France's 2026 E-Invoicing Mandate: Impact on German Suppliers

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

France's 2026 E-Invoicing Mandate: Impact on German Suppliers

September 2026 is not a distant deadline. For German companies with French B2B customers, it is a hard technical cutover that decides whether your invoices get processed or rejected. France is rolling out one of the most ambitious fiscal digitization programs in Europe, and the compliance perimeter reaches well past French borders. If your ERP still emails PDF invoices to French clients, you have a problem to solve now, not in the autumn of 2026.

Here is the thing. Sending a PDF invoice to a French buyer after September 2026 is like faxing a handwritten order to a warehouse that only accepts database entries. The fax gets filed, maybe. The database entry gets read, validated, and acted on automatically. France is building the database. Your invoices need to speak its language, and so does whatever you keep them in afterward.

That last part is what most of this article is about. Plenty of guides cover the French deadlines and formats, and we link to ours below. The question almost nobody answers cleanly is the one a German exporter actually has: when the same invoice has to satisfy two tax authorities at once, German and French, where do the two rulebooks diverge, and who has to do what?

The 2026 Shift, in One Paragraph for German Exporters

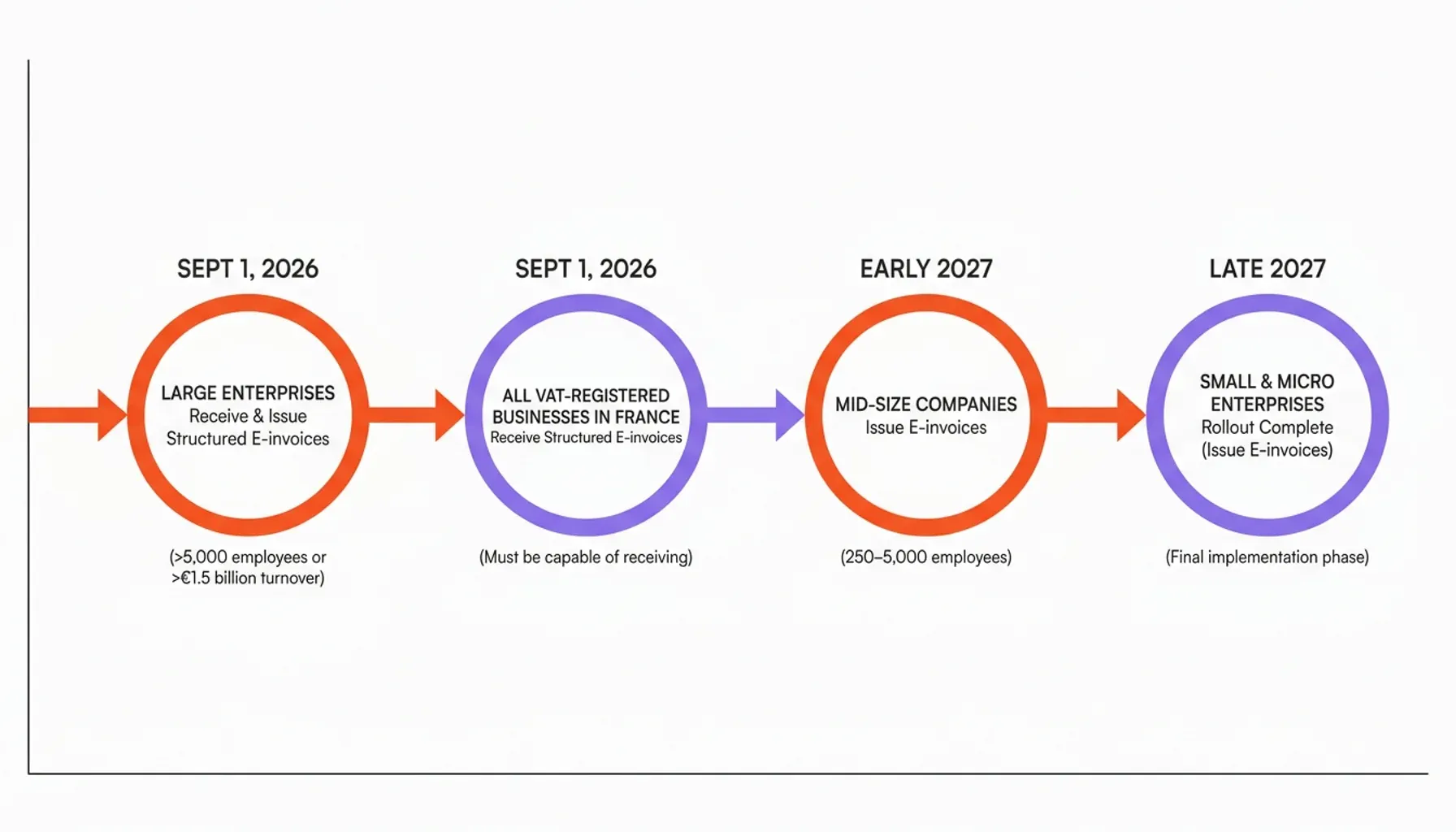

You do not need the full French timeline rehearsed again here. The short version: under the Direction Générale des Finances Publiques (DGFiP), France phases in mandatory structured B2B e-invoicing from September 1, 2026, with mid-size and small companies following through 2027, and it accepts three formats (Factur-X, UBL, CII). The one date that matters for you as a sender is also September 1, 2026: from that day every VAT-registered business in France must be able to receive a structured e-invoice. Send them a plain PDF after that and their system can refuse it. The full phased table, the employee and turnover thresholds, and the penalty schedule live in our dedicated breakdown of the France 2026 deadlines, formats, and penalties — start there for the calendar, then come back here for the cross-border mechanics.

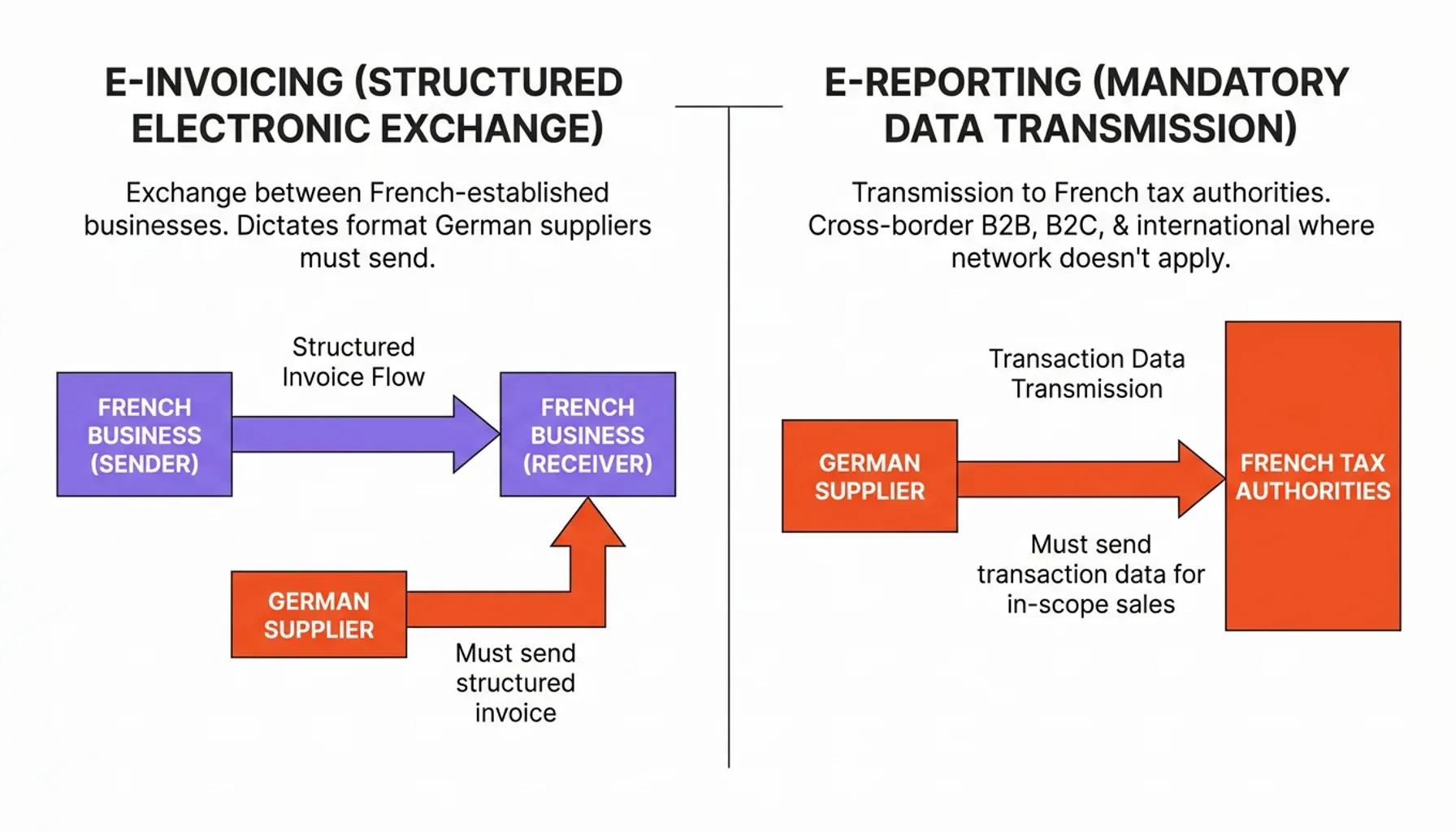

One framing is worth fixing in your head, because everything else hangs off it. The reform creates two separate obligations, and a German company can be caught by either or both:

- E-invoicing — the structured exchange of invoices between businesses established in France. Because French buyers must be able to receive these from September 2026, this is what dictates the format you have to send.

- E-reporting — transmitting transaction data to the French tax authority for sales that don't travel through the domestic e-invoicing network: cross-border B2B, B2C, and certain international flows.

France is running ahead of the EU pack here, but not off on its own. The mandate is an early, aggressive instance of the VAT in the Digital Age (ViDA) reform that will pull every member state toward real-time digital VAT reporting. Treat France as a local quirk and you will simply rebuild the same plumbing for Italy, Poland, and Belgium a year or two later.

Are You Actually In Scope? The French VAT Trigger

This is the question that decides everything else, and it has a sharper answer than most German finance teams assume. It hinges on one fact: do you hold a French VAT number?

Out of scope for e-invoicing (but watch e-reporting)

If your German company sells B2B into France without a French VAT registration, your invoices do not flow through the French e-invoicing network at all. You are a foreign supplier, the buyer receives your invoice from outside the system, and the e-invoicing format rules technically do not bind you. What can still reach you is e-reporting — more on who carries that in a moment.

In scope: the trigger that pulls you into the domestic perimeter

Here is where German companies misread their own exposure. The exemption for foreign suppliers evaporates the moment you hold a French VAT number — and you may hold one without thinking of yourself as a "French" business at all. The common triggers:

- You import goods into France and clear them under your own VAT registration.

- You maintain a fiscal representative or an establishment on French soil.

- You carry out taxable transactions physically located in France (installation, on-site work, local stock).

Any one of these registers you inside the French Tax Code (Code général des impôts) as a player in the domestic system. From that point you are not a foreign supplier emailing a PDF — you are a French-VAT-registered entity that must route invoices through an accredited channel, in a structured format, exactly like a French company.

Which channel, and who reports

France runs two accredited channels: the state portal PPF (Portail Public de Facturation, the expanded successor to Chorus Pro) and certified private platforms, the PDP (Plateformes de Dématérialisation Partenaires). The channel architecture itself is covered in the deadlines and formats guide; the only line that matters for you is the practical one. A French-VAT-registered German entity will almost always connect through a PDP rather than wrestling the raw PPF, because a PDP can plug into your existing ERP, convert your output, and push the e-reporting data on your behalf. That is the difference between a configuration project and a re-platforming project.

The receiving obligation, meanwhile, bites even if you are not registered in France. Your French customer must be able to ingest a structured invoice from September 2026. Keep sending PDFs and one of two things happens: their platform rejects the file, or their accounts-payable team re-keys it by hand and quietly starts treating you as the difficult vendor. Neither is a position you want to be in during a contract renewal.

For ERP vendors weighing how to embed audit-grade invoice archiving into their platform, the routing and registration calls made now decide how fast they can serve customers trading across both markets.

Factur-X and ZUGFeRD: Why German Suppliers Already Did the Hard Part

The good news for German exporters is short enough to state in one breath: Factur-X is technically identical to ZUGFeRD 2.1+ — same PDF/A-3 container, same Cross-Industry Invoice XML, same EN 16931 core — so a valid ZUGFeRD 2.1 invoice on the EN 16931 profile is already a valid Factur-X invoice. The two were deliberately aligned by Germany's FeRD and France's FNFE-MCE precisely so this would be true.

The payoff is the only part you really need to remember. If you implemented ZUGFeRD for Germany's own B2B mandate, you are not facing a new format build for France — you are facing a routing and validation change on top of output you already produce. For most German suppliers that turns "build a French e-invoicing capability" into "point the existing one at a PDP." If you are still untangling the German side, our XRechnung vs ZUGFeRD comparison is the place to settle that first.

What does not come for free is consistency between the two halves of the hybrid file. The PDF a human reads and the XML a machine parses must carry the same buyer name, invoice number, line amounts, and VAT rates. A mismatch is not a cosmetic bug — the PDP or PPF rejects the invoice on validation before your French buyer ever sees it. Treat the XML-versus-PDF check as a permanent gate in your generation pipeline, not a one-off QA pass. Where it helps to prove a given file was issued in a given state and never altered, that is a tamper-evidence problem rather than a storage problem, and we come back to it in the retention section.

E-Reporting: Which Obligation Actually Lands on You

E-reporting is how France captures VAT data for transactions that never touch the domestic e-invoicing rails. The generic taxonomy — cross-border B2B, B2C, intra-EU and OSS distance sales, and the exact field list and submission schema — is laid out in the deadlines and e-reporting breakdown, and the DGFiP publishes the technical e-reporting specification for the data model itself. I will not re-list all of it. Two things in it are genuinely yours to solve.

Who reports — supplier or buyer?

For a German company selling B2B into France without French VAT registration, the headline is that the transaction sits outside e-invoicing but inside e-reporting — and the reporting duty does not automatically land on you. As a rule the French-established buyer reports the purchase on its side. The ambiguity, and the reason this ends up in supplier contracts, is that the foreign supplier can also carry a reporting obligation depending on the transaction, and a French buyer whose input VAT deduction depends on the data being correct will increasingly demand contractual proof that you reported it. So the practical answer is not "the buyer handles it" — it is "agree in writing who handles it, before the first invoice." If you sell direct to French consumers through e-commerce, the B2C reporting obligation is unambiguously yours.

The mapping gap nobody scopes for

Here is the cross-border wedge that German guides skip. German accounting is built around GoBD data fields, German VAT codes, and DATEV-compatible export. The French e-reporting schema speaks a different language — different field names, a different VAT-code structure, and French identifiers instead of German ones. The seam shows up in a single concrete field.

Take buyer identification. Your DATEV records key a French customer by its German-side debtor number and, where present, a USt-IdNr.-style VAT ID. French e-reporting wants the buyer keyed by its SIREN (the 9-digit legal-entity number) or SIRET (the 14-digit establishment number — SIREN plus a 5-digit site code). Those are not derivable from a German tax number; they have to be captured, stored against each French counterparty, and emitted in the French layout. Miss the establishment-level SIRET on a customer that invoices from two sites and your report attaches the transaction to the wrong entity. Multiply that one mismatch across a customer master and you have an audit flag waiting to happen.

That mapping problem is, underneath, an integrity problem. If the numbers you report to France drift from the numbers on the original invoice — even by an honest mapping slip — the discrepancy is exactly what a tax auditor's reconciliation is built to catch. The cleaner pattern is a single sealed source of truth: one tamper-evident record of the invoice from which both the German GoBD obligation and the French e-reporting obligation are served, so there is no second copy to drift out of step with the first.

Retention: Where GoBD and French LPF Pull Apart

Generating a compliant Factur-X invoice is step one. Keeping it so that two national tax authorities are satisfied at the same time is the harder job, and it is the one this article exists to nail down. Both regimes want roughly ten years of retention — Germany's GoBD and France's Livre des Procédures Fiscales (LPF) both land near a decade, and the precise per-country durations are tabulated in our e-invoice retention periods by country. The mistake is assuming "ten years both sides" means one rulebook. It does not.

GoBD vs French LPF, side by side

The German GoBD requirement compresses to a pointer: the document must stay retrievable in its original state for the full period — original file, original metadata, machine-readable, not a printout or a re-export. Full criteria are in the GoBD archiving guide.

Where France diverges is the part that catches German teams off guard. The LPF does not just want the original file kept — it wants each stored e-invoice backed by an integrity guarantee, in practice a qualified electronic signature, a qualified seal, or an equivalent audit-trail proof, demonstrating the invoice's authenticity and that its content is unaltered. So the two regimes agree on duration and on originality, but France adds a cryptographic-integrity demand that GoBD frames more as a process control. A folder on a file server can arguably satisfy a loose reading of GoBD; it does not satisfy the LPF. That gap — same invoice, same shelf life, but France insisting on provable integrity per document — is the real dual-jurisdiction problem, and it is why "we already archive for GoBD" is not a complete answer for French-facing trade.

One mechanism that covers both

Because the binding constraint is provable, per-document integrity, the efficient move is to satisfy the stricter regime and let it cover the looser one. Anchoring each invoice's cryptographic hash so any later change is detectable gives you a verifiable integrity guarantee that does not depend on trusting the storage vendor — the canonical treatment of why that beats ordinary "secure storage" is in tamper-proof vs secure storage and what auditors actually require. Pair it with two operational habits: log every event on the document — creation, transmission, receipt confirmation, and storage — in a tamper-proof trail; and, if you migrate a Factur-X file to new storage inside the retention window, log the migration and re-verify integrity rather than assuming it carried over. The ISO 14641-1 electronic-archiving standard gives the broader framework, but the implementation work lands on ERP vendors and their customers.

For ERP vendors aiming to offer tamper-proof, GoBD-ready invoice archiving as a native feature, the architecture chosen during 2025 is what decides September 2026 readiness — and whether one design can carry every later EU mandate too.

Strategic Implementation: Preparing Your Infrastructure for 2026

The companies that clear September 2026 without drama are the ones starting the assessment now. The steps run in sequence, not in parallel.

Step 1 — Map your French exposure. Pull every French B2B customer out of accounts receivable. Quantify invoice volume, current format, and how you transmit today. Critically, flag any French VAT registration. That single question tells you whether you are in the e-invoicing perimeter, the e-reporting one, or both.

Step 2 — Test what your ERP already emits. Check whether your system produces ZUGFeRD 2.1 / EN 16931 output natively. If it does, you are most of the way to Factur-X. If not, decide between a plugin, middleware, or a PDP that converts for you.

Step 3 — Select a PDP (or commit to PPF). For anyone with a French VAT number or meaningful French volume, the PDP choice is strategic, because it carries your validation, routing, and e-reporting submission. Judge candidates on API quality, depth of ERP integration, and whether they handle German-origin invoices without manual touch. Get sandbox access and run real test invoices before you sign.

Step 4 — Build the archive as a first-class layer, not an afterthought. A generated invoice is not a retained one. GoBD and the LPF both demand tamper-evident, auditable storage for the full period, and as covered above the LPF's per-document integrity bar is the one that sets the requirement. A hash-anchored archive that seals each invoice at creation and keeps an immutable trail satisfies both regimes from one mechanism.

Step 5 — Insist on a single point of truth. The failure mode is two compliance stacks — one German, one French — quietly drifting apart over the years. One sealed store that serves both jurisdictions is simpler to run and far easier to defend when an auditor asks you to reconcile what you invoiced against what you reported.

And the horizon is not French-only. ViDA extends real-time digital VAT reporting across the EU toward 2030. France is the leading edge of that wave, not a one-off — the infrastructure you stand up for the French mandate is the same infrastructure the Italian, Spanish, and EU-wide mandates will ask for next.

Conclusion: Two Rulebooks, One Sealed Record

The French mandate is not ambiguous. The formats are specified, the channels are accredited, the dates are fixed. For a German supplier with French B2B customers the open question was never whether to comply — it is whether one system can carry the German and French obligations at once without them drifting apart.

Treat it as a pure IT project and you will pass the format check but miss the LPF's integrity-and-retention bar. Treat it as a pure compliance exercise and you will get the paperwork right while your ERP still emails PDFs. The frame that actually works is a single integrated record: structured generation, accredited routing, and tamper-evident archiving that serves GoBD and the LPF from the same sealed source of truth — so there is never a second version to reconcile.

For ERP vendors on the German-French corridor, that same record is a product. If you want to ship it rather than build it from scratch, white-label, blockchain-sealed e-invoice archiving that is e-invoicing- and GoBD-ready drops the dual-jurisdiction layer straight into your platform.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.