E-Invoicing Germany 2027: XRechnung, ZUGFeRD & GoBD Guide

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

Germany just rewrote the rules for B2B invoicing. By 2028, every invoice exchanged between German businesses must arrive in a structured, machine-readable electronic format. No exceptions, no grace periods. If you run a finance team, build ERP software, or sell a B2B SaaS product, the clock on getting compliant infrastructure in place is already running, and the deadlines arrive in waves rather than all at once.

The German E-Invoicing Mandate: A Roadmap to 2028

Germany's shift to mandatory electronic invoicing didn't arrive quietly. The Wachstumschancengesetz, the Growth Opportunities Act, established a binding, phased rollout that affects every VAT-registered business operating in Germany. The law passed in March 2024 and set a clear sequence of obligations, staggered by company size so that smaller firms get more runway than large ones.

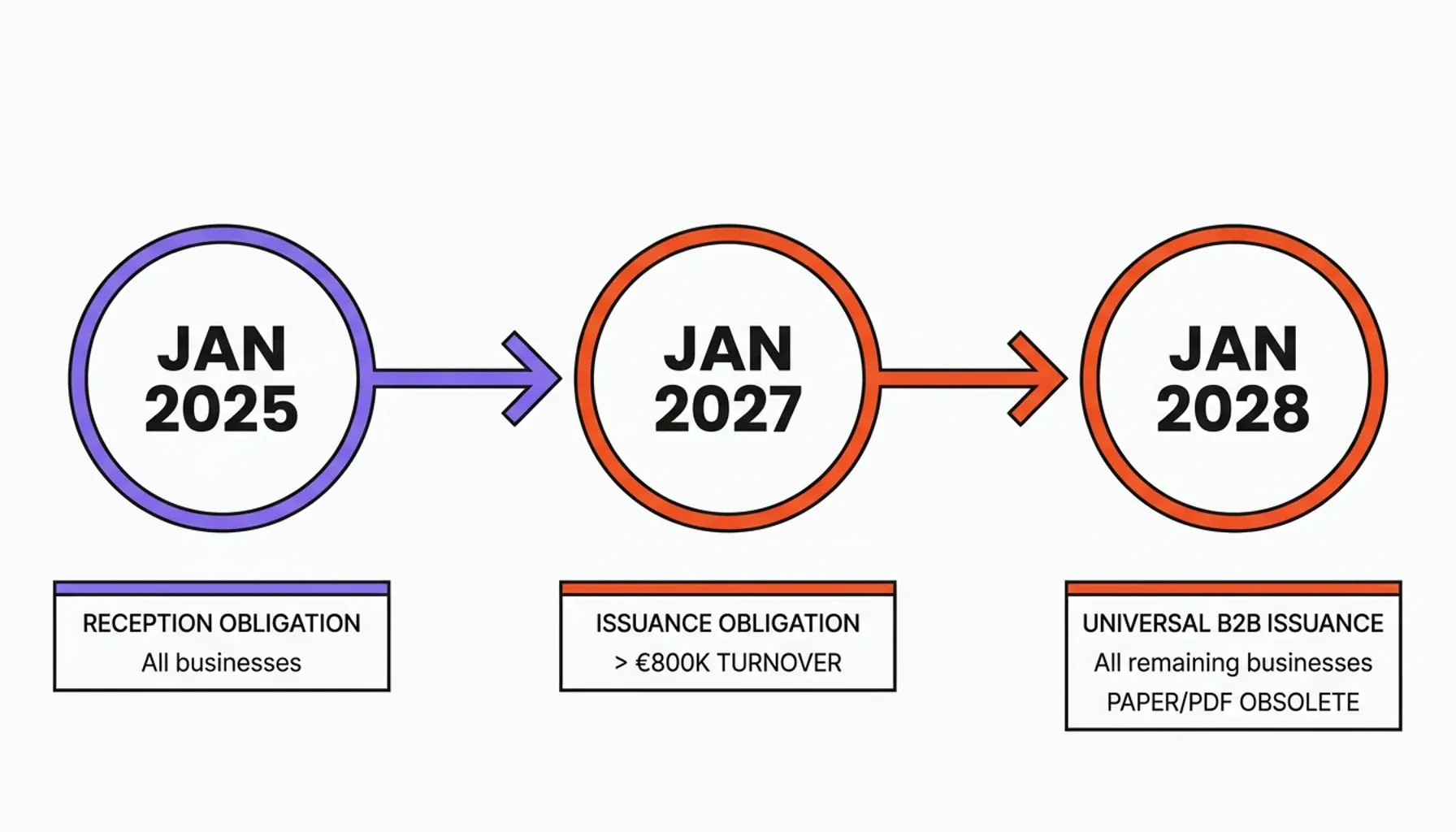

January 2025 marked the first hard deadline. From this date, every German business must be technically capable of receiving structured electronic invoices. Refusing or being unable to accept an e-invoice from a supplier is no longer a valid position. This reception obligation applies regardless of company size or annual revenue, so even a two-person firm has to be ready to take in a structured invoice the moment a supplier sends one. In practice, that means an inbox and a parser, not a printer.

January 2027 raises the stakes. Businesses with annual turnover exceeding €800,000 must also begin issuing structured electronic invoices for all domestic B2B transactions. This threshold captures the majority of mid-market and enterprise companies in Germany, and it is the deadline that turns e-invoicing from a "be able to receive" exercise into a full send-and-receive obligation for most of the economy.

January 2028 completes the transition. All remaining German businesses, regardless of turnover, must issue structured e-invoices for B2B transactions. At this point, paper invoices, unstructured PDFs, and scanned documents are fully obsolete under German tax law. A handful of narrow carve-outs survive, such as small-value invoices under €250 and certain tax-exempt supplies, but the default flips: structured is the rule, paper is the exception.

Germany's Federal Ministry of Finance has published detailed guidance on the scope of the mandate. It covers all B2B transactions subject to German VAT where both parties are established in Germany. Cross-border invoices and B2C transactions remain outside the immediate mandate, though the trajectory points toward broader adoption across the EU.

The business case for early action is straightforward. Companies that treat 2025 as a planning year and 2026 as an implementation year will be well-positioned. Those that wait until the 2027 deadline face rushed integrations, compliance gaps, and the very real risk of rejected invoices choking off their cash flow. An invoice that doesn't meet the format requirement is not a valid invoice for VAT purposes, which means the buyer may refuse to pay until it is reissued correctly, and the input-tax deduction can be jeopardised. The pain lands on accounts receivable long before it shows up in a tax audit.

For ERP vendors and SaaS providers, the mandate isn't just a compliance checkbox. It's a product requirement. Once a critical mass of German customers is legally obliged to send and receive structured invoices, any accounting, ERP, or billing tool that can't handle the formats and the downstream archiving becomes a liability customers will churn away from. End customers expect structured invoice formats, compliant archiving, and audit-ready documentation as standard features, not paid add-ons.

XRechnung vs. ZUGFeRD: Germany's Two Qualifying Formats

Not every digital file qualifies as an electronic invoice under the new mandate. The law specifically requires a structured format conforming to the European standard EN 16931, the EU's semantic data model for electronic invoices. A PDF created in Word, a scanned paper invoice, or an image file sent by email: none of these count as an e-invoice. Under the Wachstumschancengesetz, an electronic invoice is defined by its structure, not its delivery method. Emailing a PDF is still emailing a document; it is not sending structured data.

Germany recognizes two formats, and both satisfy EN 16931.

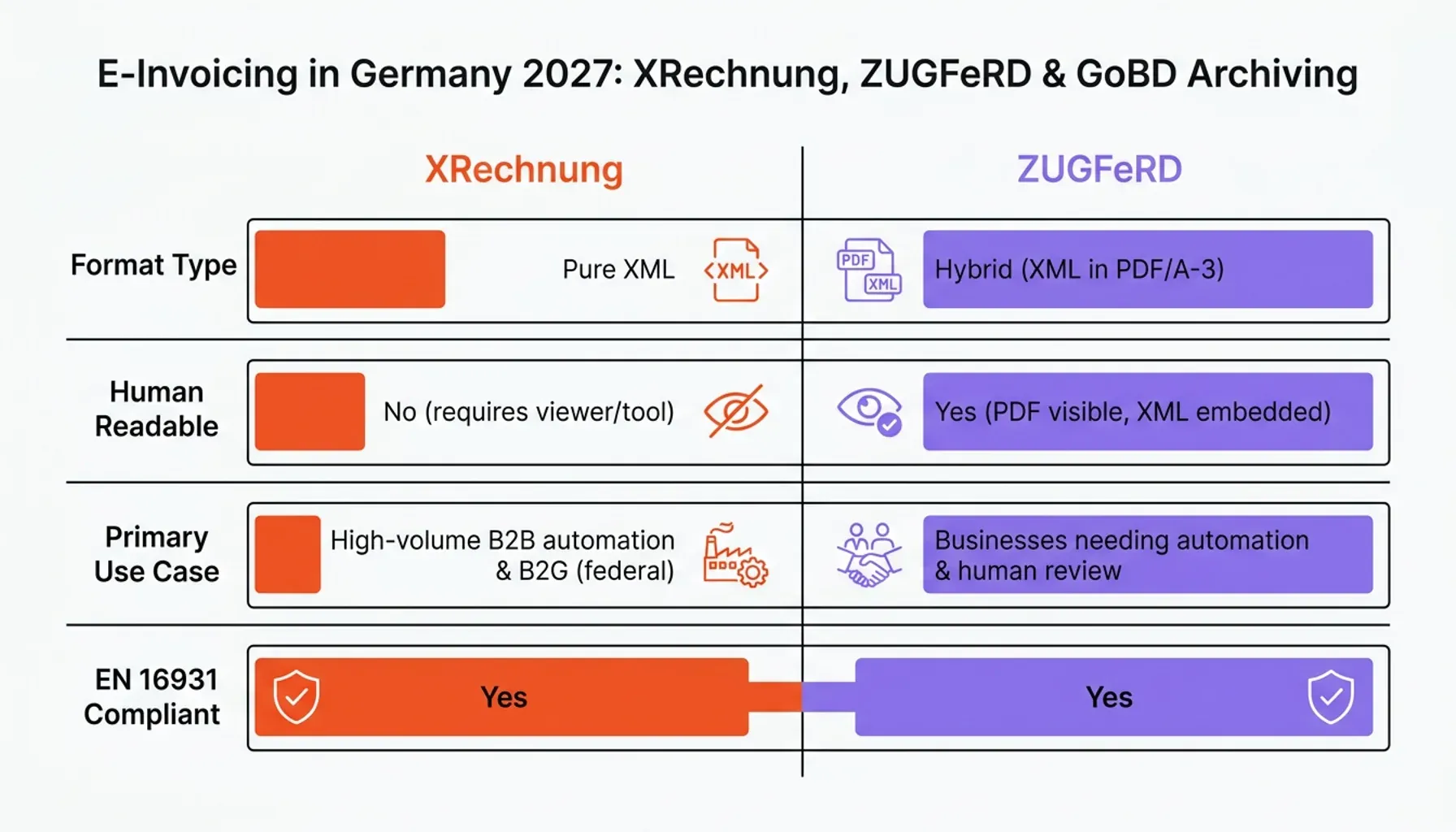

XRechnung is a pure XML standard developed by KoSIT, the Coordination Office for IT Standards, as Germany's national implementation of EN 16931. The invoice exists entirely as structured data, with no human-readable layer. ERP systems can ingest, validate, and post an XRechnung file without anyone touching it, which makes it the natural fit for high-volume automation. It is already mandatory for invoices sent to German federal public authorities (B2G), so many suppliers to the public sector have run it in production for years and already know its quirks. Open it in a plain text editor and you see tags, not a layout, which is exactly the point.

ZUGFeRD (version 2.2 and above) takes a hybrid approach: structured XML embedded inside a PDF/A-3 file, so the invoice is both human-readable and machine-processable at the same time. A supplier's finance team can eyeball the PDF while the buyer's ERP quietly parses the embedded XML, no second file required. That dual nature makes ZUGFeRD friendlier for organisations that still have humans in the approval loop, while keeping a fully compliant data layer underneath. ZUGFeRD is the German sibling of Factur-X, and the exact mechanics of the embedded-XML profiles, from BASIC through EN 16931 to EXTENDED, are covered in this guide to the hybrid Factur-X format.

Which one you reach for depends on transaction volume, your counterparties, and whether your ERP can swallow raw XML or needs a visual fallback. The mandate accepts both, so this is an architecture decision rather than a legal one. That decision deserves its own walkthrough, so I'll point you to the full XRechnung vs. ZUGFeRD comparison rather than half-cover it here.

GoBD Compliance in the German Context

Receiving and issuing structured invoices is only half the job. German tax law requires that every invoice, incoming and outgoing, be retained for ten years in a form that satisfies the GoBD, the principles for proper bookkeeping. The mandate creates a flood of new structured files, and the GoBD decides how you are allowed to keep them. For a German B2B issuer, that boils down to four obligations: keep each invoice in its original format (an XRechnung stays XML, never a printout), keep it machine-readable and searchable across the full ten years, prevent any undetectable alteration through technical controls rather than office policy, and maintain a Verfahrensdokumentation that describes the archiving process end to end. In an audit, a missing Verfahrensdokumentation is treated as a failure on its own, no matter how sound the system behind it is.

These rules reshape ERP workflows in ways teams often underestimate. A system that auto-converts incoming invoices to PDF for storage has to be reconfigured to keep the source XML. A folder of files with no index fails the machine-readable test the moment an auditor asks you to pull every invoice from a given supplier in a given quarter. And because the mandate now routes structured data through the same pipes that feed your archive, the easiest time to get retention right is when you build the ingestion path, not three years later under audit pressure. For the full requirement-by-requirement breakdown, see what GoBD-compliant archiving demands for e-invoices.

Beyond Storage: Why Plain Cloud Isn't Enough

Here is the catch most teams miss: standard cloud storage doesn't satisfy GoBD's non-alteration rule on its own. Files in S3, Azure Blob, or a shared drive can be overwritten or deleted by anyone with admin rights, usually without a trace. Storage keeps a file available; it does not prove the file is the same one you received. GoBD's prohibition on alteration needs a separate technical integrity layer, and blockchain-anchored SHA-256 sealing provides one: a mathematical fingerprint that breaks the moment a single byte changes, paired with independent proof of when the invoice was archived. The full mechanism, and why this beats trusting a provider's access controls or an ISO 27001 certificate alone, is unpacked in tamper-proof versus merely secure storage.

The ERP Challenge: Embedding Compliant Archiving

Building certified, GoBD-grade archiving infrastructure in-house rarely pencils out for an ERP vendor. Original-format retention, ten-year machine-readability, tamper-proof sealing, Verfahrensdokumentation, multi-tenant isolation: each one is its own engineering project, and all of them need maintaining as the rules shift. So most vendors don't build it. They embed a certified white-label archiving layer through an API and ship compliant archiving under their own brand, with invoice ingestion, sealing, and audit export running quietly in the background. White-label invoice archiving with blockchain-level integrity lets you offer the capability without owning the subsystem, and treating compliance as a revenue line rather than a cost centre is what turns it into a retention and pricing lever.

Action Plan: Preparing Your Infrastructure for 2027

The 2027 deadline is close enough to require action now. Here's a structured approach to closing compliance gaps before the mandate takes effect.

Step 1: Audit your current invoice lifecycle. Map every touchpoint from invoice generation or receipt through transmission, processing, and long-term storage. Identify the format at each stage. Is the original structured XML preserved, or converted at some point? Where does the invoice file physically reside, and who has write access? Most teams discover at least one silent format conversion they didn't know was happening.

Step 2: Run a gap analysis against GoBD requirements. Test your current system against four criteria: original-format retention, machine-readability over ten years, technical non-alteration controls, and a Verfahrensdokumentation. Be honest about the last one. Plenty of companies have decent storage and no written process documentation at all, which is its own audit finding.

Step 3: Validate your format capabilities. Confirm that your systems can both generate and receive XRechnung and ZUGFeRD 2.2+ files. If your ERP currently exports PDF invoices, this is a format upgrade, not just a configuration change. Test against real counterparty systems early, because validation errors tend to surface only when a live invoice bounces.

Step 4: Select technology partners with the right certifications. GoBD compliance is not self-certified. Look for partners with recognized certification, ISO 27001 information security accreditation, and a documented track record in multi-tenant ERP environments. Ask to see how they prove non-alteration, not just how they store files. A vendor who can hand an auditor an independent integrity check is worth more than one who simply promises durability.

Step 5: Automate the compliance engine. Manual archiving workflows introduce human error and audit risk. The target state is a fully automated pipeline: invoice received, format validated, hash generated, blockchain anchor created, document indexed in a compliant archive, audit trail logged. Every step automatic, logged, and retrievable on demand, so that "show me this invoice" takes seconds rather than a frantic afternoon.

The 2027 e-invoicing mandate is a structural change to how German B2B commerce operates. XRechnung and ZUGFeRD are the formats. GoBD is the archiving law. Blockchain-sealed integrity is what makes compliance independently verifiable. The infrastructure to support all three needs to be in place before the deadlines arrive, not after.

If you're an ERP vendor or SaaS provider looking to offer your customers audit-proof, GoBD-compliant invoice archiving under your own brand, explore OriginVault's white-label e-invoicing archiving solution to see how a single API integration covers the full compliance stack.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.