Is a PDF Still a Valid Invoice in 2026? The New Reality

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

Is a PDF Still a Valid Invoice in 2026? The New Reality

Imagine your accounts payable team flags a €40,000 VAT deduction as invalid. The invoice looks fine. It's a PDF. That's the problem.

This scenario is no longer hypothetical. In 2026, a standard PDF invoice, the kind millions of businesses still send every day, is no longer legally recognized as an electronic invoice under the B2B mandate in Germany and across the EU. The consequences are concrete: rejected input VAT deductions, failed compliance audits, and supplier invoices your own auditor refuses to accept. This article explains exactly what changed, how to tell whether the PDF on your screen actually qualifies, and what it means for the way you send and receive invoices.

When a PDF Stops Being an Invoice: What 2025/2026 Changes

Most companies get this wrong. There is a widespread assumption that any invoice delivered digitally qualifies as an "electronic invoice." It does not. The B2B e-invoicing mandate, introduced in Germany under the Wachstumschancengesetz and effective January 1, 2025, draws a hard line: an electronic invoice must contain structured, machine-readable data, not just a picture of one.

Think of it this way. A PDF invoice is like a photograph of a spreadsheet. You can see the numbers, but you cannot sort, filter, or audit them. The structured e-invoice standard, EN 16931, requires the spreadsheet itself, encoded so a machine reads it without a human in the loop.

That distinction is the whole game. A standard PDF is a visual document. A person can read it; software cannot reliably pull the buyer, seller, line items, and tax amounts out of it as data. Tax authorities and auditors need invoices that can be processed, validated, and verified automatically, and a scanned or image-based PDF fails that test entirely. Drop a paper invoice through a scanner, run OCR over it, and you still have pixels with a confidence score attached, not a guaranteed field structure. The numbers a validator reads might be the numbers on the page, or they might be an OCR misread of an 8 as a 3. There is no way to prove which, and "probably correct" is not a basis for a VAT deduction.

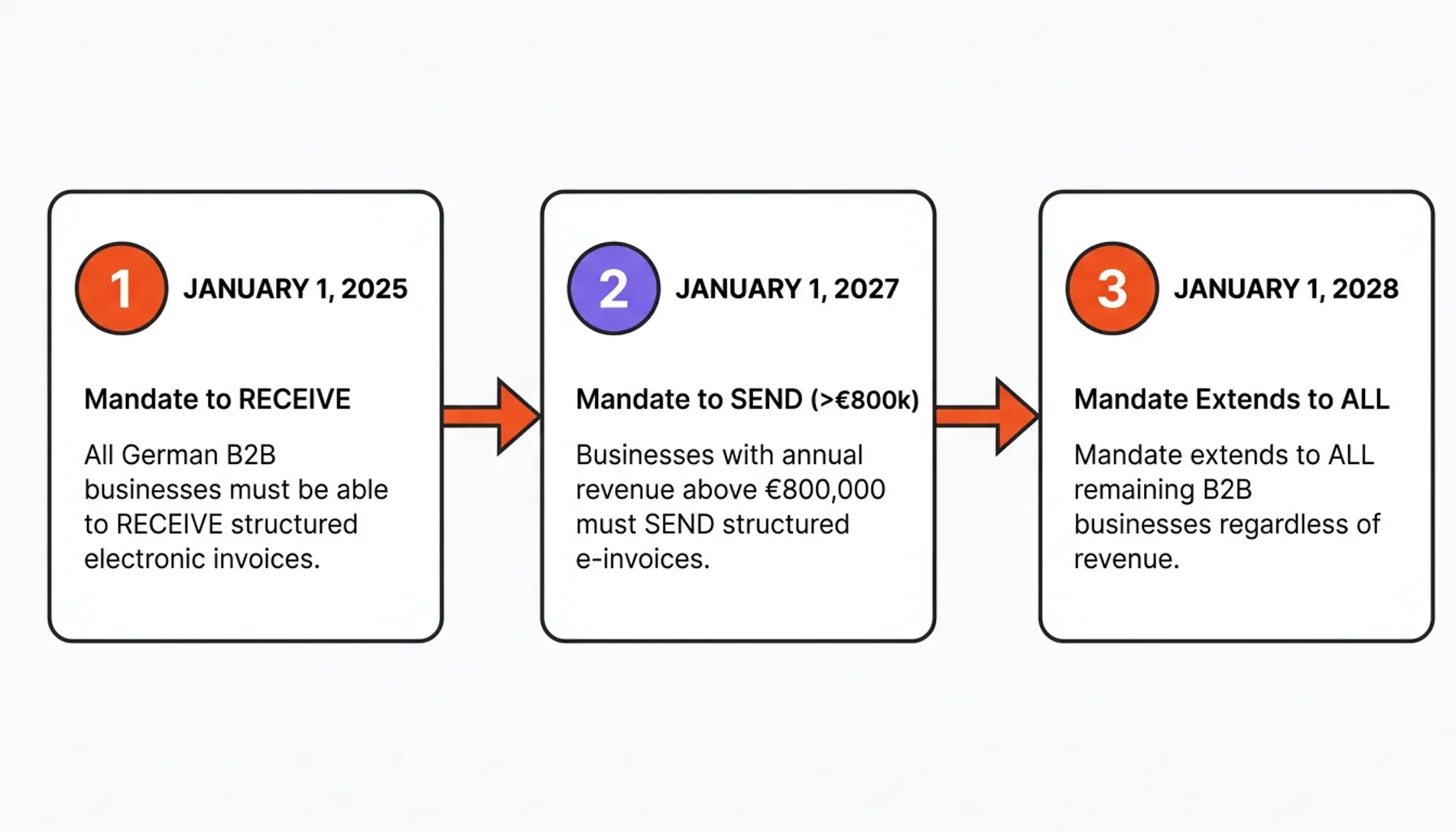

The timeline matters:

- From January 1, 2025: All German B2B businesses must be able to receive structured electronic invoices.

- From January 1, 2027: Businesses with annual revenue above €800,000 must send structured e-invoices.

- From January 1, 2028: The mandate extends to all remaining B2B businesses regardless of revenue.

The receiving obligation is live now. The sending countdown has started. So the trap is already sprung on the receiving side: if a supplier sends you a plain PDF and you claim input VAT based on it, your deduction can be challenged or denied, no matter how clean the PDF looks. EU Directive 2014/55/EU set the legal foundation for this shift years ago. Enforcement is what's new.

Is Your PDF Actually an E-Invoice? A 30-Second Test

Here is the part most people skip: a file with a .pdf extension can be a fully compliant e-invoice, or a worthless visual, and they look identical on screen. The difference is hidden inside the file.

A structured invoice that meets EN 16931 carries its data in machine-readable XML. Hybrid formats like ZUGFeRD and Factur-X embed that XML inside the PDF, so the same file shows a human-friendly page and hands software the structured layer underneath. A plain PDF has the page and nothing else. You can run the check yourself in under a minute:

- Open the file and look at its attachments. Most PDF readers list embedded files in a sidebar or attachments panel. A compliant ZUGFeRD/Factur-X invoice shows an attached XML (commonly named

factur-x.xml,zugferd-invoice.xml, orxrechnung.xml). No attachment means no structured data, which means it is not an e-invoice. - Try to select the total as text. If the amounts are part of a scanned image, your cursor won't grab them. That is an image-only PDF, the weakest possible format for compliance.

- Ask where the numbers come from. If your accounts-payable workflow reads figures off the rendered page rather than from an embedded XML field, you are treating a picture as a source of truth.

If you need to choose which structured format to send, XRechnung versus ZUGFeRD covers pure-XML against hybrid, and the mechanics of the hybrid container are laid out in the Factur-X format guide. For the purposes of this article, the takeaway is simpler: if there's no XML in the file, you do not have a valid e-invoice, you have a digital photograph.

Why Manual Re-Keying Is Now a Compliance Failure

This is the point that catches finance teams off guard. Re-typing invoice data from a PDF into your ERP is no longer just inefficient, it breaks compliance.

When a clerk reads a PDF and re-keys the net amount, VAT rate, and line items by hand, three things happen. Human error enters the record. Validation slips downstream, after the data has already been altered. And the chain between what the supplier actually issued and what your system stored is severed, because there is no structured original to reconcile against. The page your clerk read and the figures they entered are now two separate artifacts with nothing binding them together.

Picture what an auditor sees. With a structured invoice, they open the embedded XML, run it through a validator, and confirm in seconds that the seller VAT ID, tax breakdown, and totals match what was processed and archived. With an image-only PDF, there is no XML to validate against, so the auditor falls back to questions: Where did this figure come from? Who typed it? How do you know it matches the supplier's original? Every one of those questions is a place where a deduction can unravel. The structured file answers them before they're asked; the photograph cannot answer them at all.

The Forum for Electronic Invoicing Germany (FeRD) has been consistent on this: in a hybrid invoice, the XML component is the legally binding record. The PDF view is a courtesy. Relying on it exclusively is a compliance risk with direct financial consequences.

The VAT Trap: What 'Just a PDF' Costs You

The financial stakes are not abstract. Under the revised German VAT framework, shaped by the Wachstumschancengesetz and the broader VAT in the Digital Age reform (ViDA at the European Commission), tax authorities are gaining the technical capability to cross-reference invoice data at scale. A plain PDF creates a data gap that auditors can and will exploit.

The core risk lands on input tax deduction. A business that receives a non-compliant invoice and claims VAT based on it carries the burden of proving the invoice was legitimate. If the format does not meet the structured-data requirement once the mandate applies, that deduction is exposed. The financial damage compounds across thousands of invoices, not one.

The transition periods offer some breathing room, but they are finite:

- Until December 31, 2026: Plain PDFs and paper invoices remain temporarily acceptable for sending (not receiving) under certain conditions.

- After January 1, 2027: The grace period ends for large billers. Structured XML becomes mandatory for sending.

Here's the catch. "Temporarily acceptable" is not "without risk." Authorities still scrutinize archiving quality, data integrity, and audit trails during the transition. A PDF sitting in a shared drive, with no integrity record and no structured data layer, is a weak position today, not only in 2027. Once you do hold a compliant hybrid invoice, it has to stay intact: the file must be archived in its original PDF/A-3 form with the embedded XML preserved, unaltered, for the full retention period. The detail of those archiving rules belongs to that guide and to the GoBD requirements for e-invoices, which trace back to the German finance ministry's GoBD principles; for the sender and recipient, the rule of thumb is short: keep the XML, don't convert the file, and be able to prove it hasn't changed. Demonstrating that a stored invoice is unaltered across years is exactly where tamper-proof storage differs from ordinary secure storage, and where blockchain-anchored integrity proof earns its place.

What This Means If You Build Invoicing Software

For ERP and accounting-software vendors, the practical impact is direct: your invoice output has to produce valid structured XML, and your archive has to preserve that XML rather than only the PDF rendering of it. Customers are already asking whether your platform handles structured formats and whether their archived invoices will survive a tax audit. If the answer needs a long explanation, you're losing deals.

That leaves a build-or-buy decision. Standing up a compliant archive in-house means owning cryptographic integrity, write-once storage, audit logging, and format validation, and keeping all of it stable through software updates and regulatory change. The build-versus-buy trade-off for a compliant e-invoice archive walks through the real cost, and the white-label route for software vendors shows how to ship an audit-grade archiving layer under your own brand instead. If you'd rather embed a ready integrity layer than build one, OriginVault's e-invoicing archiving handles structured-data preservation and tamper-evident sealing inside your product.

Action Plan: Getting Your Invoices Ready

The path is sequential. Here is where to start.

Step 1: Audit Your Invoice Output

Does your invoice generation produce embedded XML? Run the test from earlier: open a standard invoice PDF and inspect its attachments. No embedded XML means you are issuing a visual-only invoice, and that output has to change before you hit the 2027 sending mandate. Validate the XML against EN 16931 with one of the publicly available validators. If it fails schema validation, that is your first fix.

Step 2: Validate How You Store Them

Can your archive ingest, store, and retrieve the full PDF/A-3 file with the XML intact? Does it log every access and change? Can you produce a tamper-evident trail for a specific invoice on demand? If any answer is "no" or "we'd have to check," the archive is not ready. The distance between "we store invoices" and "we store invoices in a compliant, integrity-verified archive" is wide, and auditors know precisely which questions expose it.

Step 3: Fix the Receiving Side First

The receiving mandate is the one already in force, so it's the more urgent gap. Make sure your team can accept and read a structured invoice without re-keying it. Route the embedded XML into your ERP as the source of truth and keep the PDF view as the human-readable copy, not the record. Every invoice you re-type by hand is a deduction you may have to defend later.

The France 2026 e-invoicing mandate is moving on a parallel track, which underlines that this is a pan-European shift rather than a German quirk. Building for structured invoices once, cleanly, beats patching each jurisdiction as its deadline arrives.

The Bottom Line

A plain PDF is a picture of an invoice, not the invoice itself. In 2026 that difference decides whether your input VAT survives an audit and whether the documents you send count at all. The receiving mandate is live; the sending countdown has started; the fix cannot be retrofitted the week before a deadline.

So the test is worth running today on the invoices already moving through your business: open one, look for the embedded XML, and ask whether your team is reading data or reading a photograph. If it's a photograph, you don't have an e-invoice yet, and now you know exactly what to change.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.