What Revisionssichere Archivierung Means for E-Invoices

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

The German Standard: Decoding Revisionssichere Archivierung

A tax auditor requests seven years of invoice records. Your system produces them, but can you prove not a single byte has changed since the original was stored? In Germany and Switzerland, that proof is not optional. It is the legal baseline.

The duty starts long before any cloud or blockchain enters the picture. German commercial and tax law (HGB §257 and AO §147) obliges businesses to retain bookkeeping records, including electronic invoices, in a form that stays complete, orderly, and unaltered for the statutory period. Revisionssichere Archivierung is the discipline that operationalizes those duties: it is how you keep records audit-proof, not merely backed up. The most widely cited working definition comes from the VOI and the KRM in their "Merksätze zur Revisionssicherheit", a set of plain-language criteria that German auditors and IT departments treat as the practical yardstick. The term is German, but its reach extends to every software vendor, ERP platform, and finance team operating in the DACH region.

Here is the distinction the rest of this article argues. Revisionssicher is not a synonym for "tamper-proof storage". A file can be cryptographically sealed and still fail the standard, because Revisionssicherheit is a legal-completeness-plus-traceability test, not just an immutability test. It asks whether the whole of your record-keeping is captured, ordered, retrievable, and demonstrably unchanged across a decade. Sealing solves one piece of that. The concept covers the rest.

The stakes have sharpened considerably. Germany's mandatory B2B e-invoicing rollout, phased in from 2025, means structured electronic invoices in formats like XRechnung and ZUGFeRD are no longer edge cases. They are the default, and every one of them must be archived in a revisionssicher manner from the moment it is received or issued.

Standard cloud storage does not meet this bar. Dropping a PDF in an S3 bucket, even with versioning switched on, provides no defensible proof that the file has not been modified, and no structured record of who touched it or when. That gap between "stored somewhere" and "audit-proof" is the entire reason the German concept exists, and the reason a generic compliant-archiving checklist is not enough.

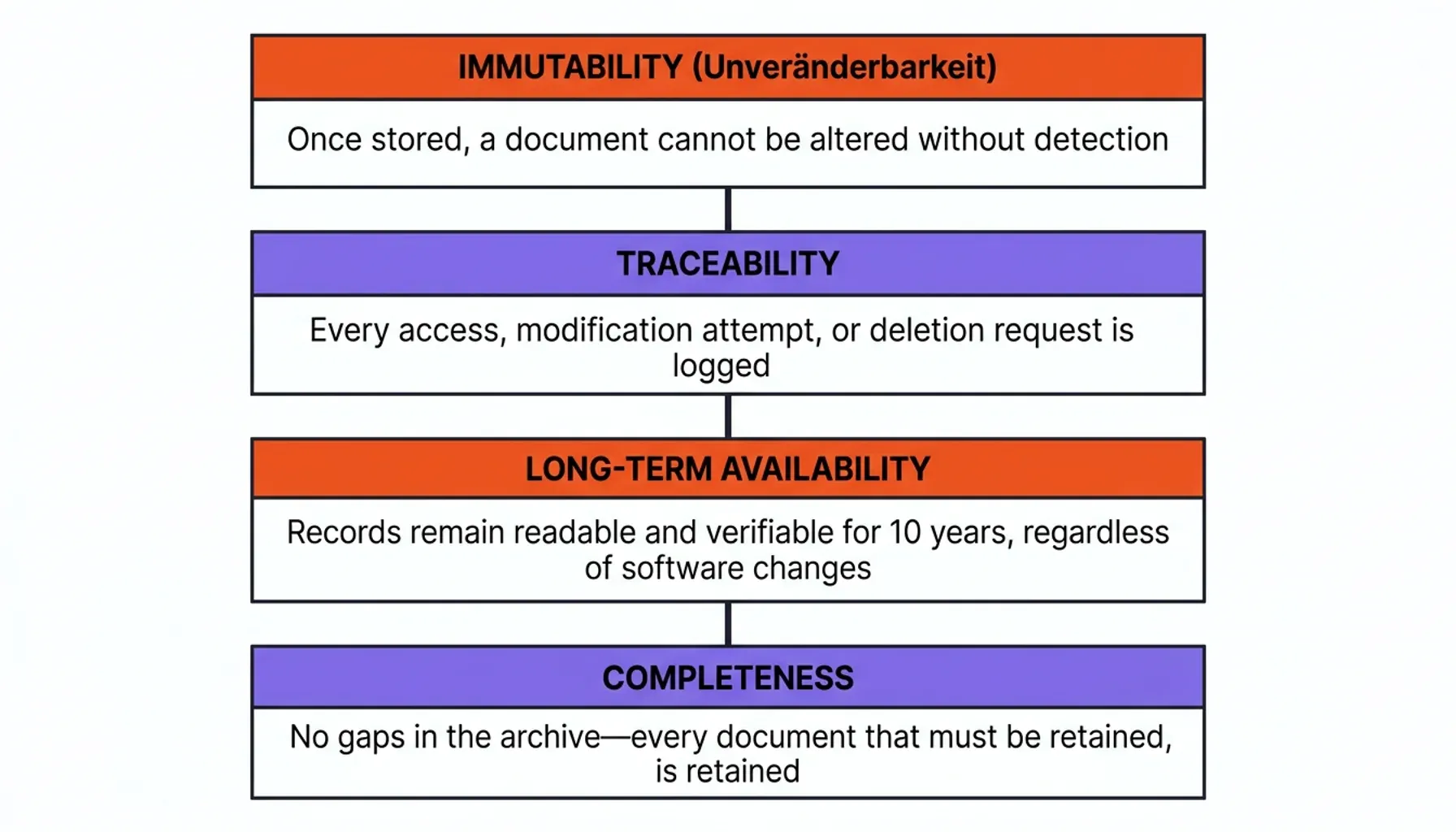

So what does the law actually require a revisionssicher archive to demonstrate? Four legal criteria sit at the heart of the VOI/KRM definition:

- Unveränderbarkeit (immutability): once stored, a document cannot be altered without the change being detectable.

- Vollständigkeit (completeness): every record subject to retention is captured, with no silent gaps.

- Nachvollziehbarkeit (traceability): every access, change attempt, and deletion request is logged and itself protected.

- Verfügbarkeit (long-term availability): records stay readable and verifiable for the full retention period, independent of any single software product.

These are the definition of the term, not a generic feature list. The broader, vendor-neutral breakdown of archiving pillars (original format, integrity, audit trail) belongs to a dedicated treatment; what matters here is that all four criteria must hold together for an archive to count as revisionssicher.

The Legal Framework: GoBD in Germany, GeBüV in Switzerland

In Germany, the GoBD (Grundsätze zur ordnungsmäßigen Führung und Aufbewahrung von Büchern) is the regulatory ground on which Revisionssicherheit rests. Issued by the Federal Ministry of Finance, it translates the HGB and AO retention duties into concrete principles for digitally stored records: immutability, capture in the original format, the 10-year retention period, machine-readability, and a documented Verfahrensdokumentation. Those mechanics, and how to satisfy them in practice, are covered in depth in the guide to GoBD-compliant e-invoice archiving. For this article, the point is narrower: GoBD is the German legal basis a revisionssicher archive must satisfy, and failing even one principle is enough for an auditor to reject the whole archive.

Switzerland is where the DACH split gets interesting, and where this concept earns its keep. The Swiss GeBüV (Geschäftsbücherverordnung) shares GoBD's intent but specifies it differently. Articles 9 and 10 are the load-bearing clauses. Article 9 governs Integrität (integrity), it requires that records be stored so that any later alteration can be detected, the formal anchor for unveränderbare Aufbewahrung in Swiss law. Article 10 governs Verfügbarkeit und Lesbarkeit: records must remain accessible and machine-readable throughout the retention period, with the information needed to read them preserved alongside the data itself.

Crucially, GeBüV leans on demonstrable conformity rather than self-attestation. A Swiss archiving solution is expected to show that its integrity protection (Integritätsschutz) actually works, which is why independent certification carries real weight in the Swiss market. OriginVault holds KRM (Kompetenzzentrum Records Management) certification for GeBüV compliance, a distinction that speaks directly to Swiss ERP vendors and their end customers, because it shifts the integrity question from "trust us" to "here is the audited proof". This Swiss layer, GeBüV Art. 9–10 plus recognized certification, is what separates a genuinely DACH-ready audit-proof archive from one tuned only for the German GoBD.

The 10-year retention duty is shared across both jurisdictions, and it is where theory meets engineering. A document archived today must be retrievable and verifiable in 2035, in a format a tax authority can actually open and validate. That rules out undocumented proprietary formats and any architecture where the vendor's continued existence is a precondition for reading the data, a constraint that resurfaces under both GoBD and GeBüV.

What Unveränderbarkeit Demands Technically

The Unveränderbarkeit criterion is met technically by cryptographic sealing rather than access policy. In short: each archived e-invoice is hashed, and that fingerprint is anchored to infrastructure no single administrator controls, so any later change to the file becomes mathematically detectable rather than merely "logged". This closes the gap that ordinary storage cannot, where a privileged user could alter a record and its local checksum together without leaving a trace.

The deeper mechanics, the tamper-proof versus secure-storage distinction, the role of the SHA-256 fingerprint, the "admin paradox" of self-certified integrity, and why mathematical proof beats administrative control, are treated in full by the dedicated comparison. What belongs here is the consequence for Revisionssicherheit: an archive satisfies Unveränderbarkeit only when integrity can be proven independently of the system that holds the data. A sealed-and-anchored record clears that bar; a version-tracked document in an editable repository does not, however careful the access controls.

That independence is also what gives the Swiss Integritätsschutz requirement teeth. Article 9 GeBüV does not ask whether your access policy is strict; it asks whether alteration would be detectable. Cryptographic sealing answers yes by construction, which is precisely why it has become the default technical route to a revisionssicher archive across the DACH region.

Audit Trails and Version Control in E-Invoicing

An archive without a complete audit trail is an archive waiting to fail an inspection. Revisionssichere Archivierung does not just require that documents be stored. It requires that every interaction with those documents be logged, timestamped, and itself protected from modification, the Nachvollziehbarkeit criterion made operational.

For e-invoices, that produces a layered logging requirement:

- Receipt logging: when was the invoice received, from which system, in which format?

- Access logging: who retrieved the document, when, and for what purpose?

- Modification-attempt logging: were any changes attempted, and were they blocked?

- Deletion-attempt logging: was a deletion requested, by whom, and was it authorized?

Archived invoices arrive either as XRechnung XML or as a ZUGFeRD hybrid PDF, and the choice between those formats is its own subject covered in the XRechnung vs ZUGFeRD comparison. What matters for audit-proof archiving is that the system preserves the original bytes of whichever it receives: the structured XML state must never be silently overwritten by a rendering step or a format conversion, because the moment that happens, the original record, and its proof, is gone.

This becomes critical during system migrations, and it is where many archives quietly break. When an ERP vendor upgrades its platform, the archiving layer must guarantee that migrated documents keep their original cryptographic fingerprints. A migration that re-renders PDFs or re-encodes XML without preserving the original hash chain destroys the immutability proof and can invalidate years of archived records, a failure that surfaces only when an auditor asks for verification, long after the migration is forgotten.

Multi-tenancy is the operational reality for any provider managing archives at scale. A platform serving 10,000 end customers must keep each archive cryptographically isolated, so that shared infrastructure never means shared risk. For a fuller picture of what a properly structured ERP archive entails, this overview of ERP archive requirements is worth examining.

The Vendor Decision: Embed Compliance, Don't Rebuild It

For software vendors, a revisionssicher archive is rarely something worth building from scratch. The engineering cost is real, the certification process is slow, and tracking regulatory change across Germany, Switzerland, Austria, and the wider EU never stops, none of which is core to the product's actual value. The cleaner path is to embed a certified compliance layer via API, white-labeled under your own brand, so the archiving infrastructure is run by a provider whose entire business is staying certified and guaranteeing decade-long retention.

That decision splits into three questions other articles handle in depth: the build-vs-buy decision and its true total cost, how white-label archiving handles brand, multi-tenancy, and liability transfer, and how compliance becomes a revenue stream for EDI and accounting platforms rather than a cost. The thread tying them together is liability: when an auditor rejects an archive, the exposure lands on the ERP vendor, not on a generic cloud host.

For vendors evaluating this route, OriginVault's white-label e-invoicing archiving layer is built for exactly it, a single API integration delivering GoBD-compliant, GeBüV-certified, blockchain-sealed, multi-tenant invoice archiving under the vendor's own brand.

Common Pitfalls in Digital Archiving and How to Avoid Them

The gap between what organizations believe constitutes compliant archiving and what actually passes a GoBD or GeBüV audit is wider than most finance teams realize. Three mistakes recur.

Mistaking backups for archives. A backup restores a system to a previous state; a tamper-evident archive is an independently verifiable record of a document's original state. Backups live in the same administrative domain as the source data and can be overwritten; a revisionssicher archive requires cryptographic independence from that domain. The two serve different legal functions, and one cannot stand in for the other.

Treating version history as Unveränderbarkeit. Many teams store documents in systems that technically permit modification and rely on version history as a compensating control. A system that allows a change and logs it is not the same as one that prevents undetectable change by construction, and Swiss and German auditors increasingly know the difference.

Vendor lock-in. Over a 10-year retention period, an archive readable only through one vendor's proprietary software is a structural liability, this is the open-format side of the build-vs-buy question. If that vendor is acquired, pivots, or shuts down, the compliance posture collapses with it. A revisionssicher archive keeps data exportable in open formats with proofs verifiable independently of the original system.

For the 2025 B2B e-invoicing mandate, four checks are worth running now:

- Confirm the archive can ingest and seal XRechnung and ZUGFeRD natively.

- Validate that the Verfahrensdokumentation is current and audit-ready.

- Test retrieval under audit conditions, not just functional conditions.

- Verify that the provider's GoBD and GeBüV coverage matches your specific use case.

The EU e-invoicing standard EN 16931 underpins both XRechnung and ZUGFeRD; its semantic model is prerequisite knowledge for any vendor building compliant invoice workflows. The format-level technical guidance for what archived records must contain, in turn, draws on bodies like FeRD and the audit-standard work of the IDW.

Where Audit-Proof Archiving Is Heading

Structured e-invoice data is starting to make the archive an active compliance asset rather than a passive storage cost. Because XRechnung is machine-readable by design, automated checks, cross-referencing invoice data against tax codes, supplier registrations, and payment terms, can run continuously instead of only at audit time. The record stops being something you dig up under pressure and becomes something the system reasons over daily.

Digital sovereignty is moving from preference to procurement requirement. Buyers in regulated sectors increasingly specify that data seals reside within European jurisdictions, Switzerland and the EU, where the rules governing data access are predictable and enforceable. Infrastructure hosted outside those jurisdictions introduces regulatory exposure that is hard to quantify and harder to fix after the fact, which is exactly why GeBüV certification and EU-resident sealing have become differentiators rather than footnotes.

There is a strategic reframe behind all of this. In the DACH region, a GoBD-compliant, GeBüV-certified archiving layer is not a feature a vendor adds for goodwill, it is a precondition for enterprise sales. Vendors who embed it through a modular, API-driven architecture stop paying the certification tax repeatedly and start treating audit-proof archiving as something customers will pay a premium for. And the transition does not demand a platform rebuild: modular sealing APIs add cryptographic immutability to existing document workflows without disturbing the surrounding architecture.

Conclusion

Revisionssichere Archivierung is not a bureaucratic formality. It is the legal-completeness-and-traceability standard, rooted in HGB §257 and AO §147, defined by the VOI/KRM Merksätze, and enforced through GoBD in Germany and GeBüV Art. 9–10 in Switzerland, that decides whether your invoice archive survives a tax audit, a regulatory inspection, or a court proceeding. It asks more than "is the file tamper-proof"; it asks whether the whole of your record-keeping is complete, ordered, traceable, and demonstrably unchanged for a decade. With Germany's B2B e-invoicing mandate reshaping document workflows across the DACH region, treating archiving as an afterthought is no longer a viable position.

The path forward is concrete: cryptographic sealing at the point of ingestion, complete and protected audit trails, original-format preservation through every migration, and a Verfahrensdokumentation that can be produced on demand. For ERP and SaaS vendors, the most efficient route to all of it is a certified, white-label compliance layer rather than a proprietary silo built from scratch.

Explore how OriginVault's audit-grade invoice archiving infrastructure can be embedded directly into your platform, GoBD-compliant, GeBüV-certified, blockchain-sealed, and ready for the 2025 e-invoicing mandate.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.