stored independently so it can be recomputed and compared at any future point. The deeper question — how to keep the proof trustworthy for a full ten-year retention period without depending on a single certificate authority that might be compromised or wound down, and how to defend against the "trusted insider" who can quietly edit an archive they administer — is the subject of its own discussion. Integrity must be proven by math, sealed independently of any single authority, not asserted by whoever happens to hold admin rights. For the cryptographic seal, blockchain-versus-PKI trade-offs, and the administrator paradox in full, see tamper-proof versus secure storage. This is also the foundation of audit-proof document retention: integrity proven by mathematics, not by assurance.

Pillar 3: The Audit Trail That Documents the Lifecycle

An immutable document without a traceable lifecycle is only half an archive. Auditors don't just verify that an invoice exists and is unaltered. They verify what happened to it: when it was received, who accessed it, how it was classified, whether it was linked to the correct business transaction.

This is the audit trail requirement, and it carries as much legal weight as format and integrity combined.

What a Complete Audit Trail Contains

A legally compliant audit trail isn't an access log. It's a structured, immutable record of every event in a document's lifecycle:

- Ingestion event: the timestamp the invoice entered the archive, with the source system identified

- Classification events: when and how the document was categorized and linked to cost centers or projects

- Access events: every instance of a user or system reading or retrieving the document

- Metadata changes: any update to associated data, with the previous value preserved

- Retention decision: when and why a document was flagged for deletion at the end of its retention period

- Export events: any time the document was exported or transmitted

ISACA's framework for financially material systems treats audit trails as a core governance requirement, not an optional enhancement. The Swiss GeBüV framework goes further: trails must be machine-generated rather than manually maintained, and protected from modification.

Linking the Invoice to the Business Transaction

Documenting a file's lifecycle in isolation isn't enough. The invoice must be traceable to the underlying business transaction — the purchase order, the delivery note, the payment record. That linkage is what lets an auditor reconstruct the full transaction chain during an inspection.

It is also where your ERP archive becomes critical. The archiving system has to maintain referential integrity between the invoice and the transactional data in the ERP — not as a manual cross-reference, but as a system-enforced link that survives data migrations, system upgrades, and personnel changes.

Automating the Log

Manual audit trail maintenance is a liability. Any process that depends on a human remembering to record an event introduces gaps, inconsistencies, and the chance of after-the-fact editing.

Compliant archiving requires system-generated, append-only event logs. Every event is written automatically the moment it occurs, and the log itself is protected by the same integrity mechanisms as the documents it describes — hashed, timestamped, and immutable.

Build vs. Buy: Where the Three Pillars Live in Your Stack

For ERP vendors and SaaS providers, these three pillars aren't just a checklist. They are an engineering and operational commitment that has to be owned by someone — and that decision shapes your roadmap.

Building a compliant archiving layer in-house means implementing and maintaining ISO 27001-certified controls, auditing encryption logic, isolating tenants, tracking every format update as standards evolve, and renewing certifications per market. That is an ongoing operational function competing with core product work, not a one-time project — and the full total-cost-of-ownership picture is worth weighing deliberately before you commit, which is exactly what the build-vs-buy decision guide lays out.

The alternative is to embed a pre-certified archiving layer through an API. A platform such as OriginVault's compliant invoice archiving engine handles the pillars as a managed service, and the pattern lets you add new formats and new market certifications at the API layer without re-engineering the ERP core — the integration mechanics are covered in the archiving API guide. For ERP vendors selling into DACH, the same layer can run under your own brand, so the end customer experiences GoBD and GeBüV compliance as a native feature rather than a third-party bolt-on.

When you do evaluate a solution, three questions cut to the heart of the pillars:

- Format-agnostic ingestion. Does it ingest XRechnung, ZUGFeRD, Factur-X, UBL, and EDIFACT without transforming any of them? If a vendor normalizes everything to a single internal format, that is precisely where compliance breaks.

- Independent integrity verification. Can you take any archived document, run your own hash check, and confirm it matches the stored value — without the vendor's tooling? If verification depends on the provider staying in business, that is a trust dependency you don't want across a ten-year retention window.

- Auditor-ready trail output. Request a sample audit trail export in the format an auditor would actually receive. It should be human-readable, machine-parseable, and complete from ingestion to the present. If generating it needs custom configuration or a support ticket, that's a red flag for audit readiness.

On certification itself, don't accept claims at face value: GoBD compliance is never self-declared, and in Germany the IDW PS 880 standard governs the audit of software handling tax-relevant data. Ask for documented third-party sign-off, and for regulated customers in banking, healthcare, or public administration, confirm where data is stored and processed — Swiss-hosted infrastructure offers a legal stability that matters in long-term retention.

Designing for Mandates That Keep Arriving

The e-invoicing rollout across Europe isn't a single event. It's a phased set of mandates that keep landing through the late 2020s, with country-specific timelines and formats — a moving target tracked in the EU mandate timeline, and folded into the broader ViDA reform that brings mandatory e-invoicing and digital reporting to 2030. An archive built only for today's rules will hit compliance gaps within 18 to 36 months unless it is designed for change from the start.

That is the practical case for keeping format support, integrity proof, and audit logging in a layer that can absorb a new standard without forcing a product re-integration each time. Before committing to any solution — built or bought — validate it against the essentials of all three pillars:

Format

- Stores original structured XML without transformation

- Preserves both layers of hybrid formats (PDF/A-3 + embedded XML)

- Maintains all metadata as received

Integrity

- Computes a SHA-256 hash at ingestion, before any processing

- Seals that hash independently of any single authority

- Provides verification that doesn't rely on vendor infrastructure

Audit Trail

- System-generated, append-only event log

- Covers the full lifecycle from ingestion to retention decision

- Links invoice records to underlying ERP transaction data

- Produces human-readable output for auditor review

For vendors weighing where to host that layer, the strategic case for digital sovereignty is worth a read — infrastructure location turns into customer trust in regulated industries, where compliance becomes a feature you can sell rather than a constraint you manage. And if you're still wondering whether a plain PDF cuts it in 2026, the short answer is that it doesn't.

Conclusion

E-invoice archiving isn't a storage problem. It's a trust problem — and trust, in this context, has to be mathematically provable.

Format retention keeps the original structured data exactly as received. Cryptographic integrity proves it hasn't been altered since the moment of archiving. A complete audit trail records every event in the document's lifecycle so it can be verified later. Together, these three pillars define what "audit-proof" actually means for modern e-invoicing compliance, and the distinction between merely storing invoices and properly archiving them is where most teams either pass or fail their next inspection.

For ERP and SaaS vendors, deciding who owns that layer carries real weight: building it in-house is expensive, the certification burden never ends, and the engineering time is diverted from core product. If you're evaluating how to deliver GoBD and GeBüV-compliant invoice archiving under your own brand, OriginVault's white-label e-invoicing archive is built specifically for ERP vendors who need audit-grade document retention without standing up the compliance infrastructure themselves.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.