EU E-Invoicing Mandates 2026–2030: Country Timeline Guide

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

EU E-Invoicing Mandates 2026-2030: Country Timeline Guide

Picture this: it's January 2025, and the CTO of a mid-size ERP vendor in Munich is reviewing a routine compliance checklist. Then comes the gut-punch. Their invoice pipeline, serving dozens of German SME clients, can't receive structured XRechnung files. Not "not optimally." Not "partially." Fully non-compliant, as of that very month. The receiving obligation had gone live on January 1st, and nobody had flagged it.

That scenario isn't hypothetical. I've heard versions of it from vendors across the DACH region. And Munich was just the canary. Zoom out, and you'll see the same reckoning land in Warsaw, Brussels, Paris, and Madrid over the next 36 months.

The European Union is running the largest coordinated overhaul of business transaction reporting in its history. For decades, VAT compliance worked like a photo album: businesses snapped pictures of their transactions, filed them away, and showed the album to tax authorities during an audit years later. That model is ending. What replaces it is a live feed, transaction data flowing to tax authority systems the moment invoices are issued. By 2030, every B2B invoice crossing an EU border will move through that infrastructure.

This guide maps every major national mandate from 2025 through 2030, country by country, with the exact dates, turnover thresholds, and platforms you need to plan against. If you only read one section, read the master table below.

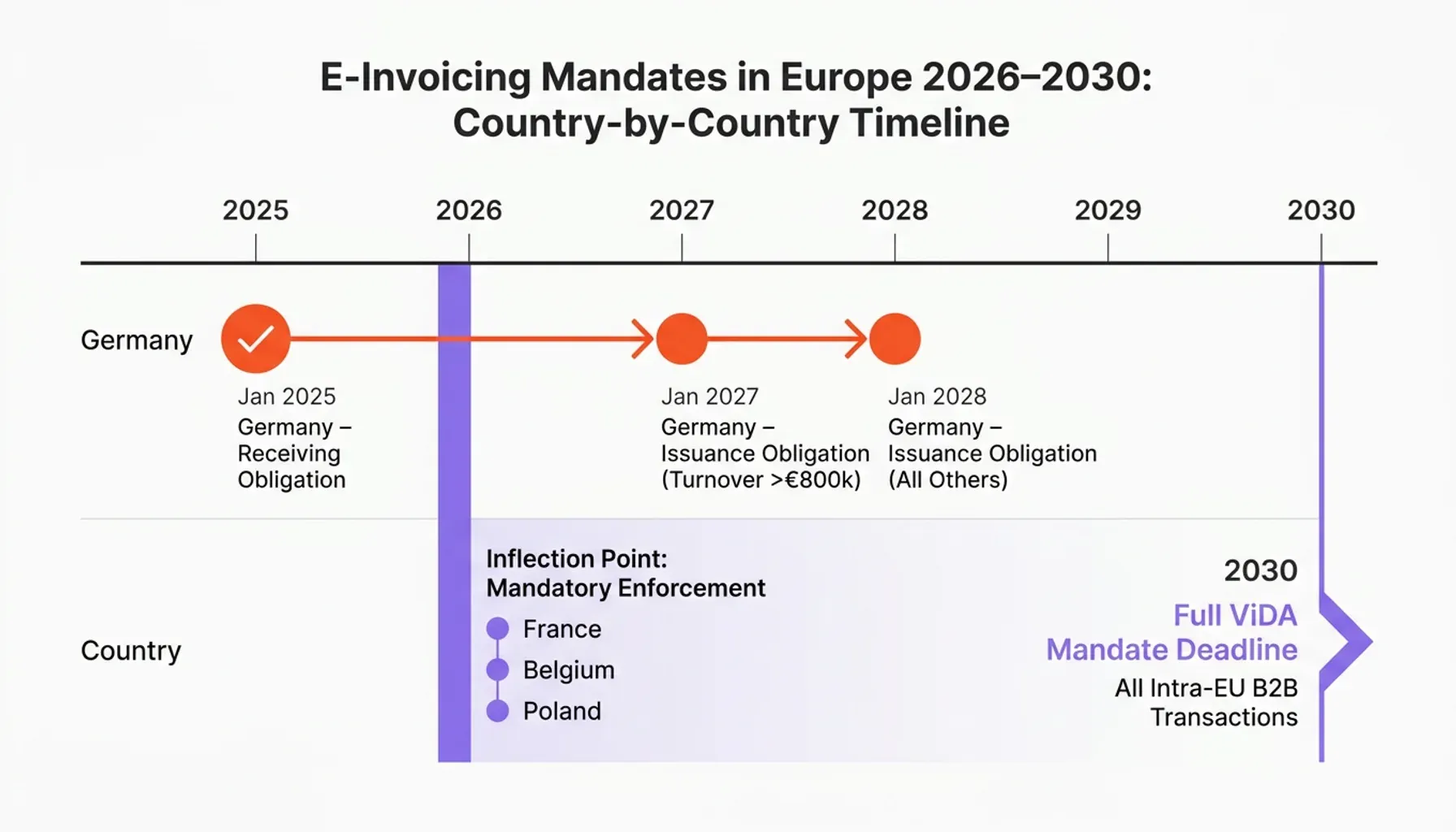

The Master Timeline: Every Country, Every Deadline

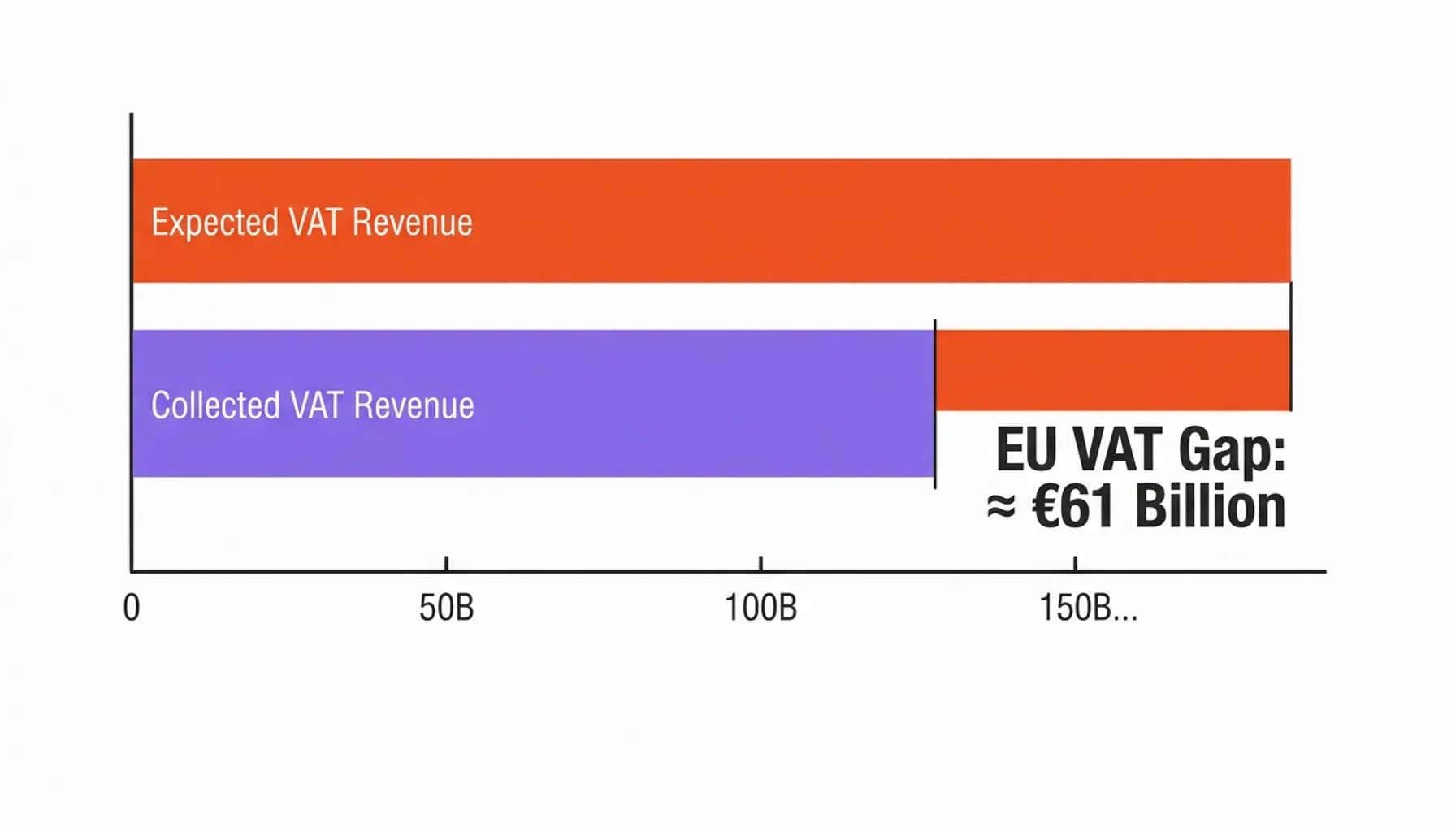

The dates below are the heart of this page. Each mandate sits on the same architectural shift: a move from post-audit models (authorities review historical records) to real-time or near-real-time clearance (invoices validated against tax systems as they're issued). That shift is codified in the EU's VAT in the Digital Age (ViDA) package. ViDA makes intra-EU B2B e-invoicing and digital reporting mandatory by 2030 and replaces today's patchwork of national derogations; the mechanics of the reform are covered in our guide to what ViDA actually changes. The economic driver is blunt: the EU's VAT gap reached roughly €61 billion in a recent year, and real-time reporting closes the reconciliation window where fraud and error accumulate.

2026 is the hinge. It's when the largest economies, Germany, France, Belgium, and Poland, move from pilots and reception-only rules into mandatory issuance and clearance. 2030 is the second hinge: the EU-wide cross-border DRR obligation.

| Country | Scope | Reception deadline | Issuance deadline | Threshold / phasing | Platform / model |

|---|---|---|---|---|---|

| Germany (DE) | B2B | Jan 2025 | Jan 2027 / Jan 2028 | Issuance from 2027 if turnover > €800k; all others 2028 | Decentralised, EN 16931 (XRechnung/Factur-X) |

| France (FR) | B2B | Sep 2026 | Sep 2026 → 2027 | Issuance phased by company size through 2027 | PPF + certified PDP platforms |

| Belgium (BE) | B2B | Jan 2026 | Jan 2026 | All VAT-registered taxable persons | Peppol four-corner |

| Poland (PL) | B2B | Feb / Apr 2026 | Feb / Apr 2026 | Large taxpayers Feb 2026; all others Apr 2026 | KSeF central clearance, FA(3) |

| Romania (RO) | B2B | Jan 2024 | Jan 2024 | Live; B2G since 2022 | RO e-Factura clearance (ANAF), UBL 2.1 |

| Italy (IT) | B2B | Live (2019) | Live (2019) | Universal; cross-referenced below | SdI clearance, FatturaPA |

| Spain (ES) | B2B | 2027 / 2028 | 2027 / 2028 | Large companies 2027; SMEs 2028 | FacturaE, eIDAS seal, payment-status reporting |

| Greece (GR) | B2B | ~2027 | ~2027 | Phased from B2G/bookkeeping | myDATA platform |

| Croatia (HR) | B2B | 2026 / 2027 | 2026 / 2027 | Phased via Fiscalization 2.0 | Real-time fiscalization → B2B |

| Netherlands (NL) | B2B | No domestic B2B mandate (2025) | — | Follows ViDA 2030 for cross-border | Peppol (B2G mandatory) |

| Denmark (DK) | B2B | Phased from 2024–2026 | Phased from 2024–2026 | Bookkeeping Act; digital records by company class | Peppol / NemHandel |

| Slovakia (SK) | B2B | Planned ~2027 | Planned ~2027 | Aligned to ViDA timeline | National clearance, EN 16931 |

Read the table once, then use the country notes below for the detail that matters most for your build, especially the "what breaks if you miss this" consequence for each major market.

2025-2026: The Early Movers

Germany: Phased Obligation, Immediate Urgency

Germany's approach is methodical. Since January 2025, every German business must be capable of receiving structured e-invoices in EN 16931-compliant formats, either XRechnung or Factur-X. The obligation to issue structured invoices follows in January 2027 for businesses with annual turnover above €800,000, and January 2028 for everyone else.

What breaks if you miss it: reception must work today. A vendor serving German SMEs that still bounces inbound XRechnung files is already non-compliant, and its clients can't post those invoices cleanly. Retention then carries its own rules. German invoices must be archived unaltered, auditable, and accessible for up to ten years under the GoBD framework, which we unpack in our GoBD-compliant archiving guide. The full German rollout, formats and all, lives in our Germany 2027 mandate breakdown. Keep the dates and the €800k threshold front of mind; that's the part this page owns.

Poland: KSeF After the Delays

Poland's KSeF mandatory e-invoicing rollout has a bumpy history. Originally set for 2024, technical-readiness concerns pushed the mandatory date to February 2026 for large taxpayers and April 2026 for all remaining B2B transactions.

KSeF is a pure clearance model. Invoices go to the national system, get validated, and receive a unique identifier before they're legally effective. No KSeF number means the invoice doesn't legally exist yet. For foreign vendors supplying Polish buyers that's a hard dependency: invoices without a KSeF number may not be deductible for the recipient. What breaks if you miss it: your ERP has to handle platform outages, validation rejections, and retry logic, or your clients' Polish customers can't reclaim their VAT.

Romania: Quiet Leader in Real-Time Reporting

Romania's RO e-Factura system has been mandatory for B2G since 2022 and expanded to B2B in January 2024. It uses UBL 2.1 XML submitted to ANAF (the national tax authority) for real-time clearance. Romania is arguably the most advanced clearance-model implementation in Central and Eastern Europe, and the clearest preview of ViDA's 2030 endgame at national scale.

Belgium: The January 2026 Mandate

Belgium's e-invoicing mandate activates on January 1, 2026, requiring all VAT-registered businesses to exchange structured invoices over Peppol. Belgium picked Peppol as its delivery backbone, so businesses need a Peppol-registered access point, not just the ability to generate XML.

The Belgian mandate stands out for scope: it covers all taxable persons, not only large enterprises. That makes it one of the broadest immediate mandates in the EU and a major driver of Peppol adoption across the Benelux region. What breaks if you miss it: from day one in 2026, a Belgian client of any size can't legally send you a compliant invoice unless both ends sit on Peppol.

2027-2028: France, Spain, and the Mediterranean

France: A Two-Track System Under Pressure

France's e-invoicing mandate has been among the most closely watched, and most revised, in Europe. The current timeline mandates reception capability for all businesses by September 2026, with issuance requirements phased by company size through 2027.

France's architecture is distinctive. Businesses route invoices through either the PPF (Portail Public de Facturation, the government portal) or a certified PDP (Plateforme de Dématérialisation Partenaire, a private partner platform). The PDP model creates a competitive private market for compliant transmission, and a real opening for ERP vendors to position themselves as certified intermediaries rather than format converters. If you're a German supplier with French customers, the cross-border picture for foreign suppliers needs attention now: a German company invoicing a French VAT-registered buyer must meet French format and transmission rules, regardless of where the seller sits.

Spain: Crea y Crece and the B2B Obligation

Spain's Crea y Crece law set the legal basis for mandatory B2B e-invoicing. Implementing regulations developed through 2024 and 2025 target a 2027 rollout for large companies and 2028 for SMEs. Spain uses the FacturaE format with electronic signatures under eIDAS.

One detail you shouldn't miss: Spain's mandate includes a payment confirmation requirement. Buyers must acknowledge receipt and payment status electronically. That goes beyond invoice transmission, so your system has to handle bidirectional status updates, not just outbound delivery.

Greece: myDATA Maturity

Greece's myDATA platform has been operational since 2021 and keeps evolving. Current requirements cover digital bookkeeping and income/expense classification, with the trajectory pointing toward full e-invoicing integration around 2027, in line with the ViDA timeline. Greece is building its feed incrementally, but it's building it.

Croatia: Fiscalization 2.0

Croatia's Fiscalization 2.0 project extends the country's existing real-time fiscalization infrastructure, originally built for B2C cash registers, into B2B e-invoicing. Milestones through 2026 and 2027 bring Croatia into full alignment with ViDA ahead of 2030. It's a useful case study in repurposing existing real-time infrastructure rather than building from scratch.

Beyond the EU: The UK and Switzerland

United Kingdom: Voluntary Progress, No Mandate

Post-Brexit, the UK isn't bound by ViDA. HMRC's current position favours voluntary adoption and industry-led standards over a mandated clearance model. The government has backed Peppol in public procurement but hasn't legislated B2B obligations.

For UK businesses trading with EU counterparties, that creates an asymmetric burden. EU customers may require structured formats for their own tax reporting even when UK law doesn't. The feed is running on the EU side of the channel, and UK suppliers are expected to plug into it regardless. Adopting EN 16931-compliant formats is increasingly a commercial necessity, not a regulatory one.

Switzerland: GeBüV and Federal Administration Mandates

Switzerland sits outside the EU but stays deeply integrated with the Eurozone. The Swiss Federal Tax Administration (ESTV) mandates e-invoicing for federal government suppliers, and the GeBüV framework governs how digital business documents must be retained. GeBüV requires that archived invoices stay tamper-evident and machine-readable across the full retention period.

The interoperability problem for non-EU entities is concrete. A Swiss supplier selling into the EU has to connect to Peppol. It has to meet each country's format rules. And it has to maintain compliant archives under both domestic and foreign retention laws at once. Few point solutions cover all three, which is why GeBüV-certified archiving infrastructure matters for Swiss firms with EU customers.

Retention and Integrity: The Obligation Behind Every Mandate

Receiving a structured e-invoice isn't the end of the job. Every framework on this page, GoBD in Germany, GeBüV in Switzerland, and the retention rules baked into national ViDA implementations, requires invoices be stored immutably and verifiably for seven to ten years, and that you can prove during an audit that the stored copy is identical to what was issued.

This is where the photo-album metaphor bites back one last time: you can switch to a live feed for issuance, but you still have to prove, years later, that the recorded footage was never edited. That's the gap most ERP implementations miss. The full treatment of the three archiving pillars (original format, integrity, audit trail) and why secure storage isn't the same as compliant archiving lives in our e-invoice archiving requirements guide. The deeper question of mathematical versus administrative integrity, why an admin or a system migration can quietly alter "secured" files and how cryptographic anchoring prevents it, is covered in tamper-proof vs. secure storage. For the timeline, the takeaway is simple: each deadline you meet on issuance creates a matching ten-year retention obligation you also have to meet.

For ERP and accounting platforms, that means three capabilities behind every mandate, receiving and issuing EN 16931-compliant invoices, storing them with verifiable integrity, and automating the audit trail, and the fastest route to all three is embedding a certified archiving REST API rather than building the subsystem yourself.

Formats and Infrastructure: A Quick Reference

The single most useful fact for cross-border planning: most national formats are profiles of one shared semantic model, EN 16931. Implement that core correctly, add the right country profile, and you can generate compliant invoices for most EU markets. The data model itself is detailed in our EN 16931 explainer.

| Format | Standard | Markets |

|---|---|---|

| XRechnung | EN 16931 (XML/CII) | Germany |

| Factur-X | EN 16931 (PDF/A-3 hybrid) | France, Germany |

| UBL 2.1 | EN 16931 | Belgium, Romania, Croatia |

| FacturaE | National XML | Spain |

| KSeF XML | National schema | Poland |

A few infrastructure notes that shape the timeline:

- Peppol is the delivery backbone for several of the mandates above (Belgium, German public procurement, the Nordics, and a growing list). It connects senders and receivers through certified access points; the full four-corner model is explained in our Peppol network guide.

- eIDAS seals authenticate high-volume automated invoicing at the organisation level under the eIDAS Regulation, applied programmatically without a human in the loop.

- Data residency isn't optional. GDPR rules and national data-sovereignty requirements mean invoice archives holding personal data must stay inside defined geographic boundaries, and multi-tenant systems must keep customers strictly separated.

- Format validity is the trap that catches teams late. A plain PDF generally won't satisfy these rules; see whether a PDF still counts as a valid invoice for why.

Conclusion: Plan Against the Dates, Not the Hype

The EU's e-invoicing transformation isn't a single event. It's a rolling series of national mandates, each with its own dates, transmission infrastructure, and retention rules, converging on ViDA by 2030. Treat each one as an isolated IT project and you'll spend five years in catch-up. Plan against the master table above, and the deadlines become predictable instead of disruptive.

The cheapest way to clear them is to stop building plumbing you don't have to. Whether to construct a compliant archive in-house or buy one is its own decision, weighed in our build vs. buy analysis; for software vendors who want to ship it under their own brand, white-label e-invoice archiving and a drop-in compliant retention API cover the integrity layer without a multi-year project.

Explore how OriginVault's white-label archiving layer for e-invoicing compliance gives ERP vendors certified infrastructure to meet every EU mandate on this timeline, without building it from scratch.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.