Belgium E-Invoicing 2026: The Peppol B2B Mandate Guide

Jun 4, 2026

Thomas Hepp

Jun 4, 2026

Belgium E-Invoicing 2026: The Peppol B2B Mandate Guide

January 1, 2026 is not a soft deadline. For every VAT-registered business operating in Belgium, it marks the moment structured electronic invoicing stops being optional and becomes the legal baseline for all domestic B2B transactions. No grace period for large enterprises. No quiet workaround. No consent required from the recipient.

Belgium is joining a growing wave of European mandates, alongside France's 2026 e-invoicing rollout and Poland's KSeF system, in a coordinated push to close VAT gaps and modernize fiscal infrastructure across the EU. What sets Belgium apart is the speed and the scope: every Belgian company in scope, all at once, with no soft ramp by headcount. This guide breaks down exactly what the Belgium e-invoicing 2026 mandate requires, who falls under it, and what your archiving infrastructure must look like to stay compliant for the next decade.

What Changes on January 1, 2026

Belgium's mandatory B2B e-invoicing framework was set by the Law of 6 February 2024 (published in the Belgian Official Gazette in March 2024), which fixed January 1, 2026 as the effective date and built on earlier groundwork from the 2019 and 2022 fiscal reform laws. Starting that day, every VAT-registered company established in Belgium must issue and receive structured electronic invoices for domestic B2B transactions, with no exemption for company size and no opt-out for recipients.

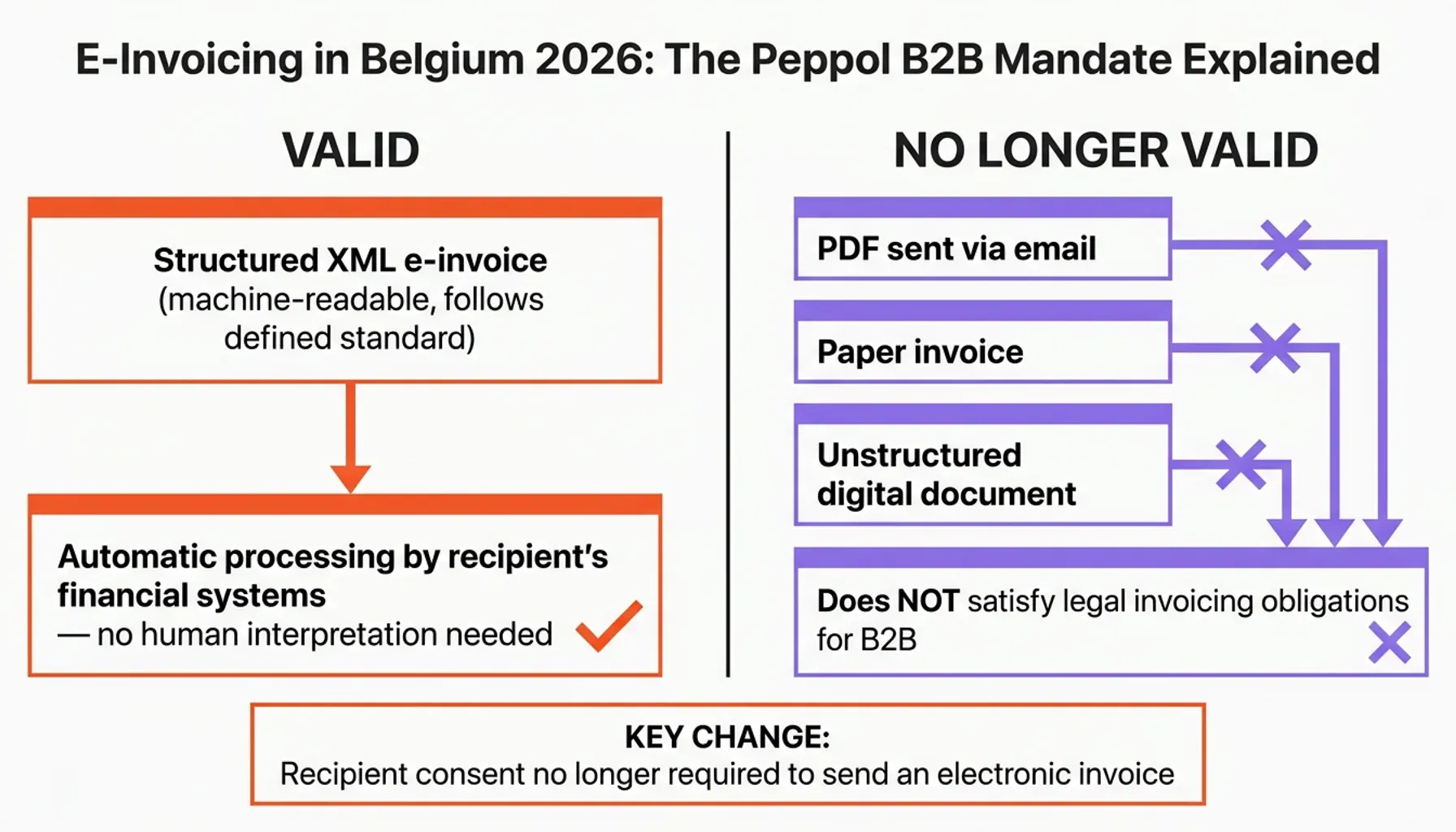

The operative word is structured. A structured e-invoice is a machine-readable XML file in a defined format that the recipient's accounting system can process automatically, with no human re-keying. A PDF emailed as an attachment does not meet that bar, and it never will under this mandate. We unpack why that distinction is now legally decisive in the dedicated guide on whether a PDF still counts as a valid invoice in 2026.

What changes specifically:

- Recipient consent is no longer required to send an electronic invoice

- Paper invoices and unstructured PDFs no longer satisfy B2B invoicing obligations

- Both issuing and receiving structured invoices become mandatory for in-scope businesses

- The obligation applies to transactions between two Belgian-established VAT taxpayers

The rationale is blunt fiscal arithmetic. Belgium's VAT gap, the spread between expected and collected VAT, runs into billions of euros a year. Structured invoicing leaves a digital trail that makes VAT fraud harder to pull off and easier to spot. It also lines Belgium up with the EU's VAT in the Digital Age (ViDA) reform, which extends the same logic to near-real-time reporting across member states later this decade.

The preparation window is 2025. Companies that wait until Q4 to look at their invoicing stack will be doing it under real pressure.

Scope, Start Date, and Affected Businesses

Let me be precise about who this mandate actually covers, because there is a lot of confusion on this point.

Who Is In Scope

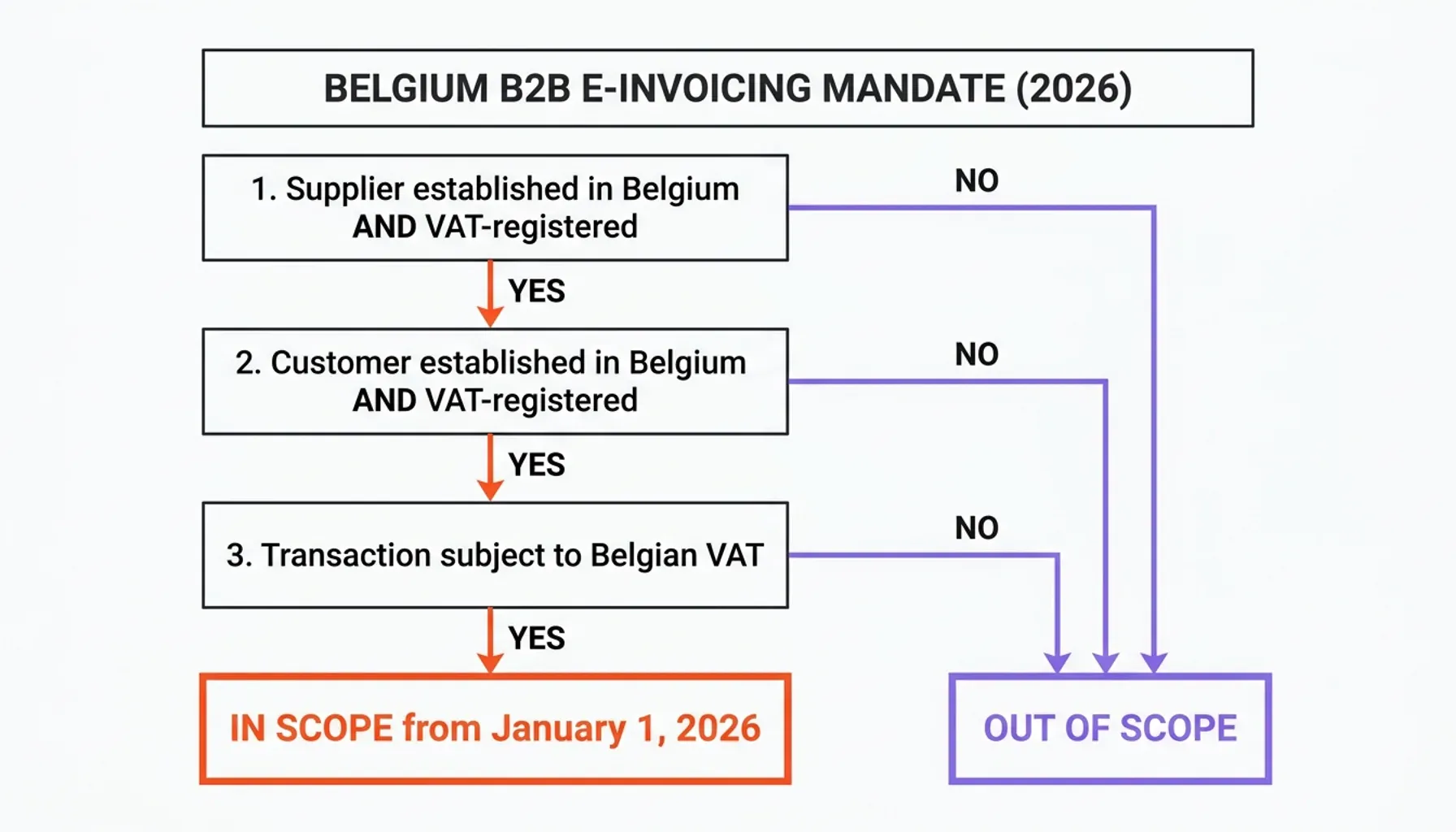

The Belgium e-invoicing 2026 mandate applies to every VAT-registered business established in Belgium that conducts B2B transactions subject to Belgian VAT. That sweeps in the vast majority of commercial activity between Belgian companies, from large enterprises down to mid-market and small firms. There is no revenue threshold that lets bigger businesses off the hook, and no phase-in by company size.

The three scoping criteria:

- The supplier is established in Belgium and VAT-registered

- The customer is established in Belgium and VAT-registered

- The transaction is subject to Belgian VAT

Tick all three boxes, and you are in scope from day one.

Notable Exemptions

Not every business or transaction falls inside the mandate. Current exemptions include:

- Small businesses under the flat-rate (forfait) scheme and those using the special VAT exemption for small enterprises below the threshold

- VAT-exempt activities, such as certain healthcare, financial, and educational supplies, which are not required to be issued as structured e-invoices

- Cross-border B2B transactions, where intra-community supplies and exports to non-Belgian customers sit outside the domestic mandate, though separate EU-level reporting may apply

Cross-border treatment is still moving. ViDA will eventually layer digital reporting obligations onto intra-community transactions, but Belgium's 2026 rule is scoped strictly to domestic B2B flows. If you supply French customers, it is worth reviewing the parallel impact on cross-border suppliers before those obligations land.

Enforcement and Tolerance

Belgium's tax authority, FPS Finance, has signaled a pragmatic line on early enforcement, focusing first on whether businesses have registered on Peppol and can actually receive structured invoices. But pragmatic is not the same as permissive. Companies that make no effort to comply will face penalties. Treat the tolerance period as a runway for good-faith implementation, not as a quiet extension of the deadline.

Legal Framework and Belgian VAT Compliance

Most companies get this part wrong. They treat the legal framework as background noise rather than the foundation their compliance decisions have to sit on.

The Belgian B2B mandate rests on three pillars:

- The Law of 6 February 2024, which wrote the structured e-invoicing obligation into Belgian law and fixed January 1, 2026 as the start date

- The Belgian VAT Code, which governs invoicing obligations, VAT deductibility, and document retention for every VAT-registered business

- Royal Decree implementation, which set the technical standard, Peppol BIS Billing 3.0, as the required format for structured invoices

Under Belgian VAT law, a valid invoice must carry specific content: full seller and buyer identification, VAT numbers, invoice date and number, a description of the goods or services, taxable amounts, VAT rates, and VAT amounts. All of it has to live inside the structured XML, not just in a human-friendly PDF rendering.

Here is the part that bites. The legal document of record is the XML file itself, not any PDF generated from it. That single fact drives how you store, retrieve, and prove the authenticity of invoices during a tax audit, and it carries straight through to your right to deduct VAT. If a supplier sends you a PDF instead of a Peppol-delivered XML invoice after January 1, 2026, your input VAT deduction on that transaction may be at risk. That is not a hypothetical. It is direct commercial exposure for Belgian buyers.

Peppol and BIS Billing 3.0: The Standard Belgium Mandates

Belgium has designated Peppol as the delivery network for mandatory B2B e-invoicing, with Peppol BIS Billing 3.0 (built on UBL XML) as the required document format set by Royal Decree. Practically, that means three things for your software stack: your ERP must generate valid BIS Billing 3.0 XML, you need a certified Peppol Access Point to transmit it, and your system must receive and process inbound Peppol documents automatically, with the XML, not any rendering of it, treated as the legal original.

Peppol itself is the same proven, interoperable network already used for public procurement across Europe, now extended to the private sector. The mechanics of how its certified access points and four-corner routing work are not Belgium-specific, so I will not re-explain them here. If you want the full picture of how the network moves a document from sender to recipient, see our complete guide to the Peppol network. The format mechanics, UBL structure and hybrid PDF+XML options, are covered in the Factur-X and hybrid e-invoice format guide.

The 10-Year Retention Obligation

Sending and receiving the invoice is only half the compliance equation. Belgian law requires businesses to retain financial documents, invoices included, for a minimum of 10 years. For certain real estate transactions, that stretches to 15 years.

The retention rule itself predates 2026. What changes is the nature of the document being kept. When the legal invoice is an XML file rather than paper or a PDF, the archiving obligation attaches to that XML file, and you must be able to demonstrate its authenticity and integrity at any point across the full retention window.

This is exactly where simple cloud storage falls short. Dropping XML files into a shared drive gives you storage, not proof. Belgian auditors must be able to confirm, years later, that the invoice in front of them is byte-for-byte the one originally issued, and a standard cloud folder can be edited, replaced, or deleted with little trace. The distinction between mere storage and genuinely audit-proof archiving, the original-format, integrity, and audit-trail pillars, is the subject of our guide to e-invoice archiving requirements and integrity audit trails. For Belgium specifically, the takeaway is simple: a ten-year obligation on a machine-readable legal original demands archiving that can prove nothing changed.

Proving Integrity Over a Ten-Year Horizon

A decade is a long time to vouch for a file. Belgian auditors do not want a promise that an invoice is unchanged; they want it to be mathematically demonstrable. That means archiving that can prove a specific XML existed in its exact form at a specific moment and has not shifted by a single byte since, including against the people who run the system. Standard enterprise software hands administrators broad rights, so "trust us, nobody touched it" is precisely the assurance regulators discount.

The cryptographic machinery that delivers this, content hashing, blockchain timestamping, and the administrative seal that blocks even privileged insiders from silently altering a record, is its own deep topic, and we cover it in full in tamper-proof versus secure storage and what auditors actually require. Peer-reviewed research on blockchain timestamping backs its reliability as a legal evidence mechanism, which matters here because the integrity of a Belgian invoice has to hold up across the entire ten-year horizon, not just on the day it is filed.

For ERP and accounting-software vendors serving Belgian customers, this is also a product decision rather than a feature to bolt on later. Embedding compliant, tamper-evident archiving natively, instead of pointing customers at third-party workarounds, turns a regulatory obligation into stickiness and contract value. OriginVault's white-label invoice archiving for e-invoicing compliance provides a blockchain-sealed, multi-tenant archiving layer you can embed under your own brand, hosted on European infrastructure to meet GDPR and data-residency expectations. Whether building this in-house makes sense is a classic build-vs-buy decision for a compliant e-invoice archive, and the broader playbook for vendors lives in the guide to white-label e-invoice archiving for software vendors.

Business Benefits: Efficiency, VAT Deductions, and Tax Incentives

Compliance spend on e-invoicing is not purely a cost line. Belgium has attached real financial incentives to accelerate adoption.

The 120% Cost Deduction

This is the standout Belgian figure, and it is worth front-loading in any business case. Companies that invest in e-invoicing implementation can claim an enhanced 120% cost deduction on qualifying e-invoicing expenses. For every €100 spent on software, integration, or Access Point services, €120 comes off taxable income. The incentive is temporary and tied to the transition period, so the early movers are the ones who actually bank it.

Operational Efficiency Gains

Beyond the tax break, structured e-invoicing delivers measurable operational wins:

- Faster payment cycles: Automated processing strips out approval lag. Research on e-invoicing adoption consistently shows payment-cycle reductions of 30-50% once AP/AR workflows are fully automated

- Lower error rates: Manual data entry disappears. Structured XML flows straight into the ERP, taking transcription mistakes with it

- Reporting readiness: The 2026 mandate is a stepping stone toward ViDA's near-real-time reporting. Build compliant infrastructure now and you sidestep a second migration later

For the software vendors themselves, the same dynamic that played out with Germany's GoBD regime and France's 2026 e-invoicing mandate repeats here: compliance quietly becomes a billable feature.

Conclusion: Preparing Your Infrastructure for 2026

The January 1, 2026 deadline is fixed. The technical requirements are defined. What is left is execution.

A practical readiness checklist:

- Software audit: Confirm your ERP or accounting system can generate Peppol BIS Billing 3.0 compliant UBL XML

- Peppol registration: Select and onboard a certified Peppol Access Point, and allow 4-8 weeks for full integration and testing

- Receiving capability: Make sure your system can accept and process inbound Peppol documents automatically

- Archiving infrastructure: Confirm your retention solution meets the 10-year integrity bar, not just storage, but tamper-evident, audit-grade preservation

- Staff training: Finance and AP/AR teams need to understand the new workflow and how to handle exceptions

- Exemption review: Check whether any of your transaction types fall outside the mandate's scope

The businesses that will struggle in 2026 are not the ones who started late on Peppol registration; that is a solvable problem. The real risk sits with those who treat the archiving obligation as an afterthought. An XML invoice you cannot prove authentic a decade from now is a liability, not an asset.

A security-first approach to the document lifecycle, where every invoice is cryptographically sealed the moment it is archived and verifiable at any future point, is the only architecture that genuinely satisfies what Belgian law asks for.

If you are an ERP vendor or software provider building your Belgian compliance offering, explore OriginVault's audit-proof invoice archiving for e-invoicing compliance, a white-label, blockchain-sealed archiving layer you can embed directly into your platform and offer to Belgian customers under your own brand.

Thomas Hepp

Co-Founder

Thomas Hepp is the founder of OriginStamp and creator of the OriginStamp timestamp, which has set the standard for tamper-proof blockchain timestamps since 2013. As one of the earliest innovators in the field, he combines deep technical expertise with a pragmatic focus on solving real business problems, and is a recognized voice in blockchain security, AI analytics, and data-driven decision support. His work has earned multiple international awards, including a top Best Project recognition from ETH Zurich and the Swiss Confederation. He publishes regularly on blockchain, AI, and digital innovation.