E-Invoicing France 2026: Deadlines, Formats & Penalties

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

A mid-size Lyon manufacturer receives an invoice in PDF format on October 1, 2026. Their ERP rejects it. Their supplier doesn't get paid. That sequence is now a legal failure, not just an operational one.

France isn't asking businesses to prepare for e-invoicing. It's requiring it, by law, with penalties attached, and on a fixed timeline that leaves no room for last-minute scrambling.

The French e-invoicing mandate is the most significant shift in B2B transaction infrastructure France has seen in decades. Every company selling goods or services to another French business will need to issue and receive structured electronic invoices through a certified platform, or face fines, audit exposure, and operational disruption. There is no opt-out and no informal workaround.

For ERP vendors, software providers, and finance teams operating in France, the window between now and September 2026 is not a grace period. It is a preparation mandate.

Here is what the deadlines look like, what the technical requirements demand, and what the real cost of non-compliance will be.

Why France Is Forcing Structured E-Invoicing by 2026

France's push toward mandatory e-invoicing is not a bureaucratic exercise. The primary driver is fiscal. VAT fraud costs the French state billions of euros annually, and structured electronic invoicing closes the reporting gaps that make fraud possible.

The mandate turns what was previously a voluntary practice into a legal obligation for all B2B transactions between French VAT-registered entities. This is not a pilot program or a phased recommendation. It is a structural overhaul of how commercial transactions are documented, reported, and stored.

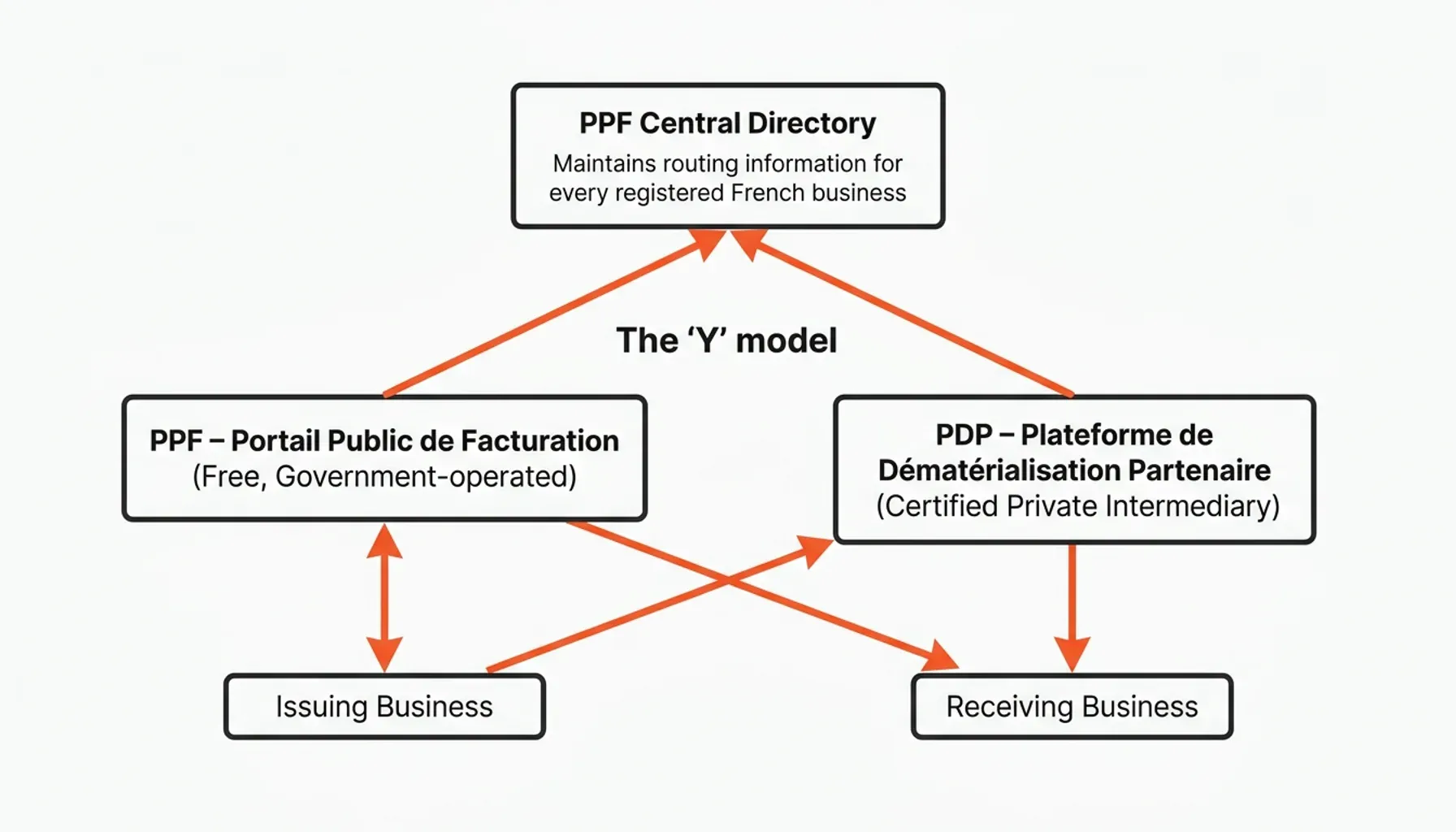

Central to the architecture is the so-called "Y" model. Businesses can route their invoices through two types of platforms: the Portail Public de Facturation (PPF), a free public portal operated by the French government, or a Plateforme de Dématérialisation Partenaire (PDP), a certified private intermediary. Both connect to the PPF's central directory, which maintains routing information for every registered French business.

The original 2024 implementation date was delayed, a decision that reflected the complexity of the infrastructure build rather than a softening of political will. The new deadline of 1 September 2026 is firm. The Direction Générale des Finances Publiques (DGFiP) has been explicit: this delay exists to give businesses and platforms time to build correctly, not to defer the obligation indefinitely. The revised calendar is written into the 2024 Loi de finances, Article 91, which sets both the phased dates and the conditional extension window.

For ERP vendors and software providers, this window is the critical opportunity to embed compliant invoicing and archiving infrastructure before the mandate creates a compliance emergency. The French rules build directly on the EU-wide EN 16931 semantic data model, which defines what a structured invoice actually contains.

The Roadmap: Mandatory Deadlines for Reception and Issuance

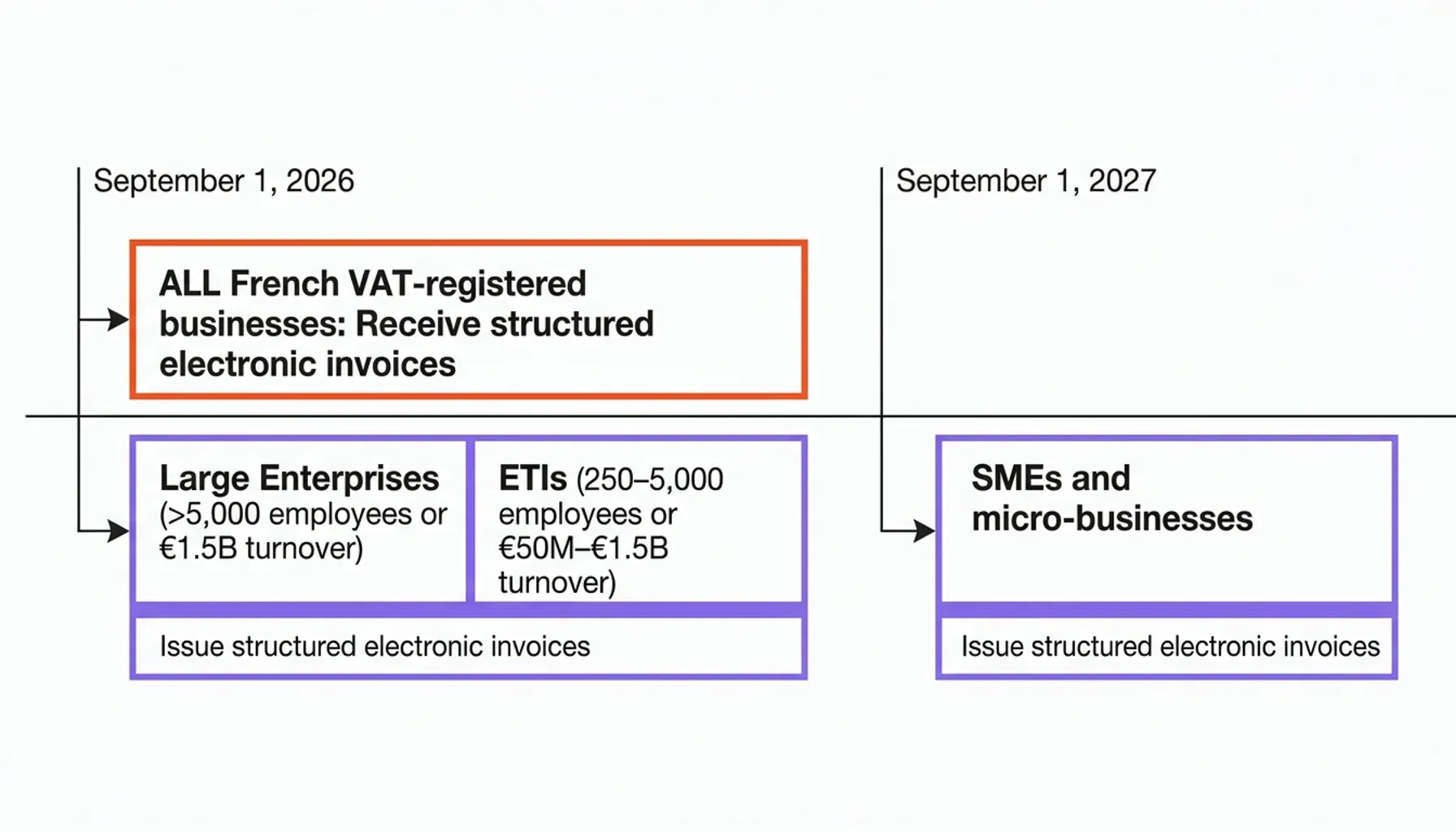

The French mandate rolls out in two distinct waves, separated by company size. Understanding which deadline applies to your business, or to your customers if you are an ERP or software vendor, is the first operational decision you need to make.

September 1, 2026: The Universal Reception Deadline

Every French VAT-registered business, regardless of size, must be capable of receiving structured electronic invoices by 1 September 2026. This applies equally to a sole trader and a multinational corporation, with no exemption for the smallest firms.

Every business needs a compliant receiving channel, either the PPF or a certified PDP, operational before this date. Planning it or putting it out to procurement is not enough; the channel has to be live and tested.

September 1, 2026: Large Enterprises and ETIs Must Issue

On the same date, large enterprises (more than 5,000 employees or over €1.5 billion in annual turnover) and mid-size companies (ETIs) (250 to 5,000 employees, or €50 million to €1.5 billion in turnover) must begin issuing structured electronic invoices for all domestic B2B transactions.

These companies are the logical starting point: they generate the highest invoice volumes and have the IT infrastructure to adapt. Their compliance also creates downstream pressure on SME suppliers, who must be capable of receiving those invoices from day one. If you supply a large enterprise and you can't receive a structured invoice, you become their problem.

September 1, 2027: SMEs and Micro-businesses Must Issue

Small and medium enterprises (SMEs) and micro-businesses have an additional twelve months to achieve issuance compliance. Their mandatory issuance deadline is 1 September 2027.

This staggered approach acknowledges that smaller businesses have fewer internal resources to restructure invoicing workflows. The reception obligation still applies from September 2026, so even micro-businesses cannot wait until 2027 to engage with the mandate. The clock is already running.

The Extension Window

The 2024 Finance Act introduced a provision allowing a potential three-month extension for each deadline phase, subject to a formal government decision. This is a contingency mechanism, not a planning assumption. Any business or ERP vendor building a compliance strategy around the hope of an extension is taking a real and unnecessary risk.

E-Reporting: The Parallel Obligation

Alongside e-invoicing, the mandate introduces e-reporting: the obligation to transmit transaction data to the DGFiP for B2C sales and cross-border B2B transactions not covered by the domestic invoice mandate. E-reporting runs on the same timeline as e-invoicing issuance, with the same platform infrastructure.

This is not a secondary consideration. It is an equal compliance requirement, with its own separate penalty structure, which I'll cover in detail below.

Technical Standards: Factur-X, UBL, and CII

The French mandate does not accept a PDF invoice sent by email. It requires structured data, machine-readable information that platforms can process, validate, and report automatically. France rejects emailed PDFs precisely because a flat PDF is a picture of an invoice, not the structured invoice data the platforms need; the reasons a plain PDF no longer counts as a valid e-invoice are covered in detail in our guide to whether a PDF is still a valid invoice in 2026.

Factur-X: The French Format of Choice

Factur-X is the preferred format for the French market. It is a hybrid document that pairs a human-readable PDF with an embedded XML data file, so finance teams keep their familiar view while platforms read the structured layer underneath. The full mechanics of how that hybrid PDF-plus-XML container is built, and which profiles to use, are covered in our Factur-X format guide. The format was co-developed by France and Germany, which makes it directly compatible with the ZUGFeRD format used by German suppliers selling into France. Its structured layer conforms to the European semantic model defined in EN 16931, the same data model that anchors the wider EU VAT in the Digital Age (ViDA) move toward real-time fiscal transparency. That semantic model itself rests on Directive 2014/55/EU, the EU instrument that first mandated a common European e-invoicing standard. The Factur-X specification is maintained by the FNFE-MPE, the French national e-invoicing forum.

UBL and CII as Accepted Alternatives

The mandate also accepts invoices in Universal Business Language (UBL) and Cross Industry Invoice (CII) formats. Both are internationally recognized XML standards for structured business documents. UBL is widely used in public procurement across Europe; CII is the XML syntax underlying Factur-X's structured data layer.

Choosing between these formats is not just a technical decision. It's a strategic one. If your customers operate across borders, UBL's broader European adoption may matter. If you're focused on the French domestic market, Factur-X is the path of least resistance.

The Role of the PDP in Format Validation

A certified PDP does more than route invoices. It validates format compliance before transmission, rejecting invoices that fail structural or data integrity checks. This makes PDP selection a technical decision, not just a commercial one. A PDP that validates rigorously protects its customers from penalty exposure. One that doesn't creates hidden compliance risk that surfaces only during an audit.

For ERP vendors building white-label invoice archiving infrastructure for their customers, format validation and compliant storage have to be treated as a single integrated workflow, not two separate problems.

What Happens When Validation Fails?

Here's a scenario worth thinking through. Your customer issues 3,000 invoices in September 2026. Their PDP rejects 200 of them for structural errors: missing buyer VAT identifiers, incorrect currency codes, malformed XML. Those 200 invoices don't get transmitted. The buyers don't receive them. Payment cycles stall. And the DGFiP's directory shows a gap between expected and received invoice volumes.

That's not a technical glitch. That's a compliance event with financial and audit consequences. Getting format validation right before go-live is not optional polish. It is the whole game.

Non-Compliance Costs: The €15-per-Invoice Penalty

The French tax code does not leave the cost of non-compliance to imagination. The penalties are specific, documented, and cumulative.

The Core Penalty: €15 Per Invoice

Under French Tax Code provisions, failure to issue a compliant electronic invoice, or failure to issue one at all when required, triggers a fine of €15 per missing or non-compliant invoice. This penalty is capped at €15,000 per calendar year.

At first glance, €15 per invoice sounds manageable. Do the math. For a business issuing 500 invoices per month, the annual exposure reaches €90,000 before the cap applies. The cap doesn't eliminate the operational disruption or the audit risk that non-compliance creates. It just limits the direct fine. The indirect costs are another story entirely.

E-Reporting Penalties

Failures in e-reporting, meaning missing or late transmission of transaction data to the DGFiP, carry a separate penalty of €250 per failed transmission, also capped at €15,000 per year. These are independent of the invoicing penalties, meaning both caps can apply simultaneously. You can hit €30,000 in annual fines before a single tax auditor walks through the door.

The Audit Trigger Risk

The deeper financial risk is not the fine itself. The PPF's central directory creates a real-time data trail. Inconsistencies between invoices issued, invoices received, and VAT declarations become visible to the DGFiP automatically. Non-compliant businesses don't just face a fixed penalty. They flag themselves for tax audit.

The ViDA framework, which France's mandate anticipates, is designed precisely to create this kind of fiscal transparency. The e-invoicing infrastructure is, fundamentally, a real-time tax reporting infrastructure. Every invoice is a data point in a system designed to catch discrepancies.

Operational and Commercial Consequences

Most companies get this wrong. They focus on the fine and ignore the payment friction. A buyer's accounts payable system that expects structured electronic invoices will reject or delay processing a non-compliant document. In B2B relationships with large enterprises, which must comply from September 2026, a supplier who cannot issue compliant invoices becomes a liability, not a partner.

Think about what that means in practice. You lose payment speed. You lose goodwill. You may lose the contract. The €15 fine is the least of your problems.

Beyond the Transaction: The 10-Year Archiving Obligation

Issuing and receiving compliant invoices is the visible part of the mandate. The less visible, and consistently underestimated, obligation is long-term archiving. This is where most businesses and ERP vendors fall short.

The 10-Year Retention Requirement

Under French commercial law, accounting documents including invoices must be retained for 10 years. This is not a recommendation. It is a legal minimum, and tax authorities can demand access to archived invoices during an audit covering any year within that window. (The retention clocks differ from country to country, so vendors serving several markets should check our overview of e-invoice retention periods by country rather than assume the French figure applies everywhere.)

Storing a file on a server satisfies none of this on its own. Across the full ten years, a French archive has to keep each invoice intact, legible, and retrievable, and it has to be able to prove that integrity on demand. That last point is the one most teams skip: a server folder shows what a file looks like today, not whether it has changed since it was issued.

Storage Is Not the Same as a Defensible Archive

There is a critical difference between storing a document and archiving it in a way that holds up to an audit. The three pillars of a defensible archive (keeping the original format, proving integrity, and preserving an audit trail) are covered in depth in our guide to e-invoice archiving requirements and audit trails. The short version: a file saved to a cloud storage bucket can be modified, deleted, or corrupted, and if it is, nothing proves what the original contained.

That is why a French archive needs to be provably tamper-proof, not merely stored in a secure location. The cryptographic mechanics behind that proof, and the "Admin Paradox" that explains why even an administrator with full database access cannot quietly alter a sealed record, are covered in our comparison of tamper-proof versus secure storage. For a French e-invoice held under a 10-year mandate, that distinction is the line between a storage system and a compliance system. One holds up in an audit; the other does not.

Strategic Implementation: Preparing Your ERP for 2026

The mandate is fixed. The question is execution quality. Businesses and ERP vendors that treat 2026 as a compliance checkbox will build fragile infrastructure. Those that treat it as a platform modernization opportunity will build durable competitive advantage.

Step 1: Audit Current Invoicing Workflows

The first task is an honest assessment of the current state. Most businesses still issue invoices in formats that are not mandate-compliant. Some send flat PDFs. Others rely on Word documents. Many export straight from proprietary ERP systems that produce no structured XML at all. The gap analysis should cover:

- Current invoice formats and whether they carry structured XML data

- Existing connections to any e-invoicing platform or EDI network

- The volume of invoices issued and received monthly, segmented by customer size

- Current archiving practices and retention periods

Don't soften this assessment. The gap is probably larger than you think.

Step 2: Choose Between PPF and PDP

The PPF is free and government-operated. It is the baseline option for businesses with straightforward domestic invoicing needs. The PDP route offers additional services, including format validation, workflow automation, ERP integration, and value-added data services, but requires selecting a certified private partner.

For ERP vendors, the PDP decision is also a product decision: building PDP connectivity into the ERP platform creates a stickier, more valuable product for customers. It's not just compliance infrastructure. It's retention infrastructure.

Step 3: Automate E-Reporting

E-reporting for B2C and cross-border transactions cannot be an afterthought. It runs on the same infrastructure as e-invoicing but covers a different transaction set. Automation is the only practical approach at scale. Manual e-reporting submissions create error risk and operational overhead that compounds quickly at volume.

Step 4: Put Compliant Archiving in Place Before Go-Live

The worst time to solve the archiving problem is after the first compliant invoice has been issued. Archiving infrastructure needs to be in place and tested before the mandate takes effect. For ERP vendors, that means deciding now whether to build a retention engine in-house or embed one, rather than waiting until Q3 2026. Every month of delay is a month of engineering time you don't get back.

Step 5: Treat Invoice Data as an Asset

The infrastructure France is building is not just a compliance layer; it is a data infrastructure. Businesses that structure their invoice data correctly from day one get richer financial analytics, faster reconciliation, and cleaner audit trails. The mandate creates the obligation, but the businesses that win are the ones that treat it as a platform rather than a constraint, an open-innovation posture that turns a regulatory cost into a product capability.

Conclusion: 2026 Is a Technical Deadline and a Strategic Inflection Point

The French e-invoicing mandate is one of the most operationally significant regulatory changes in European B2B commerce in a decade. The deadlines are fixed, the penalties are real, and the archiving obligations extend a decade beyond the first compliant invoice.

For businesses operating in France, the path forward is clear: structured formats, certified platforms, and audit-proof archives, all operational before September 2026. For ERP vendors serving French customers, the mandate is simultaneously a compliance obligation and a product opportunity.

That product opportunity comes down to one choice: build a compliant archive in-house or embed one. The full build-versus-buy trade-off rarely favors building a retention engine from scratch once you account for the ongoing compliance maintenance. The faster route is a white-label archiving engine for software vendors that ships under your own brand. If you are an ERP or software provider weighing how to meet the 10-year French archiving mandate for your customers, explore OriginVault's white-label invoice archiving and e-invoicing compliance engine, built to embed in a single API integration, under your brand, with blockchain-sealed data integrity included.

The Lyon manufacturer whose supplier couldn't send a compliant invoice? That's a preventable failure. The tools, the standards, and the timeline are all known. What's left is execution.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.