What Is GoBD-Compliant Archiving? E-Invoice Requirements

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

What Is GoBD-Compliant Archiving? E-Invoice Requirements

A tax audit rarely starts with a question. It starts with a request: "Please provide all relevant invoices for the period 2019 to 2024 in machine-readable format." If your archiving system cannot answer that completely, correctly, and immediately, the consequences range from estimated tax assessments to full disallowance of input tax deductions. GoBD-compliant archiving is not a bureaucratic checkbox. It is the technical and legal foundation that decides whether your digital bookkeeping holds up under scrutiny.

Think of GoBD's immutability requirement the way forensic investigators think about chain-of-custody logs. Every piece of evidence must be sealed, timestamped, and traceable from the moment it enters the record, because the instant you cannot prove it was untouched, it loses its evidentiary value entirely. GoBD applies exactly that logic to your invoices. If you cannot prove a document is exactly as it was when it was archived, it is legally worthless to a German tax auditor.

With Germany's mandatory e-invoicing rollout now in effect for B2B transactions, this gap matters more than ever, both for businesses and for the software vendors who serve them.

The GoBD Framework: Why Compliance Is Non-Negotiable

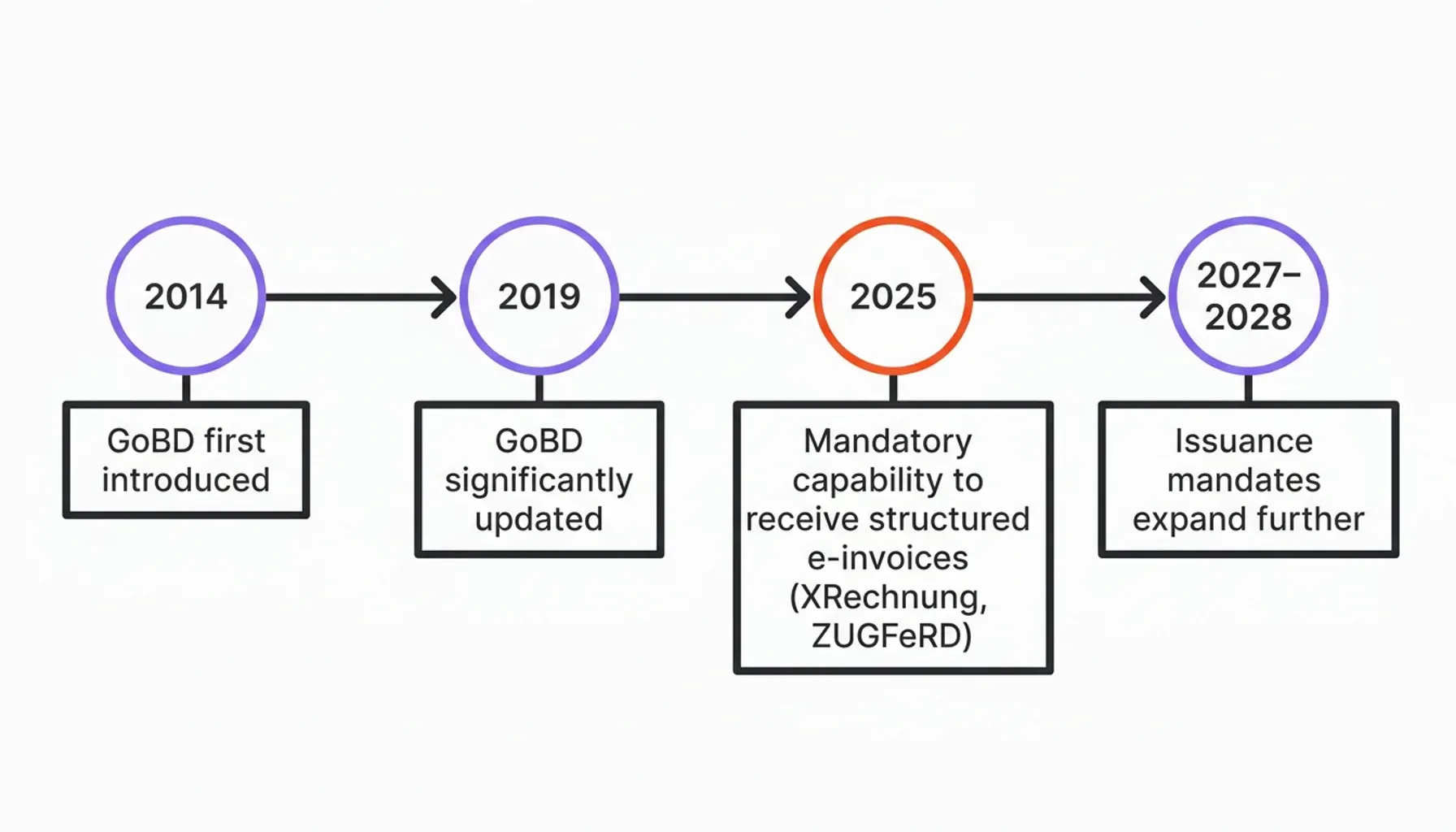

GoBD, Grundsätze zur ordnungsmäßigen Führung und Aufbewahrung von Büchern, Aufzeichnungen und Unterlagen in elektronischer Form sowie zum Datenzugriff, is the German Federal Ministry of Finance's authoritative framework governing how businesses must manage and retain tax-relevant digital records. First introduced in 2014 and significantly updated in 2019, GoBD defines the minimum technical and procedural standards that any electronic bookkeeping system must meet.

The framework's core objective is precise: digital tax records must provide the same evidentiary reliability as paper-based accounting. Every invoice, every journal entry, every supporting document must be retrievable, readable, and provably unaltered at any point during the legally mandated retention period.

The shift to mandatory e-invoicing has made GoBD compliance structurally more complex. As of 2025, German B2B businesses must be capable of receiving structured electronic invoices (XRechnung, ZUGFeRD). By 2027 and 2028, issuance mandates expand further. The volume of machine-readable, structured invoice data flowing through accounting systems will increase sharply, and every byte of it falls under GoBD's retention requirements.

The legal consequences of non-compliance are not theoretical. Tax authorities conduct digital audits with GDPdU/GoBD-compliant data access. If records are incomplete, unreadable, or show signs of manipulation, auditors are legally entitled to estimate taxable income, a process that almost always produces higher tax assessments. In severe cases, the evidentiary value of the entire bookkeeping system can be invalidated, exposing the business to back-taxes, interest, and penalties across multiple fiscal years.

For ERP vendors and SaaS providers, this creates a direct product obligation: the software you sell must not just process invoices. It must archive them in a way that survives a tax audit.

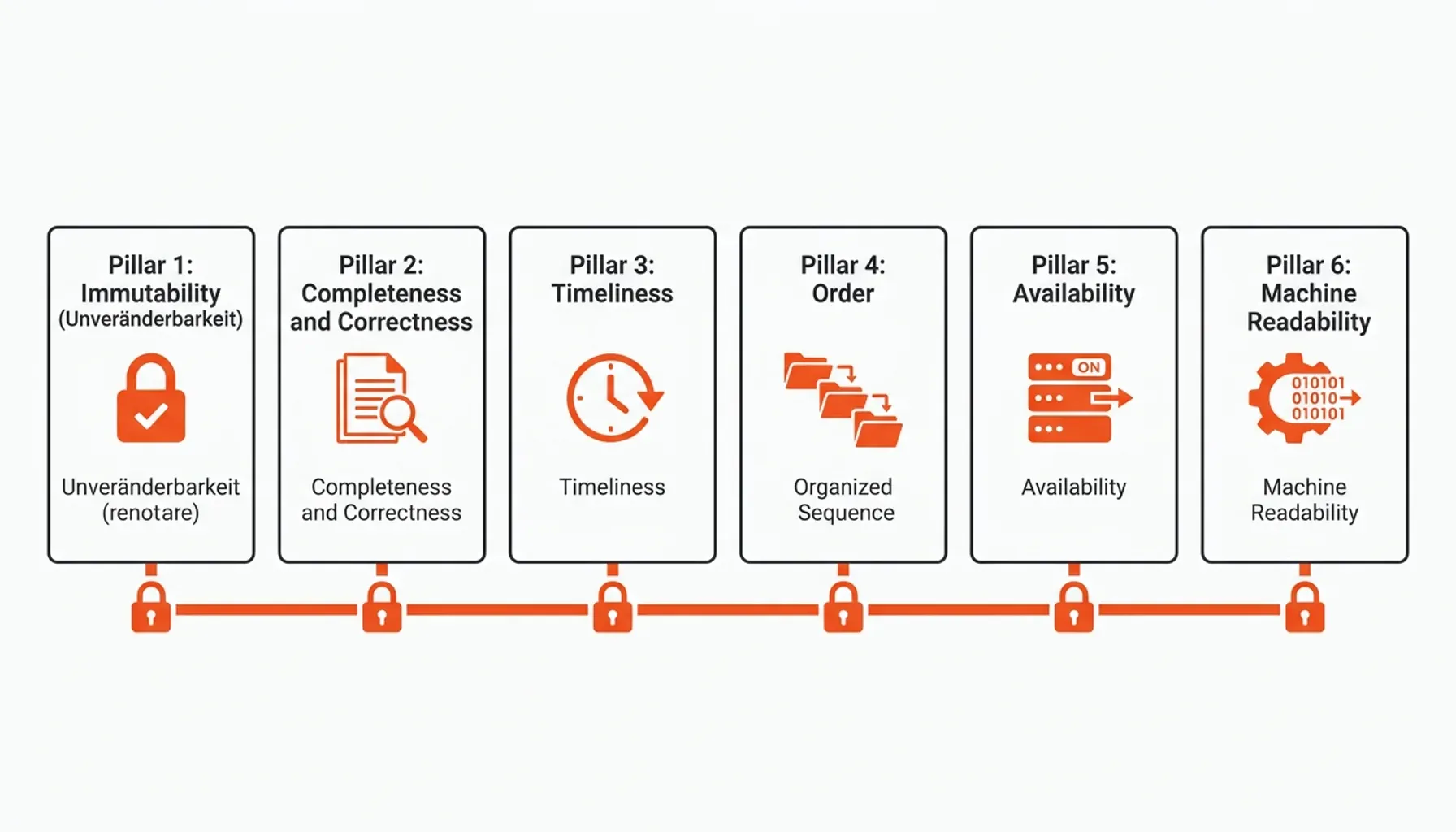

Core Requirements: The 6 Pillars of GoBD Compliance

GoBD compliance is not a single feature. It is a system of interlocking requirements, each of which must be satisfied simultaneously. Miss one, and the entire archiving process becomes legally vulnerable.

1. Immutability (Unveränderbarkeit)

This is the non-negotiable core. Once a tax-relevant document enters the archive, nobody can modify it, not end users, not system administrators, not the software vendor. GoBD does not accept "read-only" file permissions as sufficient protection. The requirement is technical immutability: any change to an archived document must be detectable, logged, and traceable. The accepted mechanism is a cryptographic seal combined with an independent timestamp anchor that no administrator can rewrite, a model explored in depth alongside the audit risks in conventional archiving systems.

2. Completeness and Correctness

Every tax-relevant document must be captured in its entirety. Partial archiving, whether storing only the invoice header but not line items, or retaining a summary PDF while discarding the underlying XML, violates GoBD. For structured e-invoices, the full XRechnung or ZUGFeRD file must be retained, not a human-readable derivative.

3. Timely Posting and Capture

GoBD specifies that cash transactions must be recorded daily, and other business transactions within ten days of occurrence. For e-invoicing workflows, the archiving trigger must be automated. Manual, batch-based archiving processes introduce timing gaps, and auditors notice.

4. Order and Traceability

Archived documents must be systematically indexed and retrievable. Every invoice needs a unique identifier, and the system must support structured search by date, amount, counterparty, and document type. The audit trail must let an auditor reconstruct every transaction from the original document to the final posting without gaps. For most ERP implementations, this is exactly where archiving either quietly succeeds or quietly fails.

5. Availability and Machine Readability

This pillar has become significantly more demanding with e-invoicing mandates. A scanned PDF is not machine-readable in the GoBD sense. XRechnung compliance requires retention of the structured XML data, and a ZUGFeRD archive must preserve both the visual layer and the embedded XML rather than a flattened copy. Exporting data in GDPdU-compatible format for auditor access is a mandatory capability, not a nice-to-have.

6. Protection Against Loss

Redundant storage, backup procedures, and disaster recovery must be documented. GoBD explicitly requires that archived data cannot be lost through hardware failure, software migration, or organizational changes. In practice this means a documented backup-and-recovery routine with verified restore tests, written into the Verfahrensdokumentation so an auditor can confirm not just that backups exist, but that data can actually be recovered intact within the ten-year window.

For software vendors building GoBD-compatible products, satisfying all six pillars at once, especially immutability and machine readability, is where most implementations fall short. A purpose-built white-label invoice archiving layer addresses these requirements at the infrastructure level, so ERP vendors do not have to engineer them from scratch.

How GoBD Treats Integrity and the Audit Trail

GoBD does not prescribe a single technology, but it does set a clear bar: immutability must be technically detectable and traceable, not merely promised by file permissions. The accepted mechanism is a cryptographic hash of each document paired with an independent timestamp anchor that no administrator, not even the archiving vendor, can rewrite after the fact. The detailed mechanics, including the SHA-256 fingerprinting, the administrator-can-recompute-the-hash problem, and how a public ledger closes that gap, belong to the deep dive on tamper-proof versus secure storage. NIST maintains the reference specification for the SHA-256 hash function that underpins these seals.

GoBD also requires a tamper-evident access log: every view, export, and failed retrieval attempt recorded with a timestamp, a user, and the action taken, in a way that cannot be selectively edited to remove inconvenient entries. The full three-pillar treatment of how that log is structured and verified sits in the guide to e-invoice archiving integrity and audit-trail requirements. For an auditor, the decisive question is never "does this system store documents?" but "can it prove every document is exactly as it was when archived?" That distinction separates compliant archiving from compliant-looking archiving.

Retention Periods and Format Integrity for E-Invoices

GoBD retention requirements draw from two primary legal sources: Section 257 of the German Commercial Code (HGB) and Section 147 of the Tax Code (AO). The standard retention period for tax-relevant documents, including all invoices, is ten years. The clock starts not on the date of the document, but at the end of the calendar year in which it was created. An invoice dated March 15, 2024, must be retained until at least December 31, 2034.

The Original Format Requirement

Most archiving implementations fail silently on this point. GoBD requires that documents be retained in their original format, the format in which they were received or created. For a hybrid ZUGFeRD invoice, that means keeping the file with its embedded XML intact, not a standalone PDF rendering. Convert it away and the visual content may look identical, but the structured, machine-readable XML that makes it a valid e-invoice is gone, and the archive no longer satisfies GoBD.

For XRechnung, the rule is stricter still: only the XML file itself constitutes the invoice, while a PDF rendering is a convenience document, not the legal record. The format-level anatomy of each option is covered in the XRechnung versus ZUGFeRD comparison; here the point is simply the GoBD consequence: strip out the XML and you break the archive. Many businesses do not realize this until an auditor points it out.

System Migrations and Format Conversion

When businesses upgrade ERP systems or migrate to new archiving platforms, the legal validity of historical archives must be preserved. GoBD permits format conversion during migration under strict conditions: the conversion process must be fully documented, the original format must be retained alongside the converted version during a transition period, and the integrity of every migrated document must be verifiable post-migration. One undocumented migration can invalidate years of otherwise compliant records.

Hardware WORM vs. Software-Defined Integrity

Legacy archiving relied on hardware WORM (Write Once, Read Many) optical disks to enforce immutability. Modern GoBD-compliant systems use software-defined integrity layers, cryptographic seals and timestamps, that achieve the same legal effect without proprietary hardware dependencies. This shift matters enormously for cloud-based and multi-tenant architectures, where physical media is not a practical option. It also explains why auditors increasingly expect software-defined immutability as the default rather than the exception.

The Vendor Perspective: Building GoBD-Compatible Software

For ERP and SaaS vendors serving the German market, GoBD compliance is no longer a differentiator. It is a market entry requirement. A product that cannot demonstrably meet GoBD standards cannot be sold to German businesses for bookkeeping purposes. The question is not whether to build compliant archiving, but how to build it without consuming your entire engineering roadmap.

Rather than build and maintain a proprietary archiving stack, many vendors now embed a certified third-party archiving layer through an API. That choice keeps GoBD's hardest pillars, immutability, per-tenant segregation, and machine-readable export, out of their own codebase. The mechanics of embedding a compliant retention API, the multi-tenancy and brand questions covered in the white-label archiving guide for software vendors, and the buy-versus-build economics laid out in the build-vs-buy decision for a compliant archive each deserve their own treatment. The GoBD-specific takeaway is narrower and worth keeping in view.

A vendor selling into both Germany (GoBD) and Switzerland (GeBüV) faces requirements that are similar in principle but differ in certification specifics, and maintaining two separate compliance stacks is expensive. A single archiving layer carrying both GoBD and GeBüV certifications removes that duplication. The IDW PS 880 audit standard for software products reinforces the embed approach: software that relies on a certified sub-component for a function such as archiving can reference that component's certification in its own compliance documentation, provided the integration is properly documented. OriginVault's audit-grade invoice archiving infrastructure is built for exactly this, a dual-certified layer ERP vendors embed through one API.

Procedural Documentation: The Most Overlooked Requirement

Ask most software vendors whether their product is GoBD-compliant, and they will point to technical features: hash values, access controls, retention policies. Ask them for their Verfahrensdokumentation, and the conversation often goes quiet.

The Verfahrensdokumentation, procedural documentation, is a mandatory GoBD requirement that describes, in plain language and technical detail, the complete process from invoice receipt to final archiving. It must cover the content of the process (what documents are captured and why), the technical structure of the system (how data flows, where it is stored, what security measures apply), and the internal control systems (ICS) that prevent errors and unauthorized access.

This documentation is not a one-time deliverable. It must be versioned and updated every time the underlying process or system changes. A software update that changes the archiving trigger, a migration to a new storage backend, a change in user access roles: each of these events requires a documented update to the Verfahrensdokumentation, with the previous version retained for the duration of the retention period. Miss an update, and you have a gap. Auditors find gaps.

For auditors, a complete and current Verfahrensdokumentation is the first document they request. An immutable, timestamped audit log, where every system access, every configuration change, and every document retrieval is recorded and tamper-evident, dramatically simplifies the verification process. Instead of reconstructing system behavior from fragmented logs, the auditor reviews a complete, chronological record that proves the system operated as documented.

Businesses that invest in procedural documentation upfront, and maintain it rigorously, consistently experience shorter, less disruptive tax audits. Those that treat it as an afterthought discover its importance at the worst possible moment.

Where Archiving Requirements Are Heading

The rules governing digital invoicing and tax data are not static. The European Commission's VAT in the Digital Age reform points toward real-time digital reporting across EU member states, which will make continuous, automated, tamper-proof archiving a baseline expectation rather than an optional investment; the full scope of that change is covered in the guide to the ViDA reform.

Germany's e-invoicing mandate is an early piece of that broader trend. As real-time reporting converges with structured invoice formats, the technical requirements for compliant archiving will only grow more specific. Systems that cannot produce machine-readable audit evidence on demand, in formats auditors can directly ingest, will steadily lose ground.

The architecture that survives this evolution is cloud-agnostic, API-driven, and built on software-defined immutability. It does not depend on proprietary hardware, a specific cloud provider, or manual compliance workflows. It seals every document at the moment of archiving, generates an independent proof of integrity, and maintains a complete, queryable audit trail automatically.

For businesses evaluating their current archiving infrastructure, the right question is not "are we compliant today?" It is "will our system still be compliant when real-time reporting requirements take effect, and can we prove it?"

GoBD-compliant archiving is a precise technical discipline with direct legal consequences. Every pillar, immutability, completeness, machine readability, and procedural documentation, must be satisfied simultaneously and sustainably. As e-invoicing mandates expand and real-time reporting approaches, the cost of getting this wrong will only rise.

If you are building or evaluating archiving infrastructure for the German and European market, explore how OriginVault's white-label invoice archiving solution delivers audit-grade, GoBD-ready retention as a back-end service, so your product meets the standard without building the stack yourself.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.