What Is EN 16931? The EU E-Invoicing Standard Explained

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

The Foundation of European Digital Trade: Understanding EN 16931

A PDF invoice is not an electronic invoice. That distinction, still misunderstood by thousands of finance teams across Europe, is precisely what EN 16931 was designed to resolve.

Consider what that misunderstanding costs in practice. In 2023, a mid-sized German manufacturer sent 4,200 invoices to a federal contracting authority as PDF attachments. Every one was rejected. The accounts receivable team spent six weeks manually re-keying data into XRechnung-compliant XML, delaying €1.2 million in payments and triggering a late-delivery penalty clause. The root cause was not a software failure. It was a misunderstanding of what "electronic invoicing" legally means under EN 16931.

EN 16931 is the European semantic data model for electronic invoicing, published by the European Committee for Standardization (CEN) and mandated by Directive 2014/55/EU. It defines, with mathematical precision, exactly what information a valid electronic invoice must contain: buyer and seller identifiers, VAT breakdowns, line item details, payment terms, and how that information must be structured so that any compliant system can read it without a human in the loop.

Before EN 16931, "e-invoicing" often meant emailing a PDF. A person still had to read it, type the numbers into an ERP, and hope for no transcription errors. The standard ends that by mandating machine-readable, structured data, formats that accounting software can ingest, validate, and process on its own.

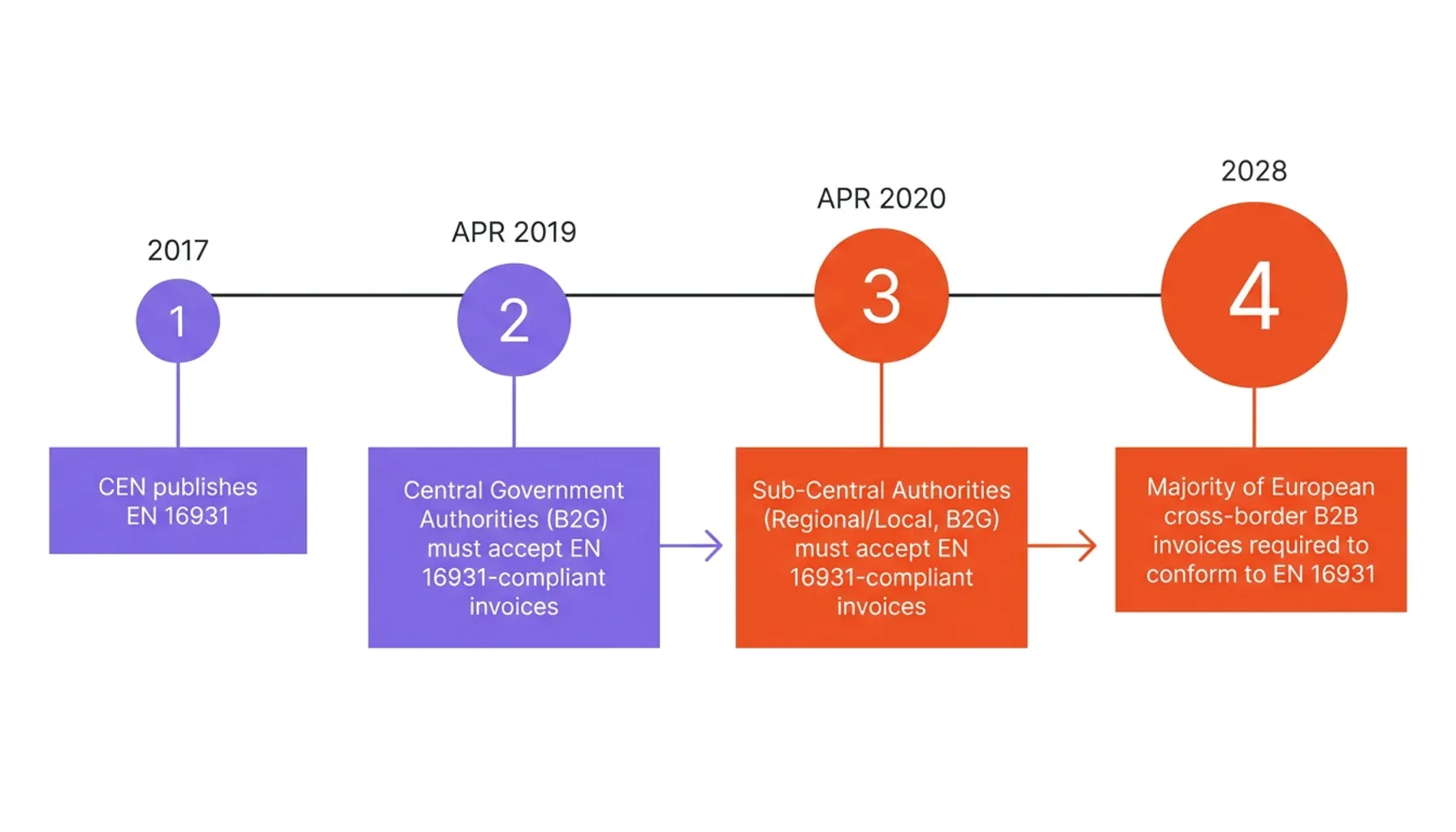

The standard became legally binding for European public procurement in April 2019. Every contracting authority in the EU must now accept invoices conforming to EN 16931 for B2G (business-to-government) transactions. That obligation is now expanding into B2B through the EU's VAT in the Digital Age (ViDA) reform and national mandates in Germany, France, Italy, and Poland. For most European businesses, the question is no longer whether to implement EN 16931, but how fast and how completely.

What EN 16931 Actually Is, and Why Directive 2014/55/EU Made It Mandatory

EN 16931 is a formal European standard, not a software specification or a government IT project. CEN published it in 2017 in direct response to Directive 2014/55/EU, which required all EU member states to accept electronic invoices in public procurement. The Directive did not prescribe a single format. It required a common semantic standard that multiple formats could implement, and EN 16931 is that standard.

The Directive set two compliance deadlines: central government authorities had to accept EN 16931-compliant invoices by April 2019, and sub-central authorities (regional and local governments) by April 2020. Both deadlines have passed. Non-compliance by a contracting authority is a breach of EU law, with no grace period remaining.

The Core Invoice Semantic Data Model

The heart of EN 16931 is its core invoice semantic data model: a precisely defined set of 156 business terms organized into logical groups. These are not field names in a database schema. They are semantic concepts with unambiguous definitions that hold regardless of the syntax used to encode them.

Each term carries a stable identifier. BT-1 is the invoice number. BT-5 is the invoice currency code. BG-25 is the group that holds every invoice line item, and each line nests its own terms (BT-126 line identifier, BT-129 invoiced quantity, BT-146 item net price). That numbering is the backbone of the whole standard: when two systems both speak "BT-31", they agree on what a seller VAT identifier is, with no further negotiation.

The key business term groups include:

- Process and invoice identifiers: invoice number (BT-1), issue date, invoice type code, currency, and the process identifier that tells the receiving system how to handle the document.

- Seller information: legal name, postal address, VAT identifier, tax registration number, and electronic address.

- Buyer information: name, address, VAT identifier, buyer reference (often a purchase order number or cost-centre code), and electronic address.

- Delivery information: delivery date, delivery location, and the period of supply where applicable.

- Payment instructions: payment means code, payment due date, IBAN, and remittance information.

- VAT breakdown: for each applicable VAT rate, the taxable amount, VAT rate, VAT amount, and the VAT category code (standard, zero-rated, exempt, reverse charge, and so on).

- Invoice line items (BG-25): line identifier, item name, quantity, unit of measure, net price, line VAT information, and line net amount.

Each term carries a cardinality, mandatory, conditional, or optional, plus business rules that constrain its allowed values. The standard defines more than 80 such rules: cross-field validations that enforce internal consistency. The sum of line net amounts, for instance, must equal the invoice total before VAT, and the VAT breakdown must account for every taxable line. Break a single rule and the whole invoice fails.

The distinction between terms and groups matters in practice. A business term (BT) is a single value, BT-1 invoice number, BT-9 payment due date, BT-112 invoice total with VAT. A business group (BG) is a repeatable container that bundles related terms: BG-25 wraps each invoice line, so a ten-line invoice repeats BG-25 ten times, while BG-23 holds one VAT breakdown subtotal per rate. Cardinality is attached at both levels. A buyer reference (BT-10) is optional in the core model but a whole CIUS can elevate it to mandatory, which is exactly how national rules tighten the standard without rewriting it.

This semantic precision is what makes EN 16931 interoperable. A "seller VAT identifier" means the same thing in a German ERP as in a Portuguese government portal, because the standard defines it once, unambiguously, at the semantic level.

Scope and Boundaries

EN 16931 covers commercial invoices and credit notes for the supply of goods and services. It does not cover:

- Order documents or despatch advice (these fall under other CEN standards in the BII suite)

- Payroll or internal accounting documents

- Consumer-to-business transactions (B2C is explicitly out of scope)

- Invoices below national thresholds in jurisdictions that apply them

The standard applies to both B2G and B2B contexts, though legal mandates currently enforce it most strictly in B2G. The B2B expansion is underway and gaining pace through national legislation and ViDA.

What Happens When You Get It Wrong

Rejection is the least painful consequence. A rejected invoice triggers a manual correction cycle: re-keying data, resubmitting through the correct channel, waiting for reprocessing. At scale, that cycle consumes accounts receivable capacity that should be generating cash, not fixing errors.

The more serious risk is audit exposure. If your archived invoices do not conform to EN 16931 semantics, tax authorities in Germany, France, and Italy can challenge their legal validity during a VAT audit. An invoice that cannot be validated against the standard may not be accepted as evidence of a deductible expense. That is not a processing inconvenience, it is a tax liability.

Semantic vs. Syntactic: How the Standard Actually Works

Understanding EN 16931 means separating two concepts that are routinely conflated: semantics and syntax.

The Semantic Layer

The semantic layer defines what information must exist in an invoice. It specifies those 156 information elements organized into groups: process and invoice identifiers, the seller's postal address and VAT number, the buyer's reference, delivery details, payment instructions, VAT breakdowns, and individual line items.

This layer is intentionally format-agnostic. The standard does not care whether you use XML, JSON, or any other encoding. It cares that the right data is present, correctly labeled, and unambiguous.

The Two Permitted Syntaxes

While the semantic model is format-neutral, EN 16931 permits exactly two XML syntaxes for compliant implementation:

- UBL 2.1 (Universal Business Language, maintained by OASIS Open): widely used in the Nordic countries, the Netherlands, and the Peppol network.

- UN/CEFACT CII (Cross Industry Invoice): preferred in Germany (via ZUGFeRD/Factur-X) and France.

Both syntaxes carry the same semantic payload, and a compliant receiving system must process either one. A ram:SellerTradeParty element in CII and a cac:AccountingSupplierParty element in UBL are two spellings of the same EN 16931 concepts (BT-27 seller name, BT-31 seller VAT identifier). The wording differs; the meaning is identical. This is what makes EN 16931 a genuine interoperability standard rather than a vendor-specific format, and it is why a system built around the semantic model can validate either syntax without format-specific business logic.

The Factur-X/ZUGFeRD family makes the same point in hybrid form: it maps its CII XML directly onto EN 16931's 156 business terms, so the semantic layer does the validation while the file format is merely the container. The full format mechanics, the PDF/A-3 embedding, and the five conformance profiles are covered in the dedicated Factur-X and ZUGFeRD format guide.

CIUS and Extensions

No single standard can anticipate every national tax requirement. EN 16931 handles this through a layered architecture:

- Core Invoice Usage Specifications (CIUS) are national or sector-specific restrictions that narrow the core standard. They can make optional fields mandatory or restrict allowed values, but they cannot contradict the core.

- Extensions allow additional data elements required by specific use cases (construction-sector payment schedules, public-sector project codes) without breaking interoperability. A receiving system simply ignores the extension elements it does not recognise and still processes the core data.

This architecture is why XRechnung, Factur-X, and Peppol BIS Billing can coexist: they are all EN 16931-compliant implementations of one core, not competing standards.

The practical implication for software vendors is that you do not need to build a separate invoicing engine for each European country. You need one semantic core and several syntax renderers. That is a far more efficient architecture, but only if your infrastructure is designed for it from the start.

Schematron Validation: The Enforcement Mechanism

The standard does not rely on goodwill for enforcement. CEN publishes official Schematron rule sets, machine-executable validation scripts, for both UBL 2.1 and UN/CEFACT CII. Any compliant receiving system runs these rules against every incoming invoice before accepting it.

Schematron validation catches two categories of error. The first is structural: a mandatory field is absent or malformed. The second is semantic: field values are internally inconsistent, for example a VAT amount that does not match the declared rate applied to the taxable base. Both categories result in rejection, and both are entirely preventable when you validate before transmission rather than after.

How EN 16931 Shows Up in Real Formats and Networks

EN 16931 provides the blueprint; national formats and delivery networks provide the building. Three of them carry the bulk of European invoice traffic, and not one is a plain PDF. Each is simply a CIUS or transport layer wrapped around the same semantic core.

- XRechnung is Germany's pure-XML CIUS of EN 16931, with German-specific additions such as the Leitweg-ID routing identifier. When to choose it over the hybrid alternative is the subject of the XRechnung vs ZUGFeRD comparison, and its place in the national rollout is covered by the German B2B e-invoicing mandate guide.

- Factur-X / ZUGFeRD is the hybrid format that embeds EN 16931 XML inside a human-readable PDF/A-3, jointly maintained by France's FNFE-MPE and Germany's FeRD. Its profiles and embedding mechanics live in the Factur-X format guide.

- Peppol BIS Billing 3.0 carries EN 16931 semantics over the Peppol network using UBL 2.1 as its syntax, governed by the official German XRechnung specification for the national variant. How the four-corner network actually moves a document is explained in the Peppol network guide.

For an ERP or accounting vendor, the takeaway is architectural rather than country-by-country: support the EN 16931 semantic model once, render it to XRechnung or Factur-X for national delivery, and ship it over Peppol for cross-border transmission. These are not three separate problems but one semantic model with three output channels.

The same logic applies to keeping those invoices once they are issued. If your platform needs to retain EN 16931 documents in their original format with verifiable integrity, OriginStamp's e-invoicing archiving handles all three format variants behind one API.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.