What Is ViDA? The EU VAT in the Digital Age Reform Guide

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

The EU Is Rewiring VAT. Here's What Every Finance and Tech Leader Needs to Know.

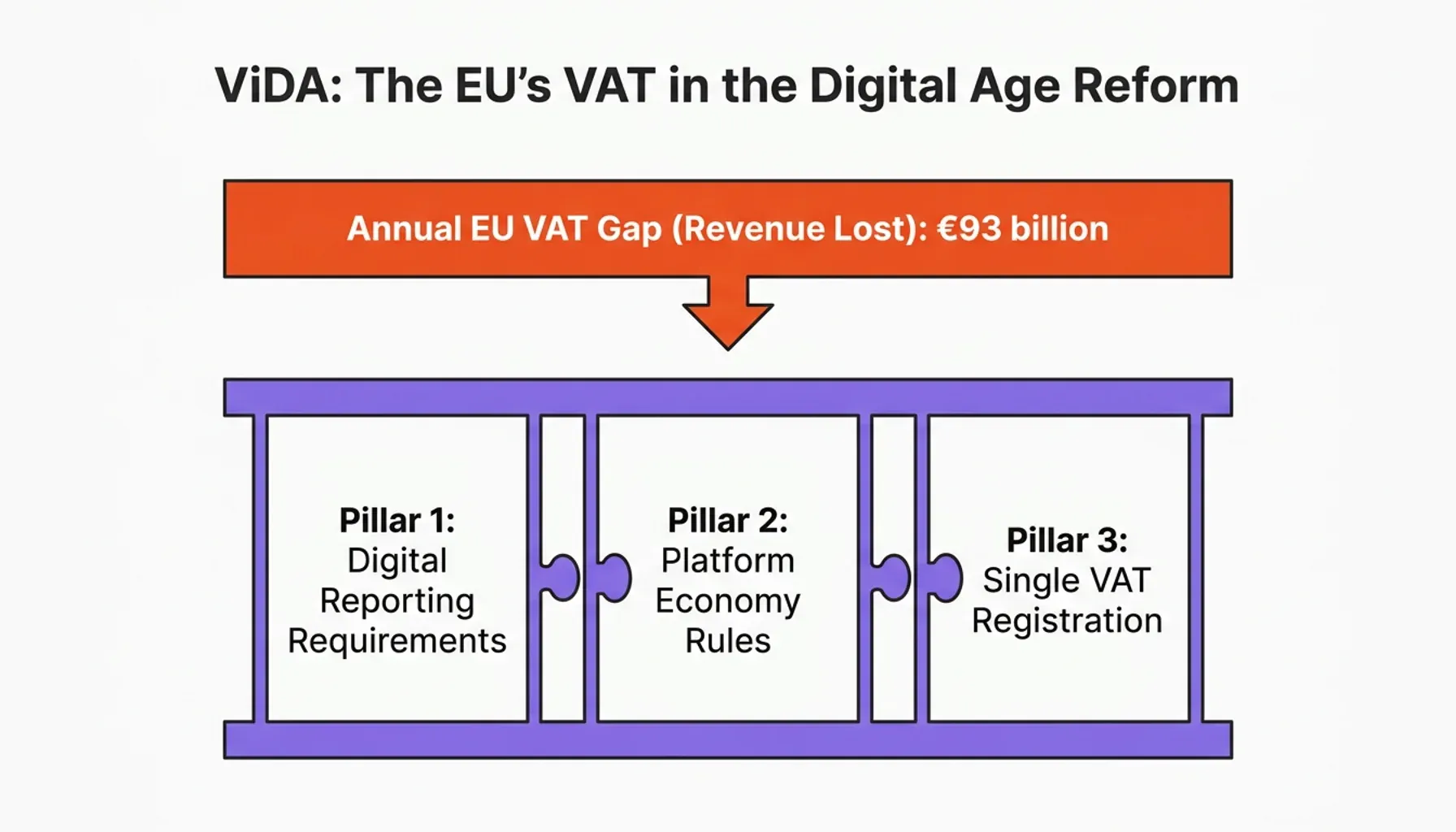

A €93 billion annual VAT gap does not fix itself. That is the scale of VAT revenue the European Union loses every year through fraud, evasion, and systemic inefficiency. The EU's response is not a patch. It is a structural overhaul: VAT in the Digital Age, known as ViDA.

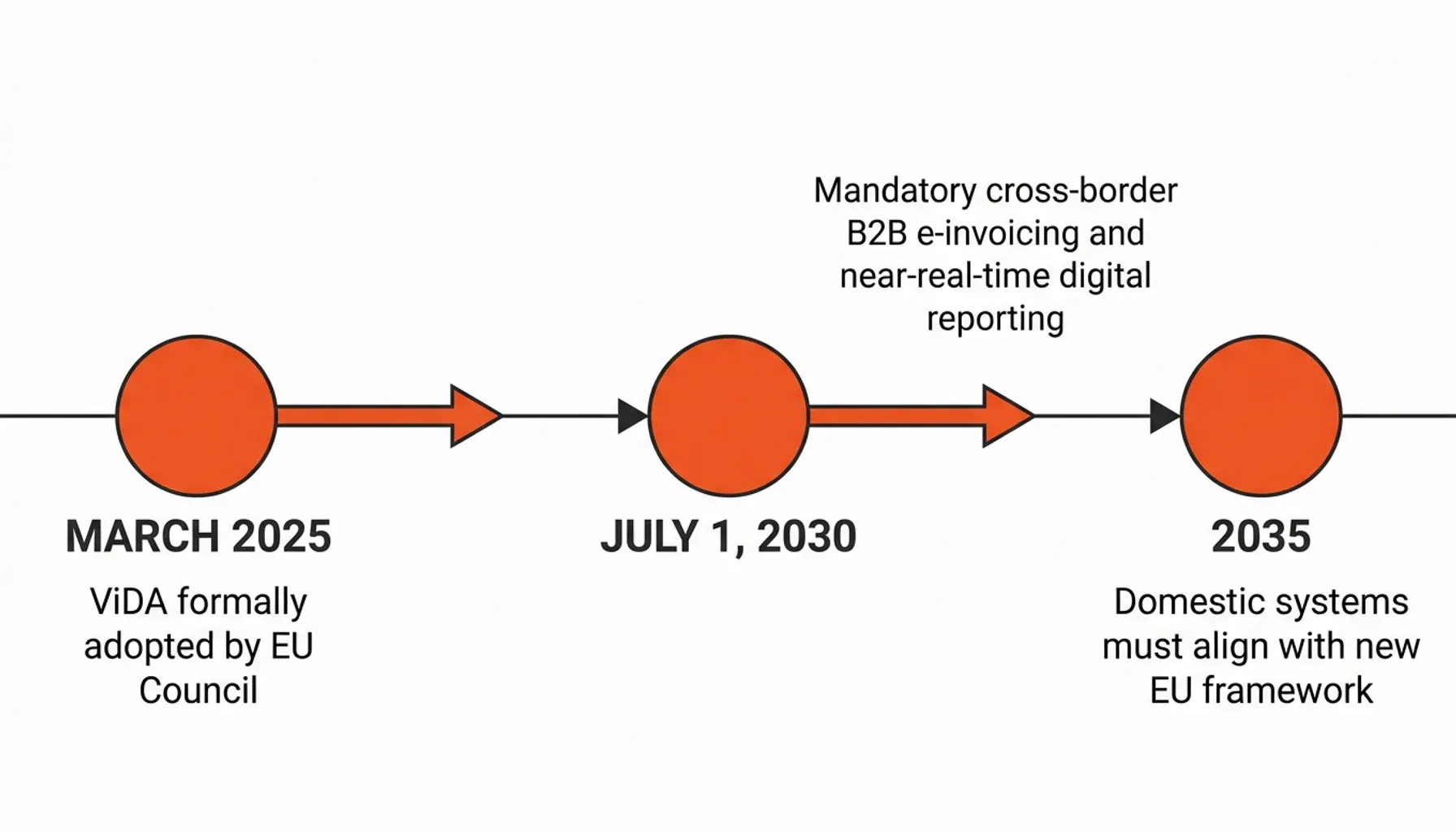

Formally adopted by the EU Council on 11 March 2025, ViDA is the most significant reform to the European VAT system in two decades. It rests on three interlocking pillars: Digital Reporting Requirements, new rules for the platform economy, and a simplified Single VAT Registration system. Together they will change how businesses issue invoices, report transactions, and store financial records across the EU.

The clock is already running. 1 July 2030 is the hard deadline for mandatory cross-border B2B e-invoicing and near-real-time digital reporting. By 2035, domestic systems must align with the new EU framework. For CTOs, CPOs, and ERP vendors operating in European markets, this is not a compliance checkbox. It is an infrastructure decision that needs to be made now.

This guide breaks down every pillar of ViDA, the technical requirements it imposes, and the practical steps organizations need to take to be ready, not just compliant.

The 2030 Mandate: Real-Time Digital Reporting (DRR)

The most operationally disruptive element of ViDA is the shift to transaction-by-transaction reporting, and the speed at which it must happen.

Under today's system, businesses submit periodic recapitulative statements (EC Sales Lists) that summarize cross-border B2B transactions. These summaries land weeks after the fact, and that delay is exactly the blind spot fraudsters have exploited for decades. The classic exploit is missing trader intra-community (MTIC) fraud, also called carousel fraud: goods are traded rapidly across borders, one trader collects VAT from a buyer and then vanishes before remitting it, while the chain reclaims input VAT the state never received. By the time the quarterly summary surfaces, the trader is gone.

ViDA closes that window.

The 10-Day Reporting Window

Starting 1 July 2030, businesses engaged in intra-EU B2B transactions must report each transaction to tax authorities within 10 days of the invoice issue date. That is not real-time in the literal sense, but it is close enough to rewrite the risk math for VAT fraud. There is no longer a quarter-long gap for a carousel to spin in.

For finance departments, the old rhythm breaks. Batch-processing at month-end and filing a summary no longer works. Data has to flow continuously. Systems must generate structured, machine-readable invoice data at the moment of issuance and push it to the Central VIES (VAT Information Exchange System) inside the 10-day window.

What Changes in the Central VIES

The Central VIES gets a significant upgrade. Instead of receiving aggregated periodic reports, it will ingest granular transaction-level data for every qualifying cross-border B2B supply: supplier VAT ID, buyer VAT ID, invoice number, invoice amount, VAT amount, and transaction date. Tax authorities move from a rear-view summary to a transaction ledger they can cross-match in near real time.

That architectural shift has a direct consequence: recapitulative statements (EC Sales Lists) will be abolished. Businesses no longer file them separately, because the DRR data itself becomes the authoritative record. That is one less reporting obligation, but only if the underlying data infrastructure can produce continuous, structured output.

For ERP vendors, this is the core engineering problem. Legacy platforms built around periodic batch exports need real rearchitecting to emit structured invoice data on issuance and transmit it on a per-transaction basis.

Mandatory E-Invoicing: The New Standard for Cross-Border B2B

Not every invoice survives ViDA. The format most businesses send today, a PDF attached to an email, will no longer count as an "electronic invoice" for cross-border B2B.

From 1 July 2030, cross-border B2B invoices must be structured and compliant with the European Standard EN 16931 — a machine-readable data object rather than a human-readable page. The detail of that semantic data model is its own subject, covered in the dedicated EN 16931 standard guide, and the hybrid PDF-plus-XML option is broken down in the ZUGFeRD and Factur-X format guide. The ViDA-relevant rule is simply this: a plain PDF will not qualify, because it cannot be ingested and validated by tax-authority systems without human handling — the full reasoning lives in why a PDF is no longer a valid invoice.

Consent Is No Longer a Barrier

Under current EU VAT rules, a supplier must obtain the buyer's prior acceptance before issuing an electronic invoice. ViDA scraps that requirement. From July 2030, suppliers can issue structured e-invoices unilaterally for cross-border B2B transactions, with no consent needed from the recipient.

This flips the default. Cross-border invoicing becomes digital, structured, and machine-readable by design. Buyers need systems ready to receive and process structured invoices, and any supplier still emitting unstructured documents will be non-compliant the day the mandate lands.

Cross-Border vs. Domestic: A Two-Speed Timeline

ViDA's 2030 mandate applies specifically to intra-EU cross-border B2B transactions. Domestic invoicing rules stay under national jurisdiction until 2035, when EU member states must align their domestic frameworks with the ViDA architecture.

That creates a two-speed reality. Businesses with heavy cross-border activity hit the earlier, harder deadline. Those operating mostly in domestic markets get more time, though not unlimited time. ERP vendors serving both segments need a single solution that spans both timelines rather than two parallel systems.

For software vendors that want to offer clients audit-ready e-invoice archiving aligned with both the ViDA standard and national requirements, the architecture has to be designed for both horizons from day one.

The Platform Economy and Single VAT Registration

Two of ViDA's three pillars tackle structural problems that grew up alongside the digital economy: VAT leakage through online platforms and the administrative drag of multi-country VAT registration.

The Deemed Supplier Model

Short-term accommodation platforms (think Airbnb-style rentals) and passenger transport platforms (ride-hailing services) will be treated as deemed suppliers for VAT purposes. The platform, not the individual host or driver, becomes responsible for collecting and remitting VAT on transactions where the underlying supplier is not VAT-registered.

The logic is straightforward, and the European Commission spells it out in its ViDA package: VAT compliance has been notoriously hard to enforce across thousands of micro-suppliers. By making the platform the liable party, tax authorities gain a single, auditable point of collection instead of a long tail of individual operators.

For platforms, this is a substantial operational change. They must track the VAT status of every service provider, calculate VAT correctly on every transaction, and remit it to the correct member state.

Expanding the One-Stop Shop (OSS)

Today the OSS scheme lets businesses selling digital services or goods to consumers across the EU register for VAT in a single member state and report all EU sales through that one registration. ViDA widens OSS coverage to include:

- Intra-EU transfers of own goods (simplifying the VAT treatment of cross-border inventory movements for e-commerce sellers)

- Domestic B2C supplies in certain circumstances

- Certain B2B supplies where the reverse charge mechanism does not apply

For SMEs operating across multiple EU markets, the payoff is concrete: fewer VAT registrations, fewer local compliance obligations, and one reporting channel covering a broader range of transactions.

Retention: One Obligation That Outlives the Invoice

A ViDA invoice does not end its life once it is reported. Most EU member states require business records to be kept for 7 to 10 years in their original form, which raises two separate questions ViDA itself does not answer: how to archive those structured invoices so they survive an audit, and how to prove they have not been altered. Those are different disciplines with their own owners — the country-by-country detail sits in the guide to e-invoice retention periods by country, the immutability and original-format rules in GoBD-compliant archiving requirements, and the tamper-evidence question — why ordinary cloud storage cannot prove integrity, and how a cryptographic hash anchored to a public blockchain can — in the blockchain timestamping guide. The short version for ViDA planning: budget for an archive that holds the structured invoice unchanged for a decade, not just for the moment it clears reporting.

For ERP vendors, that archiving layer is also a product opportunity rather than a build-from-scratch burden. The cryptographic infrastructure, retention management, and audit-trail generation can be embedded as a service, letting vendors offer blockchain-sealed, audit-proof invoice archiving under their own brand without standing up the compliance stack themselves.

Timeline and Implementation: Preparing for 2030 and 2035

ViDA's timeline is fixed, but implementation is already underway in several member states, and the gap between early movers and late adopters is widening.

2025 to 2027: Early Mandates and Voluntary Adoption

Several EU member states have already implemented or are implementing mandatory domestic e-invoicing ahead of the 2030 EU deadline. Poland's KSeF system and France's phased e-invoicing mandate are the most advanced examples. These national mandates are technically independent of ViDA but architecturally aligned with it. Businesses that comply with them are building the technical muscle ViDA will demand at scale.

For businesses not yet caught by a national mandate, this stretch is the window for voluntary adoption and infrastructure investment. Organizations that use it to upgrade their ERP data models, implement structured invoice generation, and establish compliant archiving workflows will face a far smoother 2030 transition than those who wait.

1 July 2030: The Cross-Border B2B Deadline

This is the non-negotiable date. From this point:

- All intra-EU cross-border B2B invoices must be structured and EN 16931-compliant

- Transaction-level data must reach Central VIES within 10 days of invoice issuance

- EC Sales Lists are abolished

- Supplier consent is no longer required for e-invoice issuance

2035: Full Domestic Harmonization

By 2035, domestic VAT reporting systems across all member states must be harmonized with the ViDA framework. This is the deadline that reaches businesses operating primarily in domestic markets, and the point by which ERP vendors must ensure their platforms can handle the full scope of ViDA for every customer segment.

Immediate Steps for CTOs and CPOs

- Audit your current invoice data model. Can your system generate EN 16931-compliant structured invoice data today? If not, where exactly is the gap?

- Map your cross-border transaction volume. Identify which customer segments and transaction types fall under the 2030 mandate first.

- Evaluate your archiving infrastructure. Can your document store demonstrate invoice integrity to a tax auditor for the full 7-to-10-year window, not just hold the files?

- Assess your ERP partner ecosystem. If you are an ERP vendor, your customers will ask you for a compliant e-invoicing and archiving solution. Do you have one ready to offer?

A ViDA-Forward Conclusion

ViDA is not a tax update with a deadline attached. It is a structural shift in how the EU expects businesses to generate, transmit, and preserve financial data. Treat it as an infrastructure decision rather than a compliance chore, and you come out of the transition with leaner, more automated finance operations and a far lower audit-risk profile. The transaction-level reporting that ViDA forces also produces cleaner data: disputes resolve faster, audits get shorter, and the quality of your financial records improves across the board.

The decisions made in the next 18 months determine which side of the 2030 line you land on. Cross-border suppliers, platforms, and the ERP vendors who serve them all need structured invoicing, near-real-time reporting, and a decade-long compliant archive in place before the mandate, not after.

If you are mapping ViDA-ready invoicing and archiving infrastructure for your ERP platform, see how OriginVault's e-invoicing archiving layer delivers blockchain-sealed, audit-proof retention you can deploy under your own brand.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.