E-Invoicing in Italy: A Guide to SdI and FatturaPA

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

Italy Set the Standard. Now the Rest of Europe Is Following.

When Italy mandated electronic invoicing for all B2B and B2C transactions in 2019, it became the first EU country to do so at national scale. The result wasn't just a compliance milestone. It was a structural shift in how tax authorities watch commercial transactions as they happen. Today the Italian model is the reference architecture for the EU's upcoming ViDA reform, and every ERP vendor, software provider, and finance team operating in Europe needs to understand how it works.

This guide covers the full picture: the SdI clearance infrastructure, the FatturaPA XML format, the 10-year preservation mandate, and what all of this means for technology vendors building compliant solutions at scale.

The Italian Blueprint: Why the World Is Watching SdI

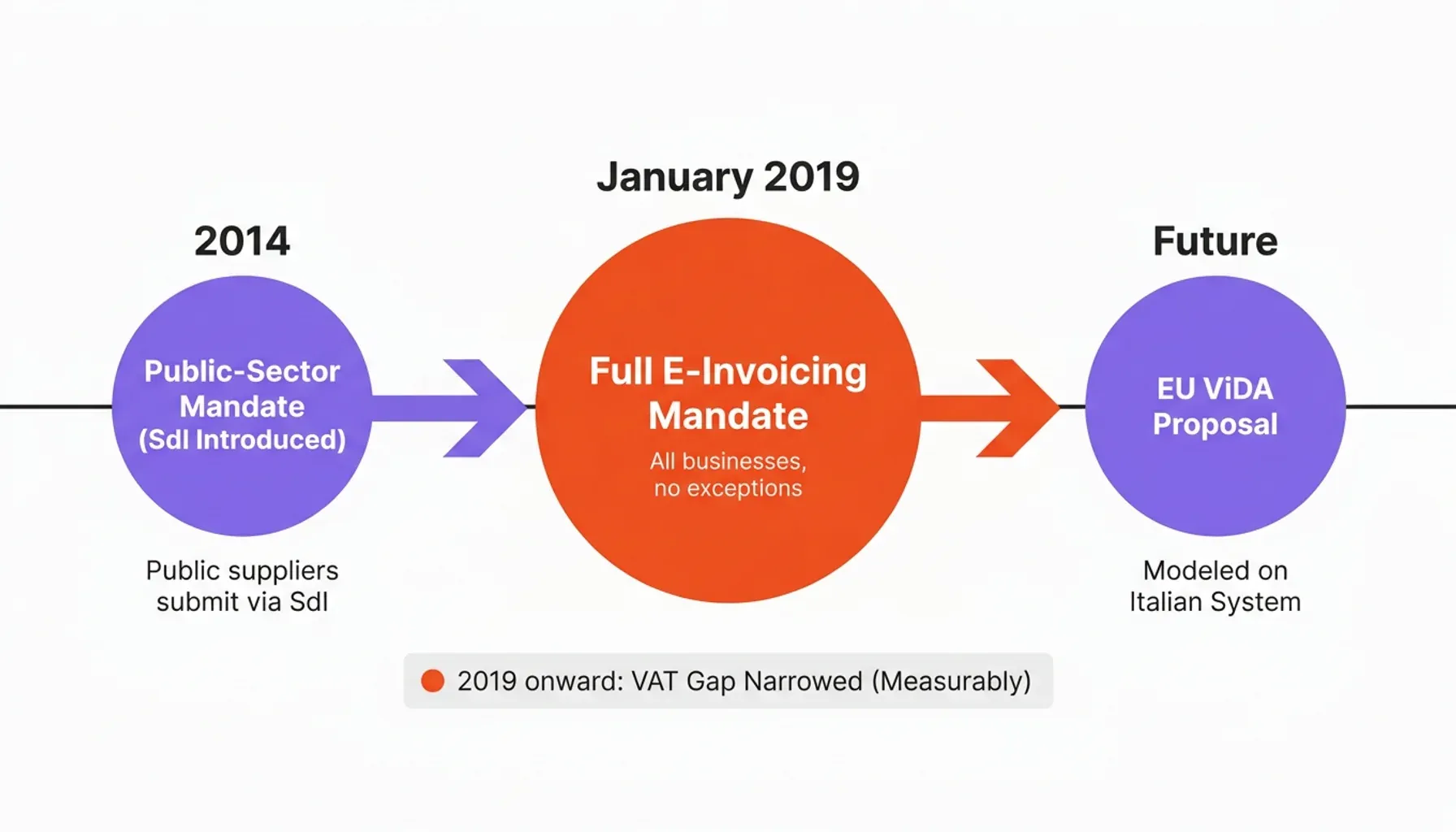

Italy didn't arrive at mandatory e-invoicing overnight. The journey started in 2014, when the government required all public-sector suppliers to submit invoices electronically through the Sistema di Interscambio (SdI). That mandate closed a critical loop: the state could validate, route, and archive every invoice issued to a public body without relying on paper or manual reconciliation.

The private-sector extension came in January 2019, introduced by the 2018 Budget Law (Legge di Bilancio 2018). From that point forward, every VAT-registered business in Italy, with limited exceptions, had to issue invoices exclusively through SdI. No paper alternative. No opt-out.

The driver was fiscal. Italy carried one of the largest VAT compliance gaps in the EU, tens of billions of euros in tax that was owed but never collected each year. By routing every invoice through a state-controlled clearance platform, the Agenzia delle Entrate gained near-real-time visibility into commercial activity, and the gap narrowed measurably in the years that followed.

That success hasn't gone unnoticed. The European Commission's VAT in the Digital Age (ViDA) reform draws directly on the Italian experience as a model for EU-wide digital reporting. When Brussels designs the next generation of tax infrastructure, it looks to Rome.

The Italian e-invoicing ecosystem has three core actors:

- The taxpayer (issuer or recipient of the invoice)

- The intermediary (a certified service provider or ERP platform that handles transmission)

- The Agenzia delle Entrate (the tax authority operating and overseeing the SdI)

Understanding how these three parties interact, and what obligations fall on each, is the foundation for any compliant implementation.

Understanding the SdI (Sistema di Interscambio) Clearance Model

Think of the SdI as a mandatory digital post office. Every invoice issued by an Italian VAT-registered entity must pass through it. There's no bilateral exchange between buyer and seller that bypasses the state. The SdI validates, routes, and archives, and its verdict on whether an invoice is accepted is legally binding.

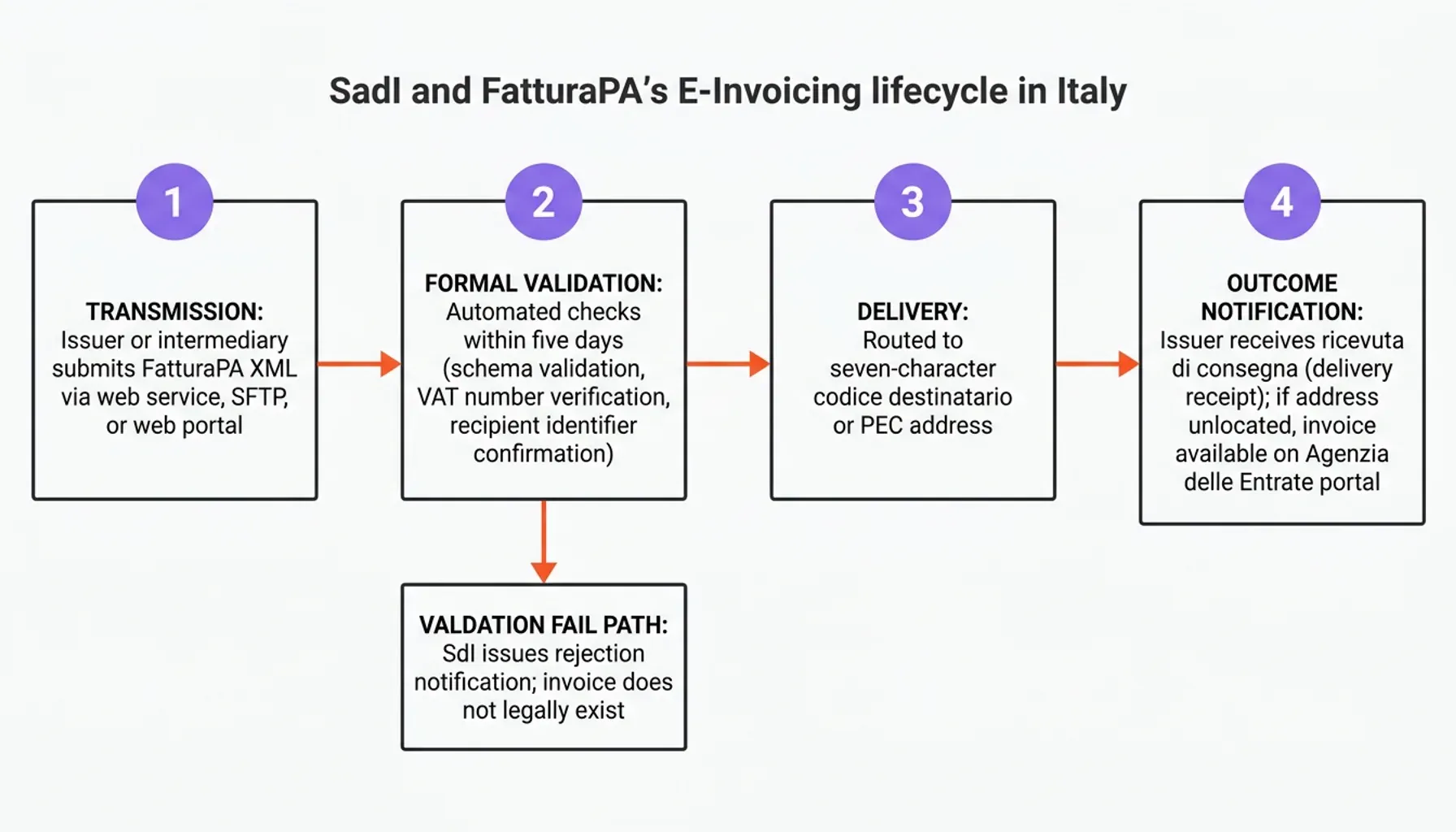

The technical workflow proceeds in four stages:

1. Transmission The invoice issuer (or their intermediary) submits the FatturaPA XML file to the SdI via web service, SFTP, or the Agenzia delle Entrate's web portal. Large-volume operators invariably use API-driven intermediary services.

2. Formal Validation The SdI runs automated checks within five days: schema validation against the FatturaPA standard, verification of the issuer's VAT number, and confirmation that the recipient's identifier (codice destinatario or PEC address) is valid. Fail any check and the SdI returns a notifica di scarto, the formal rejection message, with a numeric error code (for example, code 00400 for a VAT-rate/exemption mismatch) telling you exactly which rule failed.

3. Delivery If validation passes, the SdI routes the invoice to the recipient, either to a seven-character recipient code (codice destinatario) registered by the recipient's intermediary, or to a PEC (Posta Elettronica Certificata) address, Italy's certified email system with legal delivery status.

4. Outcome Notification A successful hand-off generates a ricevuta di consegna (delivery receipt). If the recipient's address can't be reached, the issuer instead gets a ricevuta di mancata consegna (failed-delivery receipt), and the invoice is parked in the recipient's reserved area of the Agenzia delle Entrate portal for retrieval. Either receipt is enough to make the invoice valid; the issuer's obligation is satisfied once SdI confirms transmission.

Here's the part people underestimate. An invoice that draws a notifica di scarto has five days to be corrected and resubmitted, and until it clears, it does not exist for tax purposes. You can't use it to claim VAT deductions, it creates no payment obligation for the recipient, and a rejected invoice left uncorrected past the window means you have, legally, never issued it, exposing you to omitted-invoicing penalties under Italian VAT law. Businesses leaning on manual workarounds or parallel paper invoices carry that risk on every transaction.

Qualified electronic signatures matter before submission. While the SdI applies its own seal to validated invoices, issuers and intermediaries must guarantee the authenticity and integrity of the XML file prior to transmission. That's where cryptographic tooling, hashing, signing, and timestamping, becomes operationally essential rather than optional.

FatturaPA: The Technical Standard for Italian E-Invoicing

FatturaPA is a legally mandated XML schema that defines every data element an Italian invoice must contain, in what structure, and with what encoding. Deviate from the schema and the SdI rejects you automatically. The current version 1.2.x of the FatturaElettronica schema (in force since the SdI overhaul) tightened several rules, which is why a file that validated two years ago can fail today if your generator hasn't tracked the updates.

Core mandatory fields include:

- Issuer and recipient VAT numbers (Partita IVA) and, for domestic recipients, the Codice Fiscale

- Progressive invoice number

- Invoice date

- Line items with unit prices, quantities, and VAT rates

- Total amounts and VAT breakdown

- Payment terms

- The recipient's codice destinatario or PEC address

- A TipoDocumento code (TD01 for a standard invoice, TD04 for a credit note, and so on) that tells the SdI what kind of document it is reading

For public-sector transactions, you'll also need specific codes: the CIG (Codice Identificativo Gara) for procurement tenders and the CUP (Codice Unico di Progetto) for public investment projects. Miss these in a B2G invoice and you're guaranteed a rejection.

Cross-border transactions were historically reported through a separate mechanism called the Esterometro, a periodic summary of invoices issued to or received from non-Italian counterparts. Since July 2022 the Esterometro has been abolished. Foreign invoices now flow through the SdI itself, using specific document type codes, TD17 for purchases of services from abroad, TD18 for intra-EU acquisitions of goods, and TD19 for goods held in Italy under Article 17 reverse charge, to represent the self-billing the buyer must produce.

Common XML validation errors that trigger SdI rejection include:

- Incorrect namespace declarations in the XML header

- VAT rate codes that don't match the declared exemption reason (Natura code)

- Missing mandatory elements in nested XML nodes

- Character encoding issues (the schema requires UTF-8)

- Mismatched totals between line items and invoice summary

Prevention means validating against the schema at the point of generation, before transmission, using the official FatturaPA XSD schemas published by the Agenzia delle Entrate, and keeping those schemas current as they're revised.

The 10-Year Mandate: Legal Requirements for Digital Preservation

Issuing a compliant invoice through SdI is only the first obligation. What happens to that invoice over the following decade is equally governed by law.

Italian Civil Code Article 2220 requires businesses to preserve accounting records, invoices included, for a minimum of 10 years. For electronic documents, that preservation must satisfy Conservazione Elettronica, the framework set out in the AgID guidelines on digital document preservation.

Here is the distinction most companies miss, and it is the one auditors test first. Keeping a PDF on a server or in a cloud bucket is not Conservazione Elettronica. The file can be modified, deleted, or corrupted with nobody the wiser. Italy's defining trait is procedural: invoices are grouped into preservation packages (pacchetti di archiviazione) and sealed with a qualified electronic timestamp at regular intervals, at least once a year, so the entire batch carries cryptographic proof that it existed in a fixed form on a fixed date and hasn't been touched since.

If your platform manages invoices, you're implicitly responsible for ensuring those invoices can survive a tax audit 10 years from now. That's not a feature request. It's a legal requirement your customers will hold you accountable for, and one of the clearest ways to set your product apart.

Italy's annual-sealing rule sits at the stricter end of the European spectrum, and the duration and storage-versus-archiving angle differs sharply by jurisdiction, which is why it pays to read Italy alongside the retention rules across other countries before you design a one-size archive.

Strategic Challenges for ERP Vendors and Software Providers

For ERP vendors, Italian e-invoicing compliance isn't a one-time integration project. It's an ongoing operational commitment with significant technical and commercial implications.

High-availability SdI connectivity is the first challenge. The SdI operates continuously, and invoices submitted by your customers must be transmitted, validated, and tracked in near-real time. For a platform serving tens of thousands of end users, that means solid API connections, retry logic, error handling, and notification pipelines at scale. A single point of failure in your SdI integration becomes a billing crisis for your customers.

Data sovereignty and multi-tenancy add complexity. Italian invoices contain sensitive commercial and personal data governed by both Italian tax law and GDPR. Encrypted, tenant-isolated storage isn't optional. It's the baseline. Managing this across a multi-tenant SaaS architecture, while ensuring each customer's data is logically and cryptographically separated, requires deliberate infrastructure design. If you're wrestling with the intersection of GDPR obligations and document retention, Italy's dual requirements make it one of the more demanding environments in Europe.

The strategic shortcut most scaling platforms now take is to embed a certified white-label archiving layer via API, running under their own brand, so one integration covers Conservazione Elettronica in Italy, GoBD in Germany, GeBüV in Switzerland, and the EU's ViDA rules at once instead of rebuilding the stack market by market. For a deeper look at how that compliance layer becomes a revenue driver rather than a cost center, the analysis on turning archiving into a SaaS growth lever is directly relevant.

Where Italy Fits in the ViDA Endgame

Italy runs a centralized clearance model: every invoice passes through a single state-operated platform before it is legally valid, so the tax authority has full visibility at the moment of issuance. If you already know SdI, the rest of Europe is best understood as variations on that idea. Poland's KSeF is the closest sibling, a mandatory centralized clearance platform whose phased rollout makes it the one to watch. France's 2026 model takes the one structural detour worth noting, splitting transmission between a state platform (PPF) and certified private platforms (PDPs) rather than funneling everything through a single hub.

The EU's ViDA reform, formally adopted by the Council in March 2025, pulls these national approaches toward a common pan-European framework over the rest of the decade, built on the EN 16931 semantic data model. The practical shift for vendors is the move away from periodic VAT returns toward continuous transaction controls, where the state learns of a transaction as it happens rather than months later. The infrastructure you build today has to handle real-time data flows, not just periodic batch exports.

Cryptographic timestamping is the through-line. Tax authorities and auditors need proof that invoice data hasn't changed between issuance and an audit years later, and that is exactly the integrity guarantee that tamper-evident archiving is built to provide. The global trajectory of data retention and audit requirements points consistently toward stronger integrity guarantees, not weaker ones, so vendors that bake this in now aren't over-engineering. They're building the minimum viable infrastructure for the next decade of European tax compliance.

The Bottom Line

Italy's e-invoicing mandate is the most mature and instructive model in Europe. Its SdI clearance architecture, FatturaPA technical standard, and 10-year Conservazione Elettronica requirement define what serious, state-level digital tax infrastructure looks like. The rest of Europe isn't asking whether to follow this model. It's asking how quickly.

For ERP vendors and software providers, the question is equally direct: are your archiving and compliance capabilities built to meet these standards today, and are they architected to scale as ViDA and successor mandates raise the bar?

If you're evaluating how to embed audit-grade, blockchain-sealed invoice archiving under your own brand, ready for Italy, Germany, Switzerland, and the EU mandates ahead, explore OriginVault's white-label e-invoicing archiving infrastructure and see what certified compliance looks like as a product feature rather than a maintenance burden.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.